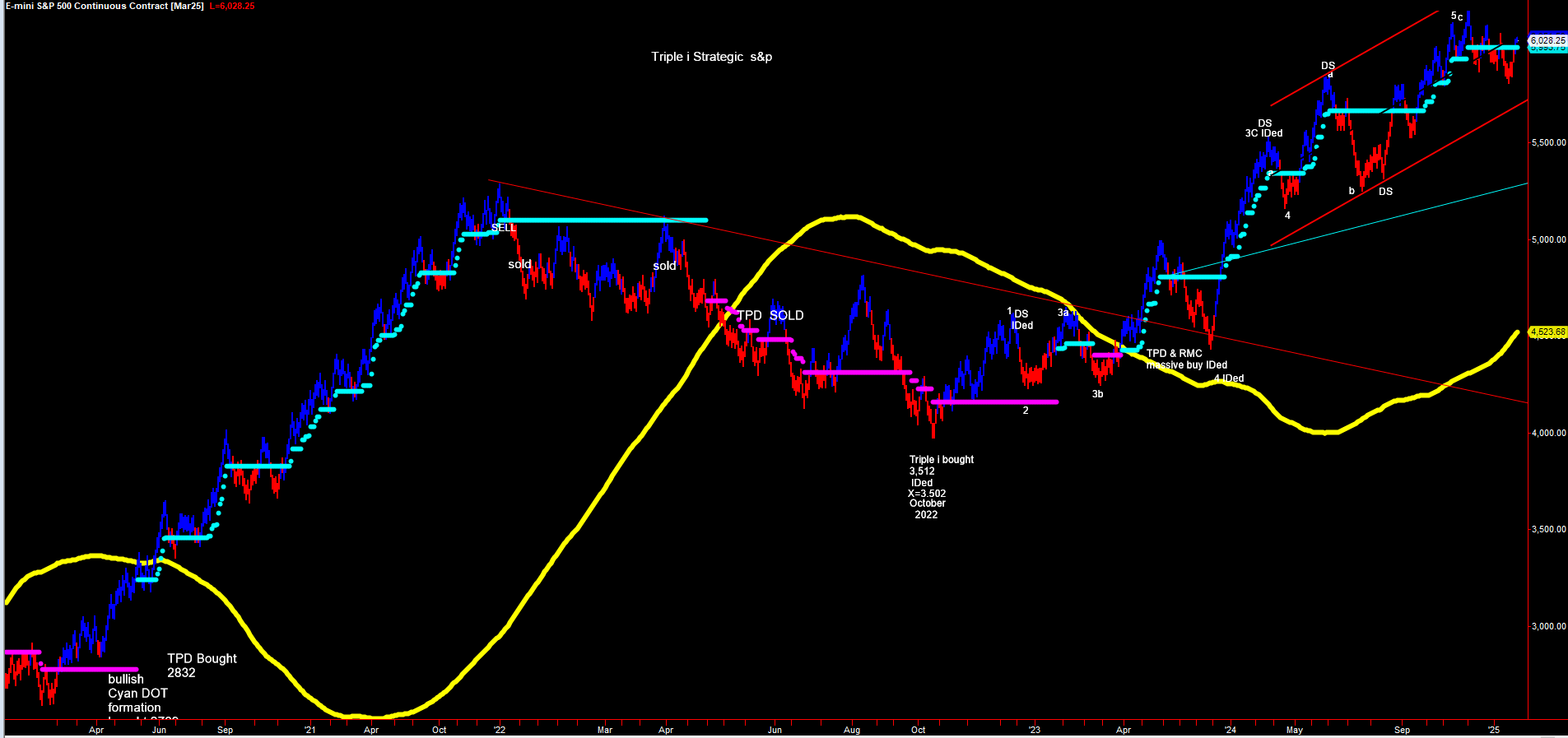

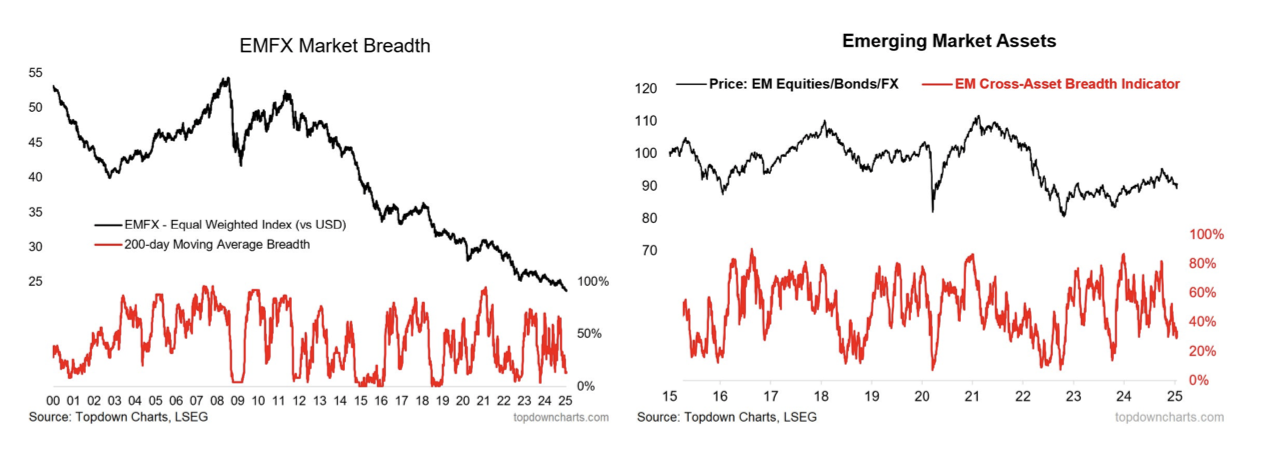

EMFX on the edge

EMFX is at a vulnerable point, claims Callum Thomas. Tariff risks and the prospect of a stronger USD is weighing heavily. EM Europe has already broken support, while LatAm and Asia are right on the cusp (notably USD/CNY). This could all be priced in by now and there may be an element of sell the rumour, buy the fact. But the bigger picture is that this is an extension of a multi-year downtrend for EMFX, and so the burden of proof is definitely on the bulls. The other complicating factor is the general weakness across emerging market assets in recent weeks/months as EMFX, EM Bonds, and EM equities have all come off the boil. The risk is that it all becomes self-reinforcing. Right now, Callum doesn’t see the start of an EM crisis, but it’s worth a close watch.

