Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

EU Telecoms: The calm before the storm

New Street expects to see an uptick in M&A activity this year after a lull in 2024. Some of the larger transactions are likely to be potential attempts at further 4-3 deals following the successful approvals in Spain and the UK. Key markets where this could happen are Germany, Italy, France, Sweden and Denmark. From an investor perspective, the best way to play this theme would be through Telefonica, 1&1, Telecom Italia, Altice France bonds or Bouygues. Away from potential 4-3 mergers, other fiber deals could still be a further theme in Europe in 2025, and again Telecom Italia comes into focus as a beneficiary of a potential NetCo-OpenFiber transaction.

BMW (BMW GR) Germany

Woozle’s latest channel checks suggest BMW is on track to achieve a +0.8% Y/Y increase in global revenue for 4Q24 vs. consensus forecasts of a -4% decline. This positive outcome has been driven by a robust performance in Europe (+1.1% Y/Y revenue growth) and the Americas (+1.6%). Sales volumes increased due to new model performance and discounts, with key models such as the BMW 5 Series/6 Series and BMW 7 Series/8 Series outperforming expectations. Foot traffic increased compared to last year, aiding sales growth and reflecting improved consumer interest in BMW.

Continuing with Fighting Financials thematic view of a downturn in pockets of the global construction and DIY sector, they recently added HWDN to their list of equity short ideas. Business fundamentals continue to deteriorate with revenue growth slowing and a steady decline in margins. For 2025, they are concerned by several headwinds facing the UK economy and expect demand for large “big box” discretionary purchases to remain weak. While management has already guided down market expectations regarding the group’s FY24e print, Fighting Financials sees some risk of a negative revision to the 1H25 outlook too.

Zalando (ZAL GR) Germany

Iron Blue initiates coverage on ZAL with a score of 28/60, which is top decile (fertile grounds for shorting) and an outlier compared with bottom decile/quartile scores of internet peers Auto Trader (13/60), Rightmove (11/60) and Scout24 (16/40). They highlight 1) Increased use of stripped out restructuring and other costs. 2) Stripped out share-based payments (27% PBT adj). 3) Profit recovery supported by compressed fulfillment, marketing and inventories provision expenses. 4) Pronounced gap between tangibles capex and the depreciation charge. Re. governance, they note CEO variable pay targets that are either undisclosed or below external targets, a non-independent Remuneration Committee and sizeable related party transactions. FY24 sees a change in auditor following the incumbent’s tenure of 13 years.

InPost (INPST NA) Netherlands

While INPST’s latest trading update may not have contained any financial data, it does appear as if the company has once again managed to beat expectations. Particularly pleasing is the further acceleration of growth in Poland, which suggests INPST has outpaced the growth of the overall market. Meanwhile, growth in the UK remains spectacular. B2C volumes are still relatively low. However, the recently announced collaboration with Yodel (in Locker-to-Door deliveries) will also provide INPST with access to over 12,000 Collect+ pickup points, thus establishing a truly nationwide network of OOH points, which offers a solid basis for further volume growth going forward.

North America

2025 year ahead outlook

Trivariate sees the US equity market as increasingly risky near-term, but eventually ending the year at new highs. Long-term, they see the S&P500 nearing 10000 by 2030, driven by 8.6% p.a. EPS growth. Revenue acceleration will matter more than gross margin growth in 2025 for stock selection. High-quality, low-beta, low forecasted growth outperforms among growth stocks. Value has lagged Growth by 1.3% p.m. for 50 years. Focus on low capital spending and high FCF among value stocks. Small caps are not cheap. Healthcare and Industrials to outperform Consumer Discretionary and Communication Services. Trivariate is tracking 6 Growth baskets: AI Semis, AI Software, Electrification Industrials, Housing / Building Product, Power / Utilities and Healthcare Services.

