Company & Sector Research

Europe

ESG report - MAB outlined the progress made with its three sustainability pillars in FY23 but its KPIs and metrics were lacking in scope and depth. CEN’s MAB score (39/100) remains below the F&B sector median. Environmental highlights included the submission of a net zero roadmap for SBTi approval and increased engagement with suppliers on sustainable packaging. Despite scoring revisions, Social was on par with the sector median. The company updated its animal welfare policy, completed modern slavery risk assessments and created strategic partnerships with charities. Governance saw the only positive y/y change thanks to alignment with the UK Corporate Governance Code. MAB plans to include a sustainability objective in executive LTIPs from FY24. Click here to access the full report.

RKT’s share price plunges to its lowest level in a decade following the Enfamil court case defeat. The market seems to have been caught totally unawares as the verdict triggered fears that RKT would face more financial liabilities from lawsuits related to the baby formula. However, Iron Blue had flagged this issue to clients last year when they highlighted additional risk commentary around a new contingent liability (US baby milk liability actions) and they also included it in their question list for clients to ask management more about. It is why one of the many things Iron Blue focuses on is y/y changes in annual report disclosures.

Inventory of finished goods has grown by 33% y/y (vs. 21% growth in revenues). Based on Q4 COGS, the DSI of finished goods has risen from 33 days at the end of FY22 to 41 days at the end of FY23. This may not seem like a large increase, but in an industry focused on “Just-in-Time” manufacturing, this is a significant move up. Whether this additional product can easily be absorbed into the market will depend on your view of demand in 2024. In any case, Forensic Alpha recommends investors to continue tracking inventory in coming quarters.

Having turned bullish on the stock back in Oct 23 in a report titled, ‘The upside everyone is missing in European banks’, in his latest piece, Erik@YWR highlights the path to £3.00/share (+65%) and beyond. Key catalysts include: 1) Upgrades to earnings forecasts. Erik’s EPS estimates are significantly ahead of consensus at 38p (2024) and 44p (2025). 2) Rebound in investment banking revenues after a 2-year downturn. 3) UK driven profitable growth strategy. All of this leads to a more consistent business, with less volatility and higher ROE’s, which is why Venkat can stand up and promise to return £10bn in dividends and share buybacks through 2026.

UK Mid Caps: Cheap Tech

Basic metrics for Willis Welby’s UK mid cap Tech coverage remain compelling - financial productivity is universally strong, the median implied to Y3 EBITM ratio is just 66 and the median consensus Y3 revenue growth is 9.1%. Highlighted stocks include Moneysupermarket - boasts a great balance sheet, decent growth and an implied to Y3 EBITM ratio of just 45. This share price would not feel strange 50% higher. Kainos - impressive growth model with good returns, a strong balance sheet and a cautious share price. The implied to Y3 EBITM ratio is back down at 66. This combination warrants a further move of 30%+ and a share price of at least GBP 14.00.

North America

Are small caps the alternative to the Magnificent 7?

Investors buying small caps as a defensive strategy is not the right move, according to Adam Parker - only once since 1986 have they outperformed when the S&P500 falls >10% (2000-2002) and his judgment is that we are not in a second TMT bubble. Small caps will not outperform in a down tape unless the Mag 7 earnings collapse at the same time the gross margins of the average small cap company expand. Possible, but not his base case. He sees the Mag 7 continuing to perform well. Valuations are high, but not offensive, and they are growing faster than the market and have better balance sheets and margins. There are plenty of small cap companies where margins can expand - Adam recommends owning low beta, high quality stocks in growth, and value stocks where fundamentals are turning.

Bear’s Den Idea Forum

Common themes from MYST's latest buy-side event focused on cyclicals / companies trading at peak, potential “Trump losers” and companies facing inventory headwinds. The most compelling ideas include:

Bentley Systems (BSY) - Mining / renewables weakness to curb ARR growth; Trump could threaten IIJA tailwind.

Powell Industries (POWL) - Absurdly valued, highly cyclical business with peaking fundamentals & large insider selling.

Starbucks (SBUX) - Litany of earnings headwinds not fully appreciated under “abysmal” new CEO.

Toro (TTC) - Recent FY24 guidance a “Hail Mary” amid rising DSO’s / Inventory Days.