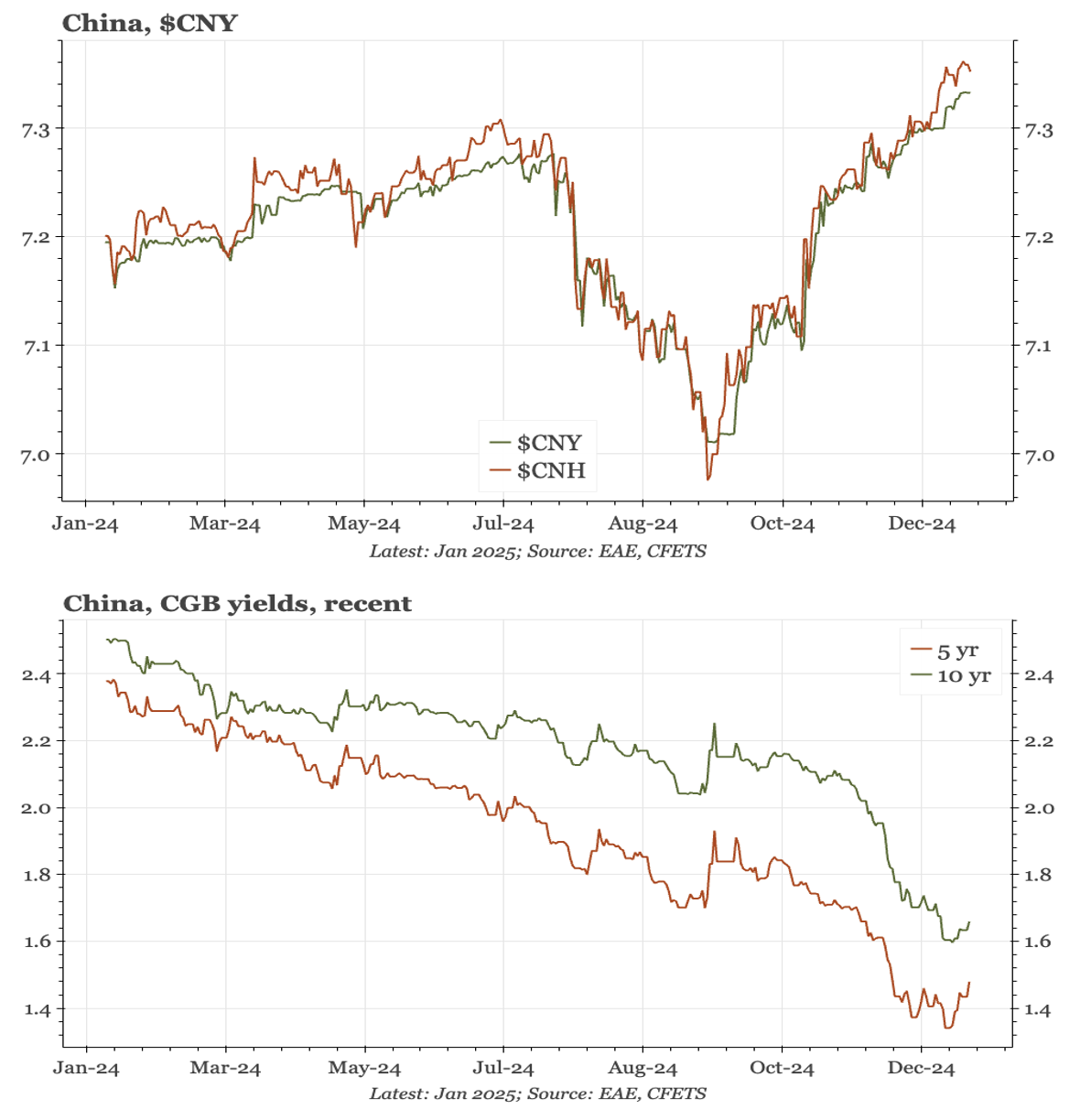

Are low rates and a weak CNY really to be feared?

Paul Cavey points out that there are two things happening in China's financial markets that seem to be causing concern. One is the rise in $CNY, which is likely to gain more momentum if Trump imposes another round of big tariffs. The worry is that this encourages capital outflows and so risks the sort of financial stability seen in China in 2015. The second development is the fall in yields. That was indeed sharp in Q424, with rates at the longer-end of the curve in particular falling to all-time lows. The substantive idea is that a 10-year yield of just 1.7% is pricing in a multi-year period of deflation and very slow nominal growth. Paul assumes that management of the cycle is probably the paramount concern in the minds of both policymakers and investors right now. It is only in that context that the continued loosening of domestic monetary conditions is welcome.

Asia: Chips and electronics

Niall Ferguson’s spent a week in India and Malaysia, meeting with high-level executives from the tech, semiconductor, and venture capital industries, as well as senior politicians. Both countries are ramping up investments in semiconductor and electronics manufacturing, supported by foreign capital and government initiatives. India is poised to grow its market share in low-end assembly for Western chipmakers and electronics, though talent shortages and bureaucratic inefficiencies hinder progress. In Malaysia, business leaders are concerned about losing market share to Chinese firms in the domestic chip industry, while the government remains accommodative, despite internal debates. The overall outlook is one of optimism, and both countries are well positioned to strengthen their roles in low-end chip assembly for Western tech firms.

