Company & Sector Research

Europe

Following publication of its FY23 annual report, Iron Blue increases their ITV score to 31/60 (still top decile) from 29/60 to reflect: 1) FY23 cost strip outs hit a decade high. 2) Capitalisations of programme & other rights expanded +10% Y/Y, also to a decade high. 3) Increased use of provisions accounting. 4) DB pensions liability discount rate of 4.75% vs. 3.8% average. 5) A new contingent liability relating to the UK CMA investigation into non-sport TV content production and broadcasting. They also note that five of management’s principal risks were deemed to have increased Y/Y and FY23’s Oracle Fusion IT platform launch saw various processes and controls not operating as anticipated.

BHP + Anglo American = 0.5Mt more copper and a lot of baggage

In this 14-page report, GMR examines the potential BHP takeover of AAL. BHP would need to take a long-term view as AAL comes with ~US$11bn net debt and midterm FCF is very weak, plus uncertainty in several of its businesses including DeBeers. Fundamentally, GMR fails to see the material value opportunity for BHP in what appears to be a dilutionary transaction. How is this different from the large deals of the past which struggled to add value?

EU Towers: A rising risk from land aggregators

Cellnex and Inwit have recently pivoted towards buying more land. Why? In part because they still see a good opportunity to deploy capital attractively, but New Street believes this is also driven by a defensive angle against a gradually rising role of land aggregators in Europe. In this note, they explore in more detail for the first time the role of land aggregators in Europe and how it might affect tower companies in future. They also update some of their broader valuation parameters for these names too. They remain Neutral on the EU tower space at current valuations.

Forensic Alpha identifies several new red flags from AUTO’s annual report - their main concern is a change in accounting policy related to revenue recognition. It suggests the company may be recognising revenue from components at an earlier point in time - when the products are shipped rather than when they are delivered. This change may have inflated revenues in 2023 and resulted in an artificially high growth rate. You might expect earlier recognition of a sale to result in a reduction of inventory as it shifts from the balance sheet faster. However, they also identified a new flag related to increased DSI in 1Q24 (up 51% Y/Y to 225 days; represents over 7 months of sales).

Leveraging its fixed cost base - management's financial goals for 2025 are likely to prove too challenging, but as long as TomTom is capable of increasing its revenue and keeping strong control over its total cash spend, its EBITDA and FCF are expected to reach levels making the stock an attractive investment case. Under the IDEA!’s base case scenario, the company’s valuation multiples are estimated to arrive at 6.8x EV/EBITDA and 9.6% FCF Yield for 2025 and 3.9x and 17.4% respectively for the year thereafter. Investors can expect to see a rerating of the company’s share price when there is more visibility in new contract wins of its Enterprise entity.

North America

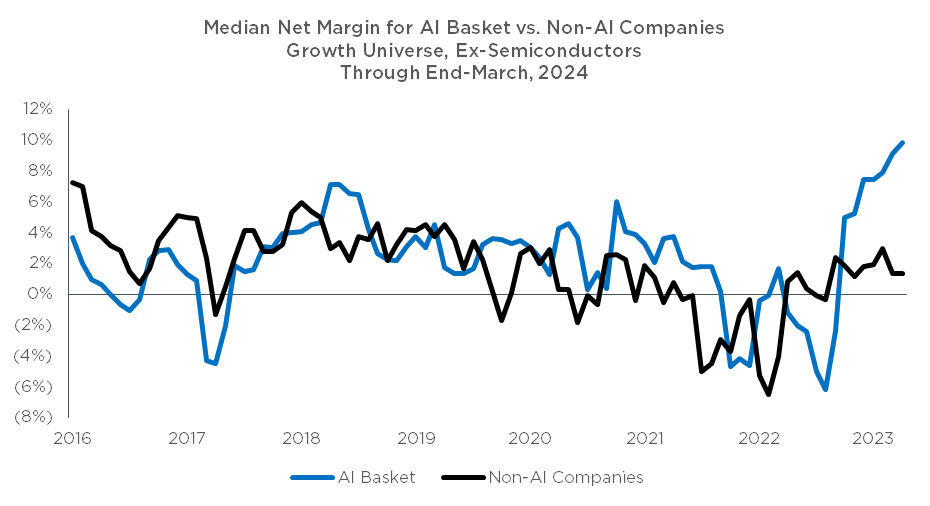

AI’s impact on corporate profitability

Trivariate Research created an AI basket by counting all the mentions of AI-related keywords (i.e., GPU, LLM) on earnings call transcripts. Among the growth universe, net margins for companies mentioning AI keywords in the Q&A portion of their earnings calls have already seen material margin expansion vs. those growth companies with no mentions, after the two buckets had highly correlated margin profiles for the median decade. This is enough data to conclude the relationship is not spurious - profitability is likely to go way higher for US corporates.