Consistently generating alpha on the short side

2024 was the largest alpha year in OWS's history - an equal-weighted basket of their short ideas outperformed the inverse of the S&P 500 index by 21.3 percentage points, with Atkore, Nucor and Upwork outperforming the most. They showed an impressive consistency, beating the index in each quarter. In Q4, OWS initiated 4 new short recommendations including Penumbra and Signet Jewelers. At the end of year, they had 17 short recommendations outstanding. For 2025, they see opportunities in cyclical setups, AI and in speculative small caps.

Mediocre capital intensive company trading at a sky high price. LTM, “below the line” NCI/Pfd expenses were $448m ($567m pre-tax) which is 64% of LYV's pre-tax income of $880m. So, minority partners are earning almost two thirds of the profits of the business! The sell-side is increasing price targets using ridiculous EV/AOI basis. Capex / Investments are now greater than D&A, and the bulk of the profits are going to the “below the line” partners, which is not captured in AOI. LYV benefitted greatly from the end of Covid lockdowns. Now it is back to normal pedestrian growth. Meanwhile, German competitor, Eventim, recently saw its share price fall 15%, as fears increase that pressure on live entertainment margins could be here to stay. TP $90 (30% downside).

GLBE is an underappreciated, leader in the high growth cross-border and D2C eCommerce market. The sustainability of 25-30% revenue growth is attractive, along with the clear value added to customers despite macro challenges. Abacus believes the Shopify deal has the potential for meaningful upside surprise over the next two years. Farfetch, GLBE’s closest competitor, has exited the business giving a strong tailwind to 2H24 and 2025 new merchant bookings that underpin 30%+ GMV growth in 2025. TP $100 (90% upside).

ULTA’s Q4 update reinforces JJK’s outlook for a strong holiday season for the beauty sector, driven by newness and to a lesser extent increased value vs. LY. They expect ULTA’s prestige makeup category continued to improve in Q4 and its mass category to generate +LSD revenue gains. JJK’s Q4 EPS estimate increases to $7.30, nicely above $6.87 consensus. This raised projection brings their FY24 EPS forecast to $24.20. Kecia Steelman has been announced as the company's new CEO; she has proved to be a strong executor and team builder with well-developed operations and supply chain experience. JJK looks for ULTA’s planned investments in FY25 to fortify the company’s positioning and deliver a return to growth and market share.

A secular bull market for Bank stocks

Looking back over the past half-century, Charles Peabody has never felt so invigorated about bank stocks. They are poised to generate fundamentals as good as the market, but trade at a substantial discount to the market. Many of the reasons for this discount are likely to abate in the coming years and investors will take note. He discusses the favourable outlook for bank revenues, asset quality, capital generation and regulatory relief. His top picks include Citigroup (a self-help story with a credible CEO trading at 2/3 of TBV) and Wells Fargo (labouring under an asset cap since 2018 that is destined to be lifted), as well as M&T Bank and Citizens.

Fully depreciated equipment in the Building Products industry

Among the 19 companies analysed by BTN, those with the biggest risk of overstated earnings from using fully depreciated equipment or unusually long depreciation lives compared to the industry include Allegion, A.O. Smith, Insteel Industries, Trane Technologies and Masco. Meanwhile, they see Simpson Manufacturing, Advanced Drainage Systems, AAON, Trex and Builders FirstSource as being positioned to start seeing lower depreciation expense and capital spending. These companies are already years into modernisation and expanding their equipment bases. Their depreciation has risen and been a headwind to earnings of late, but they may be about to see this level off and put them in a position of rising margins and FCF.

While Q3 managed to show modest revenue growth, Corto believes demand is slowing and product growth will continue to decline in 2025, placing pressure on ARLO's services business. The surveillance manufacturer faces multiple headwinds including lapping more difficult comparables, a potential pull-forward of orders by its largest customer, subscriber growth headwinds and regional weakness. Corto also flags multiple executives selling shares in recent months. Sees 40%+ downside.