Having successfully shorted DASH several times in 2022, Tom Chanos turns bearish once again. The stock has gained more than 200% off the low price of $43 in Oct 2022 and is up 125% in the past year. However, with short interest now less than 4%, Tom says there are no shorts left to squeeze, just as the business begins to slow dramatically. He argues Wall Street estimates are far too bullish and by the time DASH reaches breakeven it will have pedestrian top line growth at best. No one pays 100x EPS for single digit growth. A 40x multiple would be very generous which would put the stock at $45.

Online Sports Betting / iGaming: Eyes on the prize

Arete sees the US OSB market growing revenues 6x by 2035E and looks likely to develop into a de facto duopoly. They assume FanDuel (Flutter) and DraftKings will take 70% combined share of handle and 75% share of revenues, with higher structural hold than rivals. Similar story in iGaming; the two companies are using product innovation to take share from legacy casinos and look on track for ~50% combined share, with upside from M&A. Arete has street high price targets for both names. DKNG offers the most upside (~100%) with Arete’s revenues delta vs. consensus improving from +8% in '24E to >30% by '26E, resulting in EBITDA estimates 42% and 51% above consensus, respectively.

Kevin Kwilinski is not a long-term focused CEO and is likely to falter because of his deeply-flawed people skills - his biggest weakness, interpersonal communication, will be a major impediment to his ability to get things done. 1) Even the best laid plans struggle to come to fruition when the team is not committed. 2) He has stated an intention to expand globally but he may not be conscious of cultural nuances when forging partnerships. 3) His abrasive decision-making has jeopardised client relationships in the past. 4) His tendency to blame others and push the boundaries of acceptable business practice leads to attrition and lack of trust, even from investors.

Verbatim Advisory Group

Feb sales trends are significantly stronger than Jan and 4Q23 trends, according to Verbatim’s latest channel checks. Higher prices, product availability, warmer weather and promotions are the major factors driving Traffic and Ticket counts. Home improvement, gardening and cleaning are among the top selling product categories. Respondents indicate that their stores are either gaining or seeing no change in their market share and that prices are mostly increasing at an average of 2-3%. Hiring is easier, while wages are trending up. Online ordering is increasing y/y. Verbatim’s HD US Feb Comp Estimate is 0.0% vs. 4Q23 Actual Comp of -4.0%. Click here to access the full report.

The sneaker / active world comes undone

As Nike finally takes steps forward it seems as though its neighbours are falling apart. Adidas has had a hit shoe (Samba) for a few years, yet it has not changed the momentum for the brand. Allbirds, should never have gone public, is retrenching. Kevin Plank is back at Under Armour and the CEO of Brooks is stepping down. Retail Tracker’s thesis: 1) New competition from ON / Hoka has hit several brands hard, while Alo, Gymshark and Vuori have appealed to younger men (and women) as an alternative to UA and ADS apparel. 2) Fashion has changed and with this change comes a change in footwear - for women this means a shift to loafers and ballet flats vs. sneakers. 3) We have not had a new trend in active / sport with white shoes trending for too many years. Bring back some colour and fashion!

Market confusion surrounds its true earnings power - WLK has been very active on the M&A front recently and now generates around two-thirds of its earnings from chlorovinyls. Since hitting its Mar 2020 lows, its share price, while keeping pace with ethylene/polyethylene-biased name LyondellBasell, has significantly underperformed the company’s main chlorovinyl peer, Olin. Hassan Ahmed believes this underperformance is unwarranted and makes the case that WLK has been acquiring businesses that have a far more stable earnings profile, which should reduce the company’s overall cyclicality and result in a multiple re-rating.