Dividend sustainability - it is the first, second and third question on the minds of BCE investors right now. While it is known that BCE will be at an elevated payout ratio for FY24 (~129% based on company guidance), Veritas initially estimated an adjusted payout ratio closer to ~170% after deducting lease principal payments, but they now think it will be closer to 200% based on annual disclosures that showed a $157m (18%) increase in annual lease payments. Even under optimistic assumptions BCE will still be above an adjusted payout ratio of 120% by FY27. There is limited financial flexibility to maintain the dividend long-term. The share price has fallen ~30% over the last 12 months but is still not cheap.

PTLO has <100 locations, is growing >10% annually, with solid margins (22% RLM, 11% EBITDA), attractive unit economics (25% ROIC) and trades at a discount to the value of its foreseeable growth as well as a discount to its peers. John Zolidis believes the group's transition to smaller format restaurants will lead to even better unit economics and further derisk growth. Using his estimates (near consensus), John forecasts up to 85% upside over the next two years assuming a modest growth multiple.

Smoke-free segments boosted Philip Morris and Altria’s numbers

Some Big Tobacco have recently delivered their Q1 results. PMI continues reporting its smoke-free momentum, announcing 25% organic growth in net revenues and 38% in gross profit - with strong contributions from Iqos and Zyn. On the other hand, oral tobacco continues to make a significant contribution to Altria’s numbers, as the company reported its results for the first quarter of 2024 with encouraging earnings from its On! nicotine pouch brand.

Tom Chanos turns bearish once again having successfully shorted the stock four times since Mar 21. Revenue growth has gone from +102% to +75% to +53% to +25% and is likely to be well under 20% in 2026. Maybe INSP can earn $1 per share by then. Those metrics would earn a P/E ratio of 50 at best, meaning this is a $50 stock three years from now (vs. $247 today)! Besides the ridiculous valuation, there are 20+ companies working on sleep apnea drugs. With INSP being a one product company, if any of those drug companies has a breakthrough, INSP would be in serious trouble. If the choice is a pill or a once per week injection vs. a $35k surgery, people will take the pill!

Even with the current stock price up 80% off the low on Oct 30th, following what Craig Huber believed was a significant overreaction to the 3Q23 earnings announcement, he recommends buying the stock at these levels trading at only 14.1x/12.2x his 2024/25 EBITDA estimates or 19.2x/15.8x adjusted EPS. Craig thinks Street estimates for 2025/26 are materially too low and will need to come up in the coming quarters. The US mortgage market has finally reached the bottom and mortgage recovery in 2025/26 should be quite robust. Cost savings from the transformation programme should also be very beneficial – Craig expects adjusted EBITDA margin improvement of 339 bps in 2026(E) vs. 2023. 12-month TP $96 (30% upside).

A lot of IT Services companies that are employee-heavy and not prepared for the AI revolution, will get displaced by hardware- and software-based solutions. ACN has ~750k employees. Revenue per employee is lower than a restaurant group like Darden. The entire share price move during 2023-24 was ACN pitching themselves as an AI solution company; they have been trying to buy the expertise by doing small acquisitions but why would anyone hire them vs. using Microsoft or Amazon? ACN has negative organic growth in a massive AI tech spending boom and trades at a bigger multiple than MSFT! TP $200 (30% downside).

Software revenue growth falls short of expectations and FCF misses in 2024 - some on the Street appear to have become more sceptical of the way IBM’s management has gamed its growth targets. Besides excluding acquisition costs from the FCF calculation, OWS notes that IBM moved its declining security software business from Software to Consulting in 1Q24 to show ‘strong’ Software segment growth. Over the past year, bulls have been arguing that the firm is an AI value play. OWS counters that IBM is no such thing. Revenue growth, whether from AI or otherwise, has been ~3% with acquisitions and the EV/FCF is 30x if one were to include acquisition costs. TP $85 (50% downside).

Questionable quality of 4Q24 results - 1) Revenue had an extra six days but only rose by $8m or 0.6%. MRVL also picked up $13.7m from lower deferred revenues. 2) Ramped up Variable Considerations - a $10m change is worth 1 cent in EPS. Did MRVL load up this account to help sales and EPS going forward? 3) Accrued Warranty Expense fell - $26.9m potential boost in income or 3 cents in a quarter where MRVL only met estimates. 4) Adds back stock compensation - rose to 10.9% of sales - 2.6 cents to non-GAAP EPS. 5) Adjusted EPS also added back $42.3m in product claims that were paid out - 4.6 cents and is not expected to recur going forward. 6) Cuts to R&D spending.