Republic of Congo: Shuffles and reforms

President Denis Sassou-Nguesso undertook a minor cabinet reshuffle on January 11th. The most significant component of the reshuffle was the appointment of Christian Yoka as the new minister of the finance, budget and public portfolios, with the majority of other ministries unaffected. Yoka’s appointment is rooted in several considerations, including the government’s need to accelerate its reform programme amid enduring fiscal constraints. The appointment should bolster the state’s reform programme over the medium term to the benefit of the country’s otherwise modest economic outlook. However, the economy is subject to an array of headwinds, including the country’s dependence on oil revenue and limited buffers against any future shocks.

India’s economy sags further into 2025

Growth momentum has weakened further. Jonathan Anderson’s proxy index now shows real growth of 3.5% y/y coming into 2025. There’s no collapse but it is a clear across-the-board slowdown. Jonathan doesn’t expect serious easing or stimulus. The external balance, the rupee, inflation and the fiscal position are all constraints on the government's ability to take significant action. Meanwhile, equities remain expensive. The market may have come down over the past couple of months, but multiples are still trading at wide gaps to the rest of EM.

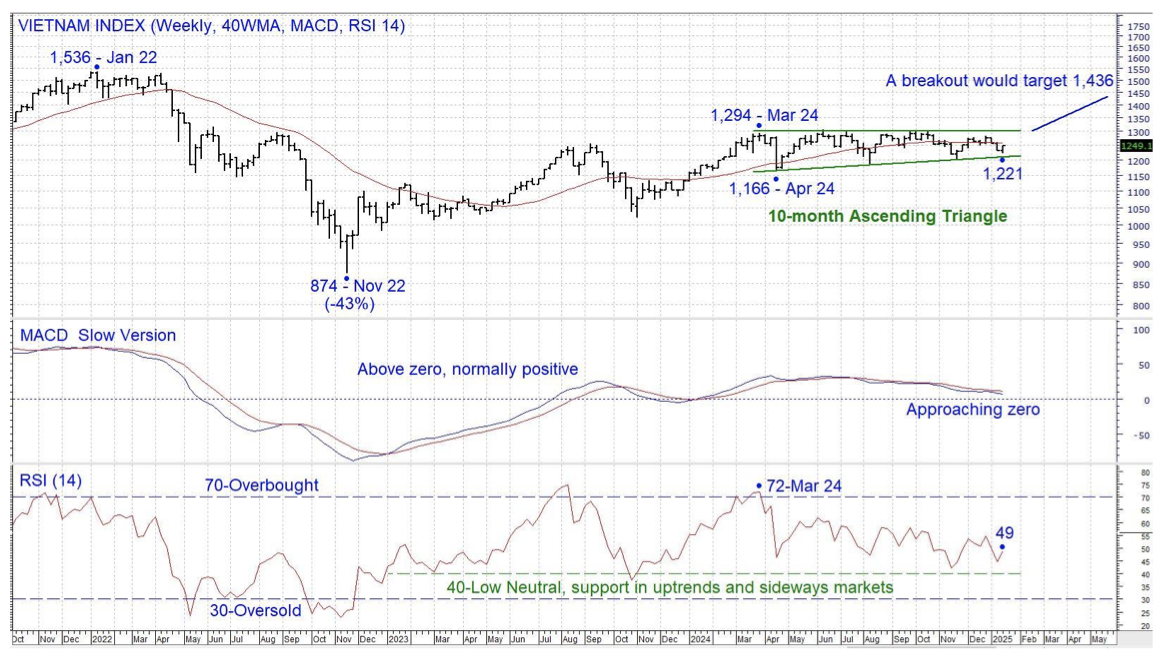

Vietnam: Breaking free?

The Vietnam Index first traded above 1,000 years ago but has since been unable to sustain a move away from that level. In 2022 the index peaked at 1,536, then fell by more than 40% in the same year. However, the short amount of time below 1,000 suggests that the market is converting the old ceiling into a floor. Since the March 2024 peak of 1,294, a potential 10-month Ascending Triangle has formed, a breakout would target 1,436, just below the 2022 peak. Chris Roberts will go 100% long on a weekly close above 1,330, using a daily close below 1,209 as a stop loss. His initial target is 1,436 and then a test of 1,500+.