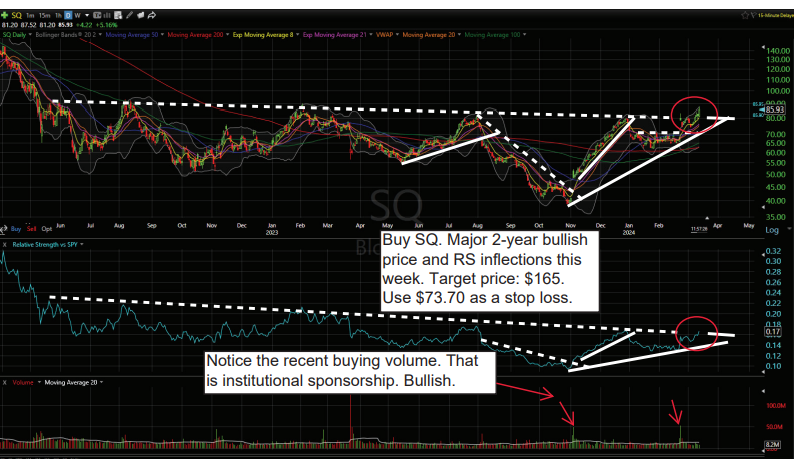

The technicals suggest the rallies in SQ and Affirm are just getting going, according to analysts at Vermilion Research. Both stocks are emerging from 2-year bases with volume patterns that are consistent with institutional sponsorship; this is a huge reason why they believe now is the time to be buying. They see potential to make 100%+ price gains in the coming months / year(s), while the max stop loss would be 10-15% based on technical invalidation levels.

The must-have name in the AI space - KC Rajkumar sees MU rivalling AMD’s market cap in the next 12-18 months. As KC predicted, MU blew away investor expectations, not merely by beating and raising quarterly numbers, but by providing a qualitative outlook for revenue / margins into Cy24 and Cy25 - unimaginably impressive for what is supposed to be a cyclical business. Not even Nvidia has been able provide a two-year outlook. Agnostic to AI chip suppliers, and increasingly a pure-play in AI, renders MU more attractive, at this stage in the investment cycle, to the likes of NVDA, AMD, Broadcom and Marvell.

While SPR’s field contacts mostly support the views discussed in PANW's recent earnings report, they also found a few factors that the company did not highlight. Issues include “security fatigue” that is resulting from time needed to implement all the tools that end users have purchased, but in PANW’s case, channels also see this fatigue resulting from overselling of ELAs. Industry contacts flagged competitive pressure (especially in cloud computing) and also helped to explain the delays / forecasting issues in PANW’s Fed business. On the opportunity side, all agree that the company has one of the most competitive security platforms, while its product and pricing strategy positions it well to compete for the Next Gen SIEM opportunity that is just starting to open up.

Acquisitions of TASK Group and Stuzo Holdings accelerate PAR’s cloud-based unified commerce platform into convenience stores and fuel retailers, as well as new international markets. The acquired businesses add $80m in ARR (to $137m ending 2023) and are expected to add $20m adjusted EBITDA, bringing PAR to adjusted EBITDA profitability ahead of its previous goal by the end of 2024. Sidoti upgrades the stock to Buy and increases their TP to $61 (40% upside).

Japan

Despite an upgrade to EBITDA guidance at Q3 results, shares of LY Corp remain mired in a slump as a near perfect storm of worries, ranging from competition to data security, have arisen in recent months. However, Kirk Boodry thinks these concerns are largely overdone, whilst his investment thesis, that ID integration and PayPay growth can support growth in the core businesses, remains intact. His new TP of ¥560 implies potential upside of 40%. Kirk assumes 6.7% consolidated annual revenue growth through 2030. Annual EBITDA growth is slightly faster at 9% as margins expand on cost efficiencies and fintech’s progression to profitability.

Emerging Markets

A ban on TikTok will have a profound impact on Chinese Internet companies

Blue Lotus believes the optimum strategy of the Chinese government is to facilitate the shutdown of TikTok in the US, make a global mega-app only available on Huawei phones and spur a global “guerrilla war” against US ideology. This leads them to believe that: 1) Alibaba (recently upgraded to Buy) will benefit from TikTok’s US shutdown by gaining momentum in its international ecommerce business; 2) Tencent will benefit from levelling the playfield against TikTok in user and usage bases for AI / LLM applications globally; 3) PDD and Shein might benefit in the short run but less so in the long run, due to their own compliance deficiencies in tax adherence and privacy protection.

Following the stock’s 40% jump over the last three years, BOA has exhausted its upside, according to AlphaMena, whose valuation methods now flash red. The fruitful African expansion seems to be fully priced in and investors are looking for a new catalyst. Why not a new bold move by targeting the attractive and large Egyptian market? While BOA trades at a discount to the sector on both P/E (18%) and P/B (12%), this is warranted because of its low ROE and dividend yield (at 10% and 2.4% vs. 12.5% and 3.4% for its benchmark, respectively). BOA is fundamentally expensive amid an anticipated near-term reversal in monetary policy.