ZBRA surpassed expectations in 1Q24, driven by substantial growth in significant retail mobile computer deals. While management remains cautious about labelling it a widespread market recovery, the strong results and improved visibility into the backlog prompted the company to increase its full-year guidance. This outcome should be considered a win for investors. Consequently, Northcoast raises their price target to $350, anticipating further positive developments. Their financial estimates for 2025 are conservative, and although they may appear optimistic compared to consensus estimates, they believe the market underestimates this company's potential.

Japan

Making waves again - Yamaha was trading at ~40x earnings when China decided to start cutting educational budgets that had been the bedrock of the world’s largest market for Classical pianos. The stock has since dropped 56% (vs. Topix up 37%). While earnings missed consensus estimates by an average of 25% over the subsequent 5 quarters, Mike Allen thinks the consensus has begun to overcompensate. The Chinese Piano market is not going to recover, but analysts are overestimating its importance - it probably accounts for less than 2% of Yamaha’s total sales - and are underestimating the company’s ability to cut costs and drive top-line growth through other avenues.

Yurtec is a construction company of electric power facilities. It is a beneficiary of increased power consumption, reshoring manufacturing and the surge in construction activities, particularly due to government-backed offshore wind power and solar projects. The firm boasts a robust balance sheet with ¥27bn in net cash, leaving it well-equipped to finance its expansion initiatives. The share price jumped c.15% post FY24 results and are up 35% YTD, but still trade at a low PE of 13.3x for FY25E and PB of 0.76x. Yuka Marosek believes Yurtec can catch up with industry leader, Kyudenko, which trades at 17.7x PE. Under this multiple expansion scenario, the shares offer 30% upside.

Emerging Markets

Iii’s interactions with DSAs (Direct Selling Agents) raises alarms with regards to the company’s lending practices especially in the affordable housing segment. While affordable housing as a total book may be small, Iii anticipates pressure on NIMs and growth. Recent regulatory actions involving companies like Kotak, IIFL and Paytm have resulted in substantial declines in their respective stock prices.

Following the release of PINFRA’s FY23 results, Robert Crimes updates his long-term model forecasts - his price target of MX$343 offers nearly 100% upside. The investment case focuses on 1) An attractive mix of mature assets and newer developed assets ramping up. 2) High EM traffic growth (+2.9% CAGR in 2023-35E). 3) Strong returns in Mexican toll roads - EBITDA margins of 79.6% in 2023 (LT EBITDA growth of +6.0% CAGR in 2024-40E). Toll road opex is low and Robert estimates average construction costs per km of c.€7m, to be 1/3 of Europe but tolls per km of €0.07 only 1/3 less. 4) High IRR guarantees. 5) Rising dividend yield - from 3.1% in 2023 to 5.5% in 2025E and 13.0% in 2030E.

Propitious Research

Indian IT Services: Where are we in the growth cycle?

The large Indian IT services companies experienced an elaborated revenue growth cycle from the Covid pandemic lows peaking during mid-2022 with above-average constant currency Y/Y growth rates. This was followed by a sharp correction during 2023 with Wipro significantly underperforming its peers. Infosys has also lagged both Tata Consultancy Services and HCL Technologies. While 4Q24 results recently showed the first signs of a bottoming in the growth rates, leading to anticipation in the market that we should see an acceleration over the medium term, based on current valuation levels Wium Malan finds very little upside for these stocks.

Production and deliveries tracking ahead of expectations - Blue Lotus sees SU7’s success stemming from its attractive design, class leading range / acceleration and compelling price point. SU7 gross margin guide suggests pricing strategy is sustainable for Xiaomi’s next vehicle, an SUV launching in early-2025. As a result, Blue Lotus upgrades the stock to Buy. They increase their EV profitability estimates and expect market share to expand. They raise their unit volume estimates for 2024/2025/2026 by 48%/14%/14% to 99k/240k/450k, respectively.