Equinox Gold (EQX CN) Canada

GMR sees EQX as one of the strongest production growth companies in their gold universe (for 2024 to 2030E). EQX offers value vs. gold peers with a P/NPV10 using GMR forecasts at 0.7x (sector average 1.1x) and P/NPV5 using spot at 0.5x (sector average 0.8x). Key metrics of AISC, FCF and net debt are set to improve markedly over the next few years with the ramp-up of Greenstone. Greenstone construction lifted net debt from US$0.2bn in 2020 to US$1.1bn in 2024E, but GMR forecasts the miner to turn net cash positive by 2029, providing opportunities for the allocation of capital including shareholder returns. TP C$9.90.

Tech: AI innovations, market disruptions and emerging opportunities

The themes SPR will be focusing on in 2025 include 1) AI related: (a) AI applications move to the edge - benefitting the likes of Ciena, Arista and Crown Castle. (b) AI networking transition to ethernet vs. InfiniBand, benefitting Arista, Cisco, Juniper and Extreme. (c) AI use cases that are delivering strong ROI vs. others that are not, despite strong sales efforts by vendors - impacting renewals for Salesforce, ServiceNow, and others. 2) In cyber security, areas of growing priority include SOC automation and Next Generation SIEM. 3) More vendors bypass distribution and sell via the CSP marketplace or direct, negatively impacting large distributors. 4) BEAD - despite delays, this program will drive meaningful revenue. 5) Vendors benefitting from the rapid growth in DevOps / DevSecOp.

Japan

2024 was ugly for turnarounds, 2025 should be awesome!

An uptick in TOBs, MBOs and merger talks is suddenly making it unsafe to short low-PBR companies indiscriminately. Dozens of previously complacent companies are acting to up their profitability and the market is taking notice. More than two-dozen large- and medium-cap stocks with deep discounts to the benchmark began to bounce off well-defined support levels in late Dec. The turnaround strategy was tough in 2024 because most of the stocks that fell out of bed in 2023 were not turnarounds. They were grossly over-valued theme stocks that suffered massive changes in sentiment. This year is starting out completely different. Mike Allen introduces 20+ turnaround ideas that have more potential than anything he saw at this time a year ago.

Emerging Markets

Active GEM Funds: Positioning insights

Steven Holden highlights 3 key investment themes across his Global Emerging Market fund universe: 1) Average exposure to South Korea has plummeted to 15-year lows of 9.25%. Net outflows of $2bn and a significant reduction in exposure to Samsung Electronics have collectively driven South Korean exposure down by -1.75% over the past six months. 2) Real Estate exposure is rebounding. The percentage of funds invested has risen to 76.7%, nearing a 5-year high, with average weights and benchmark metrics at their highest levels in 10 years. 3) South African Financials are experiencing a resurgence with 69.54% of funds now holding exposure - the highest percentage in 4.5 years.

Nigeria is showing signs of life & Banks are 2x earnings

Recent progress within the country has been helped by two Eurobond sales last month (the first in nearly three years) for a combined US$2.2bn, stable interest rates and - shockingly - a rebound in the currency. If/when the devaluation stops, the entire economy can explode higher in USD terms via the natural equilibration of street prices back up to normal levels in real terms. Mike Churchill has been running the rule over some of the Nigerian banks and insurers including the likes of Access Bank, United Bank for Africa and Zenith Bank, with each one offering massive upside as well as double digit dividends.

China Logistics: Moderation, consolidation and overseas

China last-mile parcel volume grew 22% Y/Y in 2024, far outpacing e-commerce growth of just 6.7%. The decline in consumer confidence actually drove greater volumes due to consumers buying smaller ticket items more frequently and returning more. Blue Lotus expects these two trends to moderate in 2025. Cross-platform integration is thus the No.1 priority and Blue Lotus sees JD Logistics as the prime beneficiary. They expect ZTO’s share loss to continue amid diminished returns to scale, as well as a return of J&T to overseas expansion to drive its upside. Their top pick in the China logistics space in 2025 is JDL. They maintain a Sell rating for SF Holding. They initiate J&T with a Buy rating and downgrade ZTO to Sell.