M N Ravi Chandra (VP of Operations since 2004) sold 5,000 shares at INR 1,730, cutting his stake by 50%. This is only his second sale, and whilst smaller in size than his prior timely sale of 7,000 shares in Aug 21 at INR 4,035, it is concerning to see him selling at less than half the price. K V G K Raju (CTO since 2021) sold 7,992 shares at INR 1,790, reducing his holding to zero. There is no news that he is leaving. Moreover, P Balaji (Head of Logistics) sold 1,000 shares at INR 1,764, cutting his holdings in half at the lowest price he has sold shares. This is a concerning cluster of sales from key officers and all have good overall records as sellers.

Macro Research

Developed Markets

UK: What Labour really thinks

Helen Thomas perceives the Rachel Reeves Mais Lecture as quite radical, far more than the newspaper briefings suggest. Her focus is on growth, propelled forward by securonomics – rather than getting out of the way, the government will provide workers and business owners with a safety net. Helen thinks it all sounds a little bit like a QE bazooka from central banks. To some, it looks like this is just another centrist, quasi-Blairite, Sunak-esque paean to liberalism. This couldn’t be further from the truth. Reeves has a far more radical approach, arguing that unfettered capitalism undermines democratic values and that workers need more rights and security. This is starting to look further and further away from Sunak’s voters who don’t like big government. The alluringly centrist rhetoric may in fact be far more radical than believed.

Europe: A defence renaissance?

Europe once had a large and advanced defence industry. Yet a deep and sustained decline in defence spending following the Cold War has severely diminished its capacity. To remedy the situation, Europeans need to raise defence spending, purchase more “made in Europe” arms, and reverse industry fragmentation. Niall Ferguson believes that on all three fronts there will be some progress over the coming years, notably by adopting a sizable debt-financed EU fund to support Ukraine and boost arms production. However, the reality is that the EU must continue to rely on the US as a security guarantor for the foreseeable future. The upside to going long European defence may be limited in the medium term.

US: Trump’s potential cabinet plans

Trump has clinched the 2024 GOP presidential nomination. The Electoral College outcome will hinge on just a half-dozen battleground states: Arizona, Georgia, Michigan, Nevada, Pennsylvania and Wisconsin. Trump’s victory in this year’s race for the Republican nomination begs the question of who would serve in his second administration. Trump has never been a detail-oriented policy wonk. Aside from a few key policy areas such as trade, his appointees will likely have significant room to run. Perhaps the most important appointment is who should lead the Federal Reserve when Jay Powell’s term as chair expires in 2026. Whoever is chosen, it’s possible that a Fed chair nominee closer to Trump may not take Powell’s dogged approach to asserting the Fed’s independence from the executive branch.

US: Positioning around fiscal and labour hoarding

After an interminable wait, Godot has showed up in Tokyo. The decision to abandon negative interest rate policy had been well telegraphed

US: Litmus tests

Alex Haseldine’s (smoothed) series for upward earnings revisions in the US bottomed in mid-November 2022, just before the launch of ChatGPT. Meanwhile, 30-year Treasury yields peaked on the 20th October 2022. At their highs last week, the S&P500 was up roughly 40% from the October 2022 trough, while the Nasdaq was up nearly 70%. In effect, that stunning rally has been driven by an unexpected cocktail of better economic growth, rising earnings (turbo charged by the arrival of generative AI) and falling bond yields. No wonder investor sentiment readings are now very bullish. To justify the current level of optimism, logic would suggest that either the Fed needs to hurry up its easing program, or growth needs to re-accelerate, or both, which is potentially thinkable only if inflation resumes its downtrend.

BoJ and RBA rightly dovish, but still a bit optimistic

Manoj Pradhan comments that being dovish is exactly the right choice for the two central banks, but both were still a bit too optimistic on rising real wages being able to lift consumption. The BoJ has a longer wait before the output gap turns positive and it will need to tread carefully with any rate movements given the role of FX in the economy. The RBA will have to ease by much more than its rhetoric and market pricing suggest, with an outcome similar to the US but without a growth profile to match. Manoj is staying LONG MXNJPY (Banxico will stay hawkish on services inflation and strong growth). He also recommends to stay received Aus 1y1y or 2y1y. For the RBNZ, it is time to recreate a flattener (i.e., add a payer for 2024 to the existing 1y1y receiver).