Macro Research

Developed Markets

Totem Macro

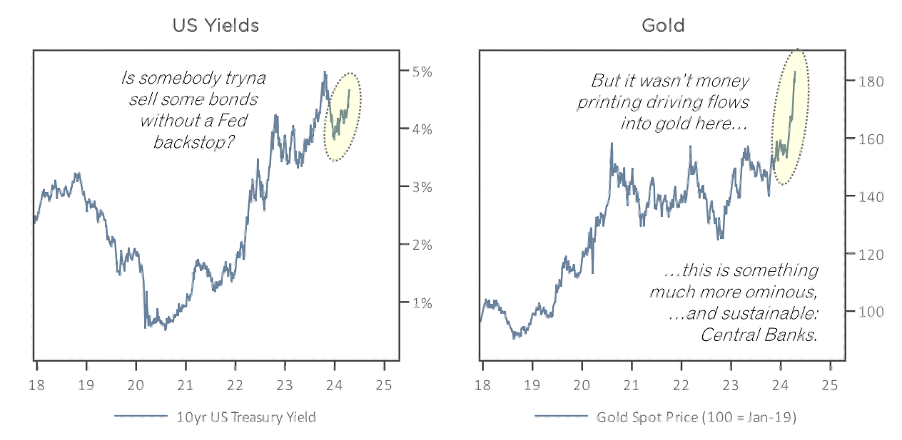

Hyper-financialisation

As Whitney Baker expected, monetary contraction has occurred in Q2 (which she expects to reverse in Q3), the Japanese reflation narrative is at its peak, and there is a new wave of US duration supply, leading to higher yields. Yet, there appears to be a non-linear rise in gold prices. The metal is seen as a crucial investment, driven by unreported central bank purchases and reserve holders diversifying away from US paper assets. US yields will not be allowed to surge uncontrollably, with money printing to come back into action in response to foreign selling of US assets. In her latest report, Whitney explains why she is conceptually SHORT the fiat-funded hyper-financialisation and why she sees deeply bullish signs for gold as the dollar weakens and economic imbalances unwind.

