Europe

Communications

While Starlink can take share in fixed broadband, satellite D2C is not a credible substitute for European terrestrial mobile networks / material threat to tower demand. New Street undertakes a detailed review of what a LEO satellite constellation could deliver for D2C, concluding that spectrum and physics remain major constraints: SpaceX has far less handset-compatible spectrum in Europe than in the US, with future European downlink access potentially limited to 5MHz or even zero, while even generous capacity-density assumptions suggest D2C might provide only c.5% of a rural terrestrial cell’s capacity and far less in urban / suburban areas. New Street sees recent share price weakness as a buying opportunity, having turned positive (after years of caution) as 4-to-3 mobile merger fears were overdone and organic tenancy growth starts to re-accelerate again. TP €34 (35% upside).

Consumer Staples

The group is caught in no man’s land as the hypermarket format structurally declines and Dutch hard-discounter Action (920 stores across France) dismantles the mid-market. Across virtually every European consumer sector since early 2026, the pattern is uniform: shoppers are aggressively trading down. Inflation has destroyed pricing power. Pierre-Olivier Essig remains sceptical of Alexandre Bompard’s strategy, viewing it as a weaker imitation of E.Leclerc’s model. The dividend is also viewed as increasingly vulnerable. Ahead of H1 results on 23rd July, Pierre forecasts 2026 operating margin down 25bps and top-line/EBIT down 4% LFL. TP €11 by end-2026 (30% downside). Pierre presented his short thesis at our latest Best Equity Short Ideas Conference - click here to listen.

Industrials

Iron Blue initiates coverage on ANDR with a score of 30/60, which is top decile and fertile grounds for shorting. Accounting red flags include significant reliance on percentage of completion revenue recognition, FY25’s ten-year high stripped out restructuring expense, unquantified stripped out acquired technology amortisation, and expanded gap between PPE/RoU capex and the depreciation charge. Iron Blue’s €0.2bn net cash calculation was €0.5bn below ANDR’s headline measure. Governance red flags include a non-independent Chair, Board and Committees as well as KPMG’s tenure now exceeding the ten-year best practise and a surprisingly low audit fee.

European IT Services: Microsoft, OpenAI, Anthropic and AWS are not competitors

Technology

Gregory Ramirez views Microsoft Frontier Company as a pragmatic response to the challenge of deploying AI at scale rather than as Microsoft's entry into the traditional IT services market. While some overlap with systems integrators is inevitable, he believes the initiatives announced by Microsoft, OpenAI, Anthropic and AWS will expand, rather than displace, opportunities for IT services firms. Gregory therefore remains constructive on the outlook for European IT services, particularly Capgemini. As enterprise AI adoption accelerates, demand for implementation, integration and managed services should continue to grow. Investors have become overly cautious on the sector. CAP’s estimated EV/adjusted EBIT multiples of 6.4x for 2026 and 5.9x for 2027 do not fully reflect its medium-term AI growth potential.

UK Growth Stocks: Low expectations in Melrose, ConvaTec and AI jeopardy names

Willis Welby screens UK large-cap growth stocks using their proprietary expectations-analysis approach, assessing share-price-implied margins and returns against consensus forecasts. Their latest screen covers companies above US$4bn m/cap, with consensus Y3 revenue growth above 6%, positive Y3 EBIT margins, attractive Y3 IROCE and implied-to-Y3 EBITM ratios below 110. Twelve stocks make the screen. Among aerospace names, BAE has the clearer defence-spending story, but Melrose looks more forgotten, with an implied-to-Y3 EBITM ratio of just 27, leaving scope for the shares to more than double. Compass remains a strong all-round compounder, while investment in new products has driven good underlying results at ConvaTec, which still offers 60%+ upside. Willis Welby also revisits AI-jeopardy stocks RELX and Experian: despite barrier-to-entry concerns, both are currently benefiting from AI through stronger revenue growth and higher margins and may now be very cheap.

North America

Communications

Richard Windsor argues that Meta’s failure to produce a AI leading model is playing to its advantage as it now can sell its compute capacity into the market for an excellent return. Bears see potential compute sales as evidence that Meta has overbuilt, that tokenmaxing is giving way to rationing and that AI compute demand may have peaked. Richard disagrees, arguing Meta is acting rationally while it gets its AI house in order, with its Muse Spark API delayed and its open-source lead ceded to Chinese competitors. The shortage argument is supported by Meta’s inability to buy more Google capacity, xAI’s recent high-return compute sales and data-centre supply constraints. He values Meta’s core business at c.$700/share, or $770/share including compute sales, implying 30%+ upside, and is considering taking a long position in the stock with a 9-to-12-month time horizon.

Consumer Discretionary

John Zolidis updates his top retail and restaurant long / short ideas for 2H26, leaving the long list unchanged but adding 3 new short ideas: Chipotle, Ollie's and new coverage GRGD, which