Japanese yen is vulnerable despite policy shift

After an interminable wait, Godot has showed up in Tokyo. The decision to abandon negative interest rate policy had been well telegraphed, some might say well leaked & the announcement therefore surprised nobody. Yet as Ueda and his BoJ colleagues must have known, maintaining JGB purchases or the threat thereof, plus offering no guidance on a hiking cycle could only have one result: yen down. James Aitken believes that Japanese wage negotiations already argue for more hikes; but until the BoJ’s monetary policy board articulate a strategy for further hikes, any threats from the MoF to intervene to support the yen will lack credibility.

Emerging Markets

EM: Things are looking up

At the start of the year, Callum Thomas commented that EM prospects were positive for the year ahead. He understood why investors would be sceptical, especially after so many looked upon EM favourably at the start of 2023, but things are different this time. Three months on and his view is unchanged. Sentiment is improving on Emerging Markets, and things are truly getting better (Fed peak, EM central bank pivot, relaxed risk sentiment and global growth reacceleration). Meanwhile, EM equities are still cheap.

China: The government’s confident narrative

In explaining the Jan-Feb data, the government's narrative on the economy has two components: growth is strengthening and quality is improving. Paul Cavey believes the Chinese economy has been stabilising and has previously highlighted the strong competitiveness of the country’s manufacturing sector. However, there is still something of a disconnect between these growth rates in specific industries and the overall performance of the economy. That can be seen most clearly in the industrial production data, which grew in Jan-Feb at an annualised rate of around 10%, the fastest since the initial covid recovery back in 2020. In terms of sectors, the improvement is most obvious in intermediate industries like metals, rubber and chemicals. That feels rather old economy.

China: Energy, durables and exports support restocking

Jan-Feb macro activity points to a solid growth in export rebound, manufacturing capex and energy-related infrastructure investment against a deterioration to housing construction. On the surface, policymakers should be satisfied with this batch of data and this could make them complacent towards growth support and supporting the RMB exchange rate. However, weak domestic demand and the property sector remain major concerns. William Hess expects a push for an acceleration to public housing construction and further eases in policy on the use of developer funds in escrow. More broadly local governments will likely have to accelerate issuance of special bonds and William expects a 50bp RRR cut in April to facilitate an uptick in fiscal funding.

Chile: Faster metrics, slower reforms

After years of debates over the country’s private pension system, a pension-tax reform may be on the way this year. Just be wary of the government’s tendency to make unforced errors. When it comes to the economy, 2023 finally saw an expansion of 0.2% and Marcos Buscaglia raises his 2024 forecast to 1.9%. If the central bank (BCCh) cuts 100bp in its April meeting and stays dovish, it may have an impact on the CLP and hence on inflation and next year’s monetary policy rate. Marcos has built two scenarios that runs his Taylor rule models to test this, leading to different inflation rates this year and policy rates the next. Marcos sees the biggest risk for 2024 of a dovish central bank is an incorrect reading of the inflation rate, leading to a 100bp cut, leading to higher inflation, higher neutral policy rates and a cost to GDP growth.

When does the Mexican growth trade take over?

Mexican assets performed extremely well last year - but this is primarily due to the strength of the peso. Jonathan Anderson contemplates when Mexico will become a "growth trade". Not soon, is his reponse. Unfortunately, there's very little momentum to be found in the data today. Domestic indicators are basically flat and the hype surrounding supply chain investment is still exaggerated. Rather, with Banxico keeping interest rates in the double digits, peso carry and fixed income remain Jonathan’s trades of choice.

Commodities

All that glitters is gold

Charles Ekins’s model is still LONG Gold; it has spiked up to a new all-time high but it retains good momentum and is not at overbought levels. The metal has lagged during the equity rally since November and arguably is just catching up, and it is not clear yet whether this rally is indicating something else. Charles has been comfortable being long gold on the basis that inflation was falling and that interest rates are likely to be cut. In an uncertain world, this should make it more attractive because the lack of income from gold is less costly in a lower interest rate environment. However, price strength may be a warning sign that inflation is not falling as fast as markets had been hoping, which puts interest rate cuts into question. The recent recovery in the oil price (literally) adds fuel to this fire.