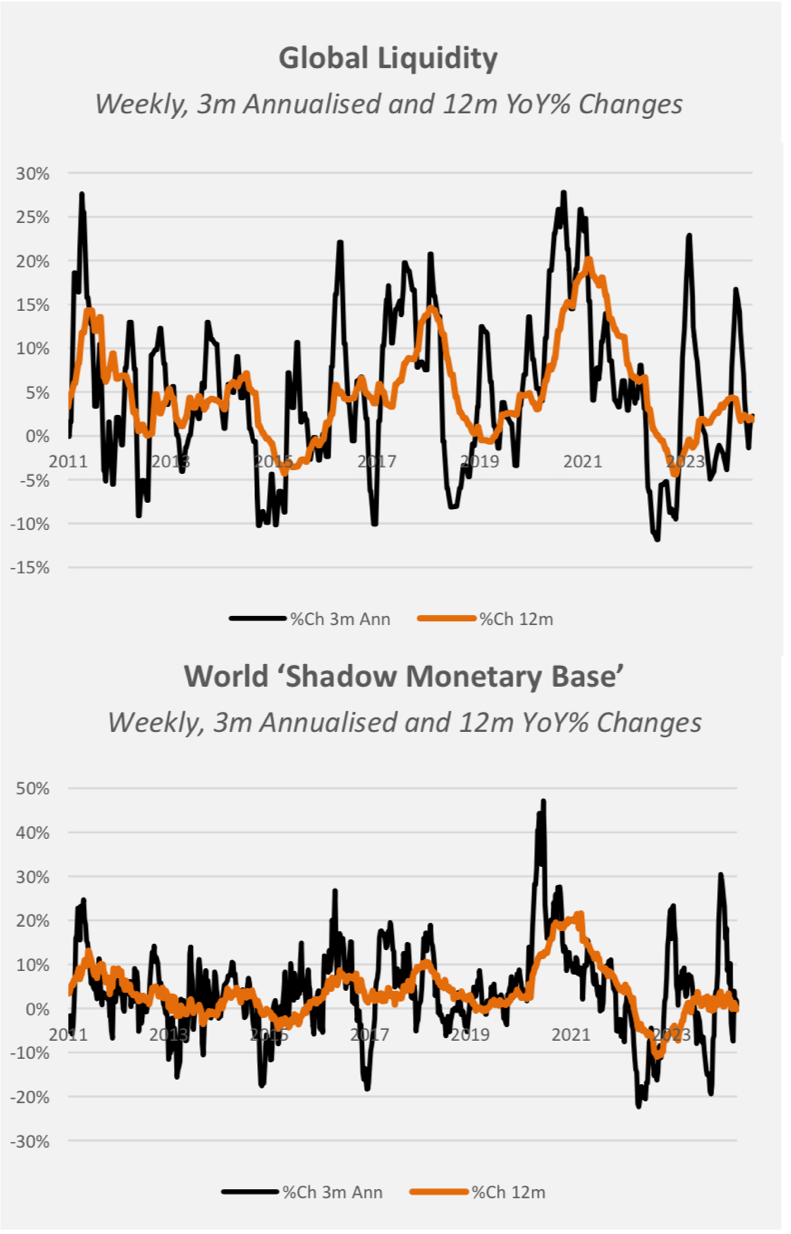

In the shadows

Latest weekly measures derived from central bank balance sheet data showed global liquidity growing at a 2.3% 3m annualised clip. This isn’t the full story; the improvement is due to a base effect. In nominal terms, it actually slipped by US$86bn last week, with the Shadow Monetary Base acting as the main driver. Four of the five major central banks are involved but the largest footprints are those of the US Federal Reserve and the People’s Bank of China. Collateral values have also slipped. Michael Howell had warned of a Q2 2024 dip in liquidity, but he continues to expect liquidity conditions to improve in the second half of the year.

Euro area inflation

Riccardo Trezzi estimates that in April the core harmonised index of consumer prices (HICP) grew 22-24bps MoM (sa). This brings the 3m/3m (ar) to 2.5%. The 3m/3m (ar) is marginally below the YoY, signaling that the annual variation should moderate further in the coming months. However, the 3m/3m is now going sideways (or in moderate acceleration), therefore the 2.5% appears as a reasonable target for the YoY going forward. Overall, the issue remains the same of recent months: yes, the EA is disinflating, but the current most likely scenario is for the YoY of core HICP to reach 2% but then rebound up in H2. An important factor is the persistency of HICP services.