Salik (SALIK UH) United Arab Emirates

High efficiency, asset light, minimal capex, with high wealth & rising population, generating accelerating FCF - Salik is unique in Insight’s Global Toll Road universe as it has the right to operate all future toll gates in Dubai (vs. competitive bidding elsewhere). In Robert Crimes' updated financial model for the stock, 10 toll gates are operational and he adds 4 new value accretive toll gates in 2027-36E (AED2.8 a share). He also considers the introduction of variable pricing (from end Jan 25) as very positive, adding additional net revenues of AED170m (AED0.6 a share), substantially above management's guidance of AED60-110m. As a result, his TP increases by 45% to AED11.0 (100% upside).

Big Tech: Asia vs. US - Samsung spoils the chase

2024 was a banner year for mega-cap US Tech companies, with Apple, Nvidia, Microsoft, Amazon and Meta rising a collective +64%. Were it not for Samsung Electronics crashing -41%, Asia’s mega-cap Tech companies (TSMC, Tencent, Samsung, Alibaba and Meituan) would have almost matched their US peers: +61% collective return (USD) without Samsung but +40% with Samsung. The good news: rolling into 2025, Crystal Shore has a positive risk rating on all 5 Asian Tech companies. Even Samsung.

Macro Research

Developed Markets

The story for 2025

Last week, Andrew Hunt noted that inflationary pressures within the non-traded goods sectors remain elevated, largely a result of the huge cyclically-adjusted budget deficits that many governments continue to run. These deficits also imply that net public debt issuance will exceed household saving by a considerable margin this year. If governments cannot embrace growth-sapping austerity, they will need to either accept higher yields to attract foreign savings / crowd out domestic investment, or return to some form of de facto QE and yield curve control. Ultimately, Andrew expects the latter to occur but not before a further rise in bond yields over the next 3 – 6 months that tips the Global Economy into a recession, while also undermining equity and credit valuations. He then expects a panicked and aggressive easing of global monetary policy in H2/2025.

Austria: Turning (far) right?

Austria may be headed for a government under Herbert Kickl, the leader of the far-right FPÖ. It may be more than three months after the elections, but coalition talks between the conservative ÖVP, the Social Democrats, and the liberal Neos collapsed. Karl Nehammer, former ÖVP chancellor and the lead figure in those talks, resigned. His attempt to keep the FPÖ out of power, even if they won the elections, backfired. Wolfgang Münchau says that there are now two options moving forward: a coalition government between the FPÖ and the ÖVP as a junior partner or new elections. The FPÖ has been rising in the polls to 35% in December and are likely to benefit even further from the current political crisis. So, everyone else apart from the FPÖ has an interest in avoiding elections. After 98 days, Austria is back to square one.

Resilient US growth

After one of the most volatile starts to the year in equities — driven by tighter liquidity trends around year-end, signalling funding stress in the banking system — the traditional Santa rally was effectively cancelled, and tax-driven equity selloffs were brought forward. However, we are now seeing a return to more normal market conditions. Ulrik Simmelholt’s growth models for the US have shifted to the upside, reducing the likelihood of an imminent decline in bond yields. That said, he anticipates a strong January for risk assets, supported by two key factors: liquidity has tightened significantly, increasing the chances of a Fed response to inject liquidity. US growth remains resilient. Ulrik enters the week with the following short-term allocations: long US equities; neutral US fixed income / USD; long energy commodities, but short industrial metals.

Blonde Money

Trump 2.0

The final two weeks before Trump returns. Except, he's already back, isn't he? In many ways these are the most powerful moments for an incoming US President as the courtiers muscle their way towards the new King. Helen Thomas points out that the markets have decided DJT 2.0 is mostly great news for risky assets with volatility lower and the S&P500 higher. It doesn't matter for now that this term is accompanied by dramatically higher inflation and interest rates and an entirely different post-pandemic economy. Meanwhile in Europe, dysfunction is shattering the governments of Germany, France, and Austria. The ECB is doing its best to step into the void, gunning for rate cuts; German data should provide them with yet more grist to the dovish mill.