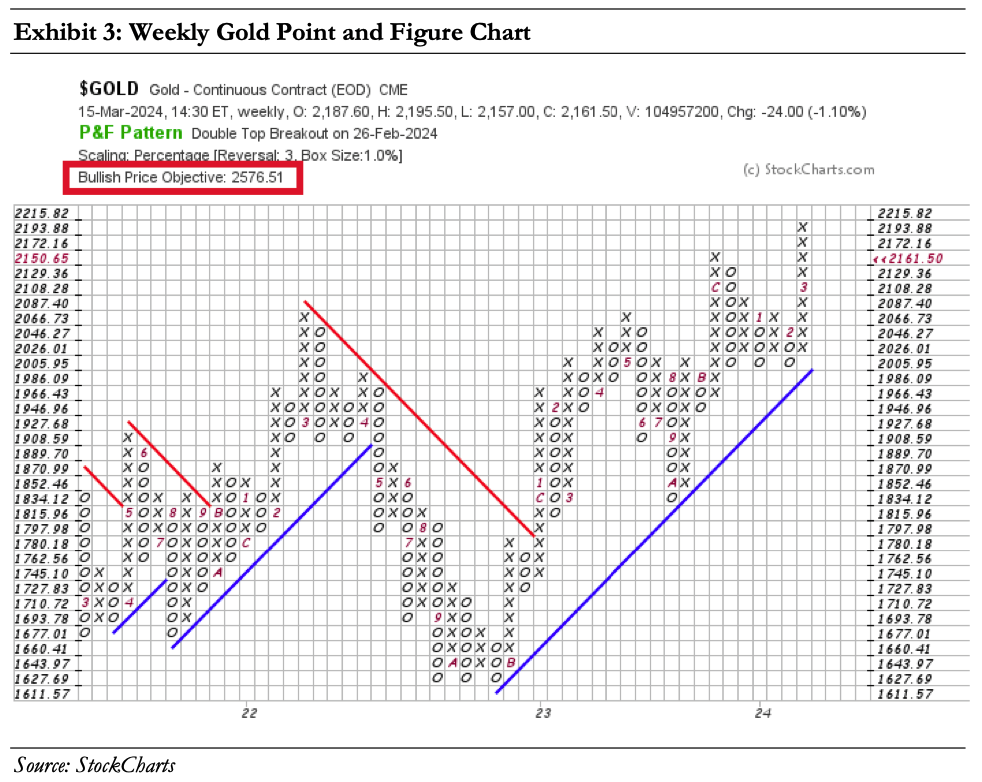

Gold: The stealth breakout you may have missed

Cam Hui points out that gold prices have staged a convincing long-term upside breakout against a backdrop of scepticism, which is contrarian bullish. Point and figure charts indicate a measured objective of 2576 over a probable 6–18-month time horizon and a measured objective of 3372 over a probable 3–5-year time frame. As well, gold mining stocks are cheap relative to gold and could offer even more upside potential on an intermediate- and long-term basis.

Materialistic desires

The Vermillion team are seeing a clear short-term rotation into commodity sectors – Energy (RSPG, XLE) and Materials (XLB). The two sectors would likely benefit once a pullback in the S&P500 finally begins. Materials (XLB) displays a bullish 10-month RS downtrend reversal and the team are upgrading the sector to market weight. Rising commodity prices are helping move these sectors higher; gold and WTI crude oil remain bullish, while the Bloomberg Commodity index (DJP) and copper are bullishly inflecting.

Manipulation and silver in a dangerous world

Jeffrey Christian shares his outlook for silver amidst escalating global uncertainty, and some considerations that investors need to account for, when determining their mode of silver investment and storage. He also discusses some long-held manipulation theories and whether CPM Group expects to see a run-up of the silver price any time soon. Jeff concludes by examining the weakness in Platinum and Palladium markets and the possibility of a recovery in those markets.

Click here to watch.

Copper primed for price bonanza

Ian Roper thinks copper prices could be poised for a rapid breakout in the coming weeks, driven by a severe shortage of concentrates supply. The metal remains the clear standout on fundamentals. There is extreme tightness in treatment charges at record lows around $12/ton and China’s smelters are being forced to adjust maintenance schedules to curb 2.5 million tons of capacity amid the shortfall. Ian believes this lack of concentrate supply is real and will persist, ultimately forcing China to significantly increase refined copper imports this year to meet demand. He envisions trading models like CTAs and algos potentially piling in to chase a breakout, mirroring gold's recent rally.