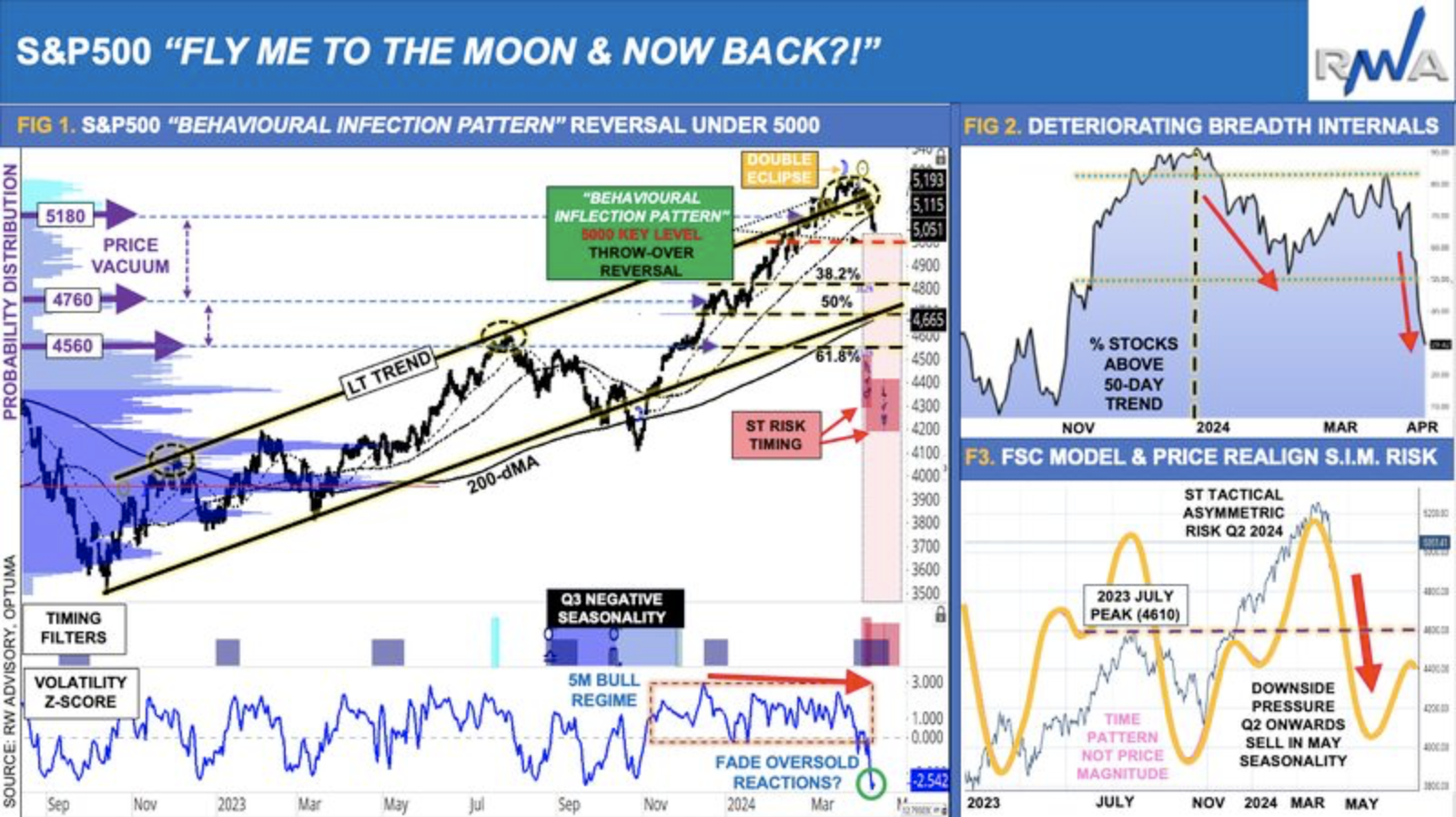

US: Behavioural inflection point eclipsed

S&P500 confirmed a major distribution pattern, which reversed under the long-term rising trend, turning again back into the 5000 psychological level. A triple whammy of headwinds is now weighing heavy, notably the unwind from momentum extremes, rotation fragility and cycle risk – all warning of an impending correction into Q2 2024. Expect a minimum 10% correction, with overshoot risk. Meanwhile, consider tilting a barbell strategy, with more profit-taking and astute downside protection. In parallel, build up robust defensive plays, such as outperforming gold, now due some respite; cash, quality bonds and non-correlated portfolio risk. Read RWA’s report for more tactical guidance.

GFC Economics

US: Big tech’s spending

The headline GDP figure for Q1 came in below expectations but the underlying numbers were strong again, especially in the core PCE index after it rebounded by an annualised 3.73% q/q in Q1, well above expectations. The 2-year treasury yield now sits at 5% as the market prices out all rate cuts this year, pulling up the long end of the curve. Multiple FAANG members saw significant capex jumps, with Microsoft’s up 79% y/y and Meta’s forecast raised by an additional $5bn+. It is difficult to envisage a slowdown in the US economy, claims Graham Turner, given the strength of tech capex and consumer spending on services. The strength of the US economy will force Europe and other economies to take a bolder approach.

US Equity Strategy: A healthy pullback

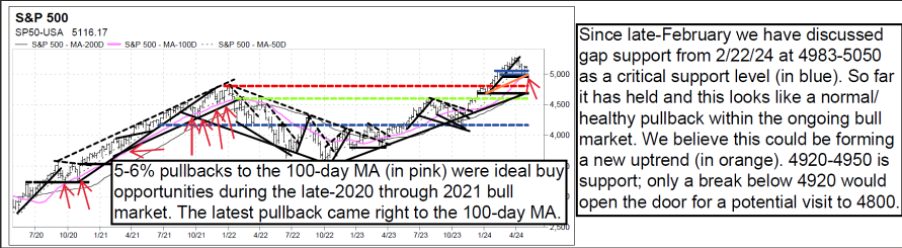

While we are not yet out of the woods, the Vermilion team continues to see evidence that suggests the lows may be “in” for this pullback. Last week they discussed the possibility that further downside was limited on the S&P 500 for a multitude of reasons. Considering that the market dynamics remain unchanged and that broad market indexes have staged strong bounces since, the team continues to view the latest pullback to the 100-day MA on the S&P 500 as healthy and normal within the ongoing bull market. 5-6% pullbacks to the 100-day MA on the S&P 500 provided ideal entry points throughout the 2021 bull market and this pullback may be no different.

Japan: Slipping lower

The BoJ unanimously voted to hold rates at 0-0.1% and revised up its estimates of inflation and cut growth forecasts. Governor Ueda continues to dangle the prospect of more rate hikes to come, and an October hike remains Niall Ferguson’s base case. Still, JYP has fallen below 157 to the dollar, the weakest point in nearly 40 years. The risk of currency intervention remains high, but if the Finance Ministry steps in, the broad trend of slow yen depreciation seems set to continue. Niall remains SHORT the yen.

New Zealand: Valuation reset

NZ equity valuations have reset notably off the highs, with the composite PE ratio at decade lows, contrasting with Australia and the US. Dividend yields have rebounded, which Callum Thomas explains is important for this traditionally yield focused market, although high rates mean fixed income alternatives have the edge from a running yield standpoint. Equities enjoy structural tailwinds from KiwiSaver flows and increased retail participation, and economic confidence and earnings revisions sentiment are on a recovering path. Yet, the housing market remains a swing factor and high rates a hurdle.