Bond yields have normalised

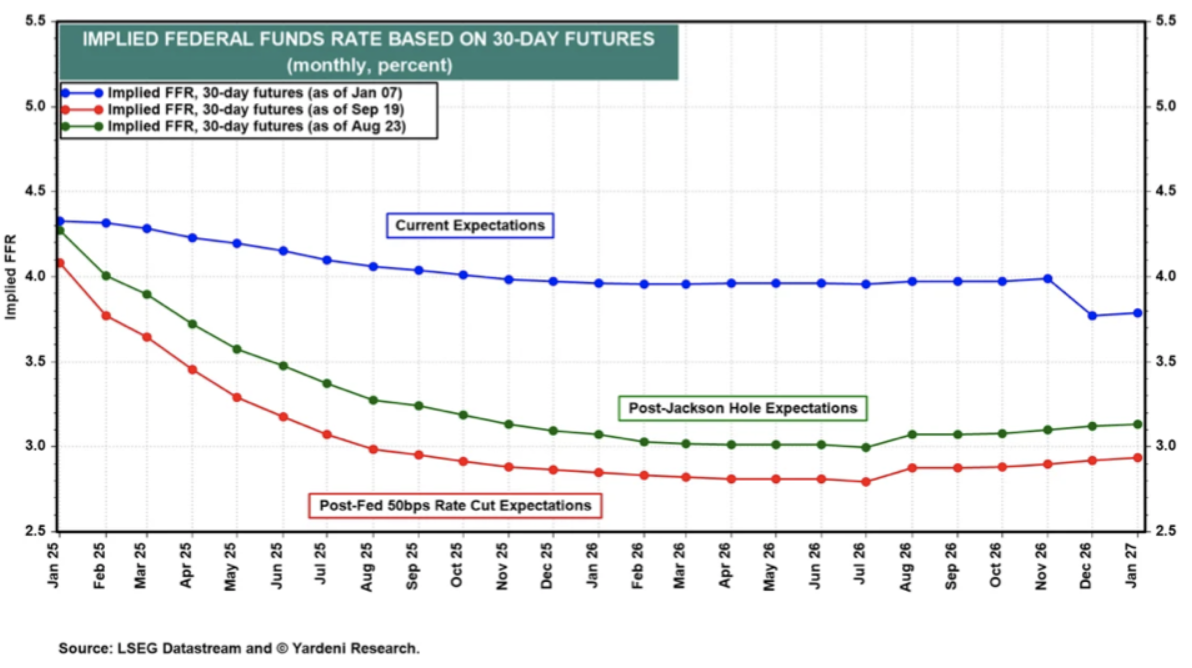

The 10-year yields should be between 4% and 5%, as it did in the years before the GFC. The recent yield curve changes and Fed decisions led bond vigilantes to conclude that monetary policy is stimulating an economy that doesn't need to be stimulated. That’s been Ed’s assessment since last August, and he predicted that yields would rise. FFR futures are pricing in roughly two or three more 25bps rate cuts this year (chart), but Ed believes that additional rate cuts would increase the odds of a stock market melt-up from 25% to 30%. Higher yields don’t appear to be weighing on stocks, but that’s because yields are returning to historical norms. Overweight high quality and cyclical sectors of the S&P500 including information tech, comms, financials and industrials.