The growing risk for NATO

Brunello Rosa recently published his latest article titled ‘Growing Risks for NATO’s Article 5 as the Cornerstone of Post-WW2 Global Geopolitical Equilibria’. He discusses the conferences and treaties that posed the basis of the post-WW2 global equilibria; the key role played by NATO’s Article 5; the de-facto extension of Article 5 to Taiwan; the credible threat of the US’s departure; why Article 5 remains the cornerstone of global security; and why isolationism in the US is not compatible with their role of ultimate guarantor of the world’s geopolitical equilibria.

Emerging Markets

Chinese overcapacity and the New Protectionism

China has become the world’s leading industrial power at a historically unprecedented speed. Using massive state subsidies, it has leapfrogged from textiles to becoming the world’s largest producer of an array of finished goods. It controls much of the upstream capacity for the inputs crucial to modern manufacturing. Without real estate as an economic driver, China is now doubling down on its manufacturing sector. However, without substantial reforms to boost China’s domestic demand, the outlet for China’s huge industrial capacity will be world markets. In the early 2000s, policymakers in advanced and emerging economies alike did not act fast enough to stop premature deindustrialisation. A loss of faith in the WTO and increasing security concerns mean this time they will turn to trade protectionism and retaliatory industrial policy.

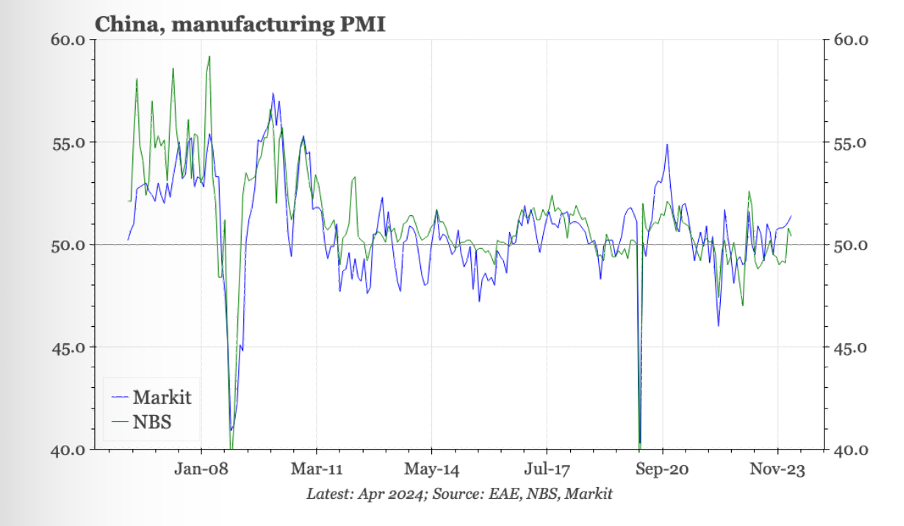

China: Exports lift the PMI

After the sudden spike in March, the official manufacturing PMI dropped back in April. However, it remains above 50. The S&P version strengthened further, with the PMI now high enough to be suggesting that the cycle has real momentum. The stand-out detail of the S&P survey is the strength of export orders, reaching a level rarely seen in the last 10 years. Paul Cavey sees some improvement in the domestic cycle too, but the picture is more mixed. Most encouraging is the pick-up in pricing, fitting with Paul’s reading that a lot of the weakness in PPI is cyclical rather than structural. With signs of the food price cycle now over, Paul thinks the worst of the deflation scare might now be over. However, the pricing trends look more like a troughing-out than a real pick-up, which rings true for other economic indicators.

Brazil: Say goodbye to the fiscal anchor

The Brazilian economy expanded for a fourth consecutive month in February and Marcos Alberdi lifts his 2024 GDP forecast from 1.8% to 2.1% in light of improving LatAm exports and terms of trade. A surge in revenues has helped the government disguise a fiscal slippage. Marcos expresses concern that this stems from a one-off jump in tax revenues. Moreover, the government’s forecasts to comply with new fiscal targets are unrealistic and debt to GDP will rise in coming years. Inflation edged inside the target band but some prices remain sticky and Marcos expects the central bank to make the easing cycle shorter, leaving Brazil with a very high ex-ante real policy rate.

Nigeria: The known and the unknown

Nigeria has let the currency go and has hiked rates to support it. The NGN rate has remained unified with the black market rate this year, the central bank has hiked rates sharply and the backlog of US dollar orders is clearing. The combination of FX weakening and financial tightening is not great for domestic demand, but it has put the external balance back in surplus. However, inflation is still rising, fiscal deficits are still wide and it’s too early to gauge how serious the government is on funding, revenue and subsidy reforms. Jonathan Anderson isn’t sure about local assets, but he maintains his dollar sovereign position as he continues to see value in hard currency debt.