US: Risk on

High yield spreads are at 17-year narrows. The major indexes across the market cap spectrum remain in uptrends. Interest rate volatility (MOVE index) continues to stabilise and move lower. Semiconductors (SMH, NVDA, TSM, AVGO) are re-emerging as leadership. Consumer Discretionary (XLY), Communications (XLC), Technology (XLK), Services, and many other high-growth risk-on areas (ARKK, ARKQ, ARKF, ARKW, BITQ, WGMI, IPO, etc., all of which the Vermilion team remain bullish on) are near new RS highs, while defensives including Staples (XLP), Health Care (XLV), Utilities (XLU), and Real Estate (XLRE) are all underperforming and near 6+ month RS lows. Discretionary vs. Staples ratios (XLY vs. XLP, RSPD vs. RSPS) continue to move up and to the right. Bitcoin remains bullish and is at all-time highs. This is all in spite of the December pullback, and is consistent with an equity bull market.

US: Too early to be bearish

Despite the new year, a dramatic shift in the US political scene, and a hawkish evolution for the Federal Reserve, Paul Krake notes that the investment landscape remains dominated by a single narrative—Artificial Intelligence. AI and the companies driving it will dominate the investment framework for years to come. The focus on global beta remains concentrated in a few Pacific Coast technology firms hyperscaling AI. While there are other narratives—clean energy deployment, infrastructure, expanded military capabilities, and even weight loss—these themes feel secondary to AI. It is the singular force capturing society’s imagination, driving productivity, and, for some, feared as an existential threat. The supremacy of the US economy, home of the world’s greatest companies that will drive AI, is a more powerful force than the uncertainty over the Trump presidency or the Fed not easing as quickly as short-term allocators would like.

A slow start to the new year

Global liquidity growth has dipped sharply in the last few weeks. The resurgent US dollar and weak central bank liquidity growth is holding global liquidity in check. Risk asset markets perform best when liquidity is growing strongly. The liquidity boost in Q3 2024 bolstered markets but the slowdown from Q4 is now feeding through. Mike Howell stands by his view that liquidity will expand a tad further this year before peaking in Q4. This final upswing of the current liquidity cycle may bring some further upside, but the best of times are likely behind us.

Closing in, closing out

Sharmila Whelan reflects on an eventful year, although one that was marked by success for Westbourne Research. Of the 43 calls made on global markets and 11 countries/regions, 69.8% were accurate. Among them were the accurate prediction of the US soft landing, a strong USD, a broad-based US led global stock market rally, sub-par growth in Europe, and overweight Bitcoin. Sharmila had also accurately forecasted that India would remain the best multi-year growth story in Asia, and that the TAIX would be the regional outperformer in 2024.

Emerging Markets

China: An exciting buying opportunity

The Shanghai Composite’s (3,211) monthly chart features two major chart patterns: a 17-year Symmetrical Triangle and a 9-year Rectangle. Chris Roberts is focusing on the latter. The fast 36% rally in Sep/Oct, reversed sharply from resistance at the top end of the pattern, leaving more participants with losing positions. A confirmed breakout from the 9-year Rectangle would be viewed as an exciting buying opportunity, leading to a test of the area of the 2007 peak. The biggest risk Chris sees at this juncture is that the 2007 peak is akin to Japan’s 1989 major top, and that the secular bear market is not yet complete. But this is not his preferred view.

China: Political messaging fails to inspire

Beijing’s approach so far has been to focus on asset prices and demand as the keys to the 2025 growth equation. William Hess disagrees that demand is the problem. Central economic planners are pretty good at backing out how much demand they need to engineer. Where it comes to stabilising asset prices, this is important to shore up nominal anchors for domestic price expectations and interrupt negative wealth effects. But this is not enough. For asset prices to sustain increases there needs to be tailwinds from stronger cash flow accruing to those assets and incomes that end up with would be buyers. Attention to these income questions largely absent from Q4 stimulus theatre. That said, changes to incomes (and income expectations) should be the byproduct of changes to the underlying economic process(es), and this is where the issues of political leadership and narratives come in.

Is India ready to be a Tiger?

The economy has enjoyed a cyclical boom over the past two years, but has India done what’s required for strong, sustained growth over a decade? Jonathan Anderson says no. The biggest problem with the economy is the lack of a vibrant export sector. Then there’s a lack of momentum in moving beyond consumption and small-scale investment into infrastructure. Finally, with a wide deficit and one of the highest public debt ratios in major EM, there is no room for fiscal stimulus but plenty of risk during a downturn scenario. All of this is precisely why Jonathan exited his equity holdings late last year; for now, the country remains a cyclical story.

Macro-Advisory

Russia: Kremlin trades growth for prudence

Growth stayed strong into the year-end, with increasing output in both the manufacturing sector and consumer spending supporting 4% GDP growth. But momentum is slowing as deceleration mode kicks in. The government is showing signs of a more conservative approach as it seeks to move to a balanced budget and bring inflation down. This will likely halve GDP growth to 2% this year. Christopher Weafer forecasts CPI to decelerate to 6-7% by year-end, which should allow the CBR to cut its key rate from the current level of 21% by around 500bp during 2H25. Expect the ruble to stay in the RUB90-100/US$ range. Geopolitics remains the wild card, with the potential to exert greater strain on Putin's economy.

Burumcekci Research & Consulting

Turkey: What’s the agenda?

At the end of last year, the Central Bank published the “2025-2027 Research Agenda” for the first time. The document aims to provide a strategic framework for prioritising topics while deepening the Bank's understanding of the economy. In his latest report, Haluk Burumcekci outlines the key focus areas and prominent research topics included in this document. The fact that we have already seen new decisions related to one of these research topics—"The financial stability implications of firms' foreign currency borrowing and the effectiveness of foreign currency credit constraints"—in the early days of the new year suggests that future policy steps are likely to emerge from the themes outlined in this document. Haluk hopes that Turkey's political environment does not hinder decisions aligned with the central bank’s principles.

Commodities

Crude gets a prop from polar vortex

It was an expectedly slow start to 2025, but crude caught the eye by bouncing out of its narrow range of the past nine weeks. Brent futures flirted with levels well above $76/barrel in intraday trading through Friday. Vandana Hari noticed some news reports attributing the bounce to Chinese manufacturing PMI in December and the US Energy Information Administration reporting a fifth consecutive weekly drawdown in crude stocks. It was neither. The supportive factor for crude was some bullishness in the European gas and diesel markets as the region braces for a colder-than-normal January. It has also ran down its gas storage faster-than-usual in December, lost about 15bn cubic metres per day of Russian pipeline natural gas supply via Ukraine, and is experiencing dunkelflaute, a period of low intensity of the sun and wind, which causes a sharp drop in renewable power generation.