West Africa: The lasting impact of regional fragmentation

Fractures are growing within the Economic Community of West African States (ECOWAS), exacerbated by distrust, including recent accusations by the Burkinabe military ruler that Cote d’Ivoire is actively harbouring destabilisers of his home nation. As Russia’s alliances deepen within Burkino Faso, Mali and Niger – the so-called alliance of Sahel States – these countries are experiencing a growing distrust of their Western-allied ECOWAS counterparts. Ripple-effects from the situation are starting to be felt as regimes in Chad and Guinea grow closer to Moscow, although to a lesser extent. These developments could end up in the culmination of a proxy war between the West and Russia in the sub-region, damaging the prospects of political stability, regional security and economic integration.

Commodities

The future of tokens

The mass adoption of Bitcoin could soon be followed by other prominent tokens such as Ethereum, claims Warut Promboon. This adoption of mainstream cryptocurrencies will lead to the adoption of real world asset (RWA) tokens, especially tokenised debt. He is positive on tokens backed by risk-free assets such as US Treasuries, however, RWA tokens based on liquid assets should not be the target of most investors since those liquid assets are already widely available in traditional financial markets. As such Warut sees a dynamic market for private and illiquid assets to be tokenised for the masses in the near future. In his latest report, he explores what is next for the private debt token world.

Bitcoin: Weakness in between the lines

The inflow of funds into Bitcoin ETFs, which resulted in the latest price rally, has dried up over the past 4-5 weeks. According to Markus Thielen, the market internals have become weaker, with funding rates decreasing significantly, indicating a lack of speculative demand. The upside drivers for Bitcoin are no longer present and the market is facing a risk-off environment, leading to a potential correction to the mid-50,000s. The impact of the Bitcoin halving event may not be as bullish as previously expected, and macro factors, such as high inflation and interest rate hikes, have a more significant impact on the price. Bitcoin has not performed as a hedge against inflation and geopolitical risks, as it has sold off during these events.

Gold in the charts

The bulls are failing to convince, at least for now. This week saw a sell-off to 2296.2, extending to 2291.7. Clive Lambert has bold supports at 2262.3 and 2228.4 – for now he’s classing this at a retrace but should those two break it could be something bigger. The MACD also turns bearish and the RSI now lies in the 40s after briefly hitting the 80s. Clive is short-term neutral – bullish. He favours 2-way trades for now, preferring LONGs, and sees 2478-2500 next, just not for now.

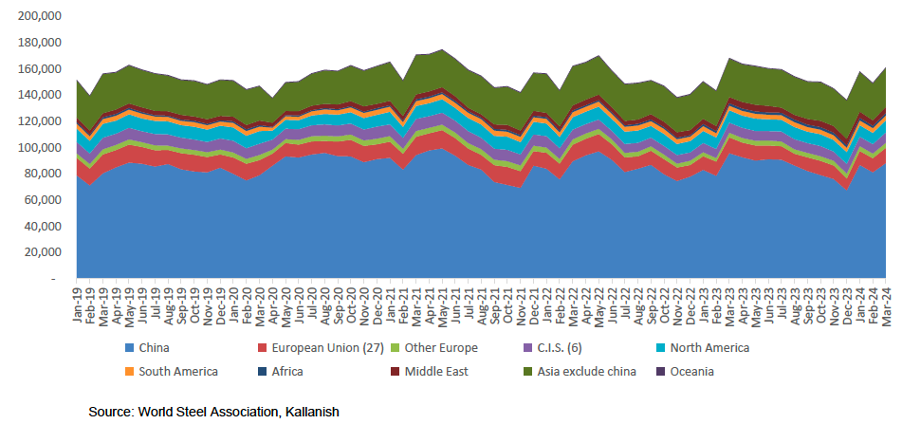

Chinese Steel: Under pressure

Steel prices in China have seen a mild recovery from multi-year lows, but the overall demand outlook for the year remains very challenged as local government infrastructure spending sees a significant contraction and housing activity remains depressed. While steel exports have been a key tool to alleviate the oversupply pressure domestically, Ian Roper comments that an increasing number of trade measures against China will limit this impact. He believes steel production to have risen around 4% last year versus officially reported flat year on year output (see chart). Thus, steel output cuts will have to be seen through H2 as domestic demand deteriorates further.