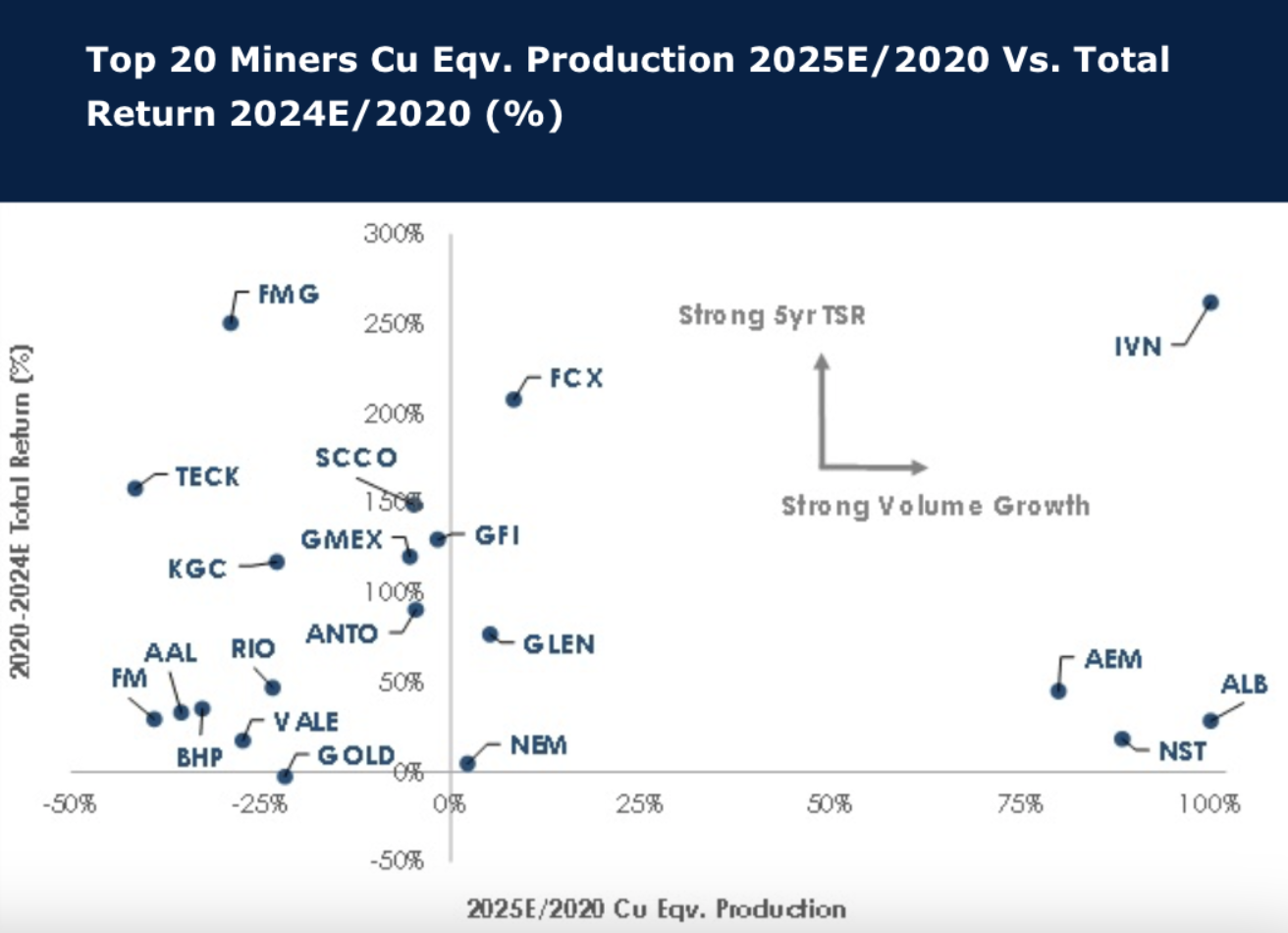

Large cap miners: Performance and growth are not related

As Sellside and Buyside set expectations for 2025, Global Mining Research examines the recent history of the leading miners. Interestingly, only Agnico Eagle Mines Limited, Albemarle Corporation, Ivanhoe Mines Ltd, and Northern Star Resources Limited are estimated to have materially grown through investment and M&A over 2020-2025E. In fact, most miners have shrunk in terms of Cu Eqv. Production, and exiting coal was a clear trend. The copper miners have outperformed, despite iron ore miners clearly returning the most cash to shareholders in dividends. Buybacks should have helped the share price return but there is little evidence this works. For over half the group, a ‘buy and hold’ strategy has not generated a robust return over the period. This reinforces the view that miners are to be traded.

A volatile but upward-trending market in 2025

With silver prices consolidating between $27 and $33 per ounce in recent months, Jeffrey Christian provides CPM Group's detailed forecast for silver markets in 2025. Jeff looks at investment demand for both EFTs and physical silver and discusses its importance and why it is the primary driver of silver prices, as well as the factors that influence it. The video concludes with a look at the macroeconomic factors driving markets, including inflation concerns, government deficits, and geopolitical instability across the U.S., Europe, and Asia, all contributing to heightened investor interest in precious metals. With projections pointing to a volatile but upward-trending markets.

Click here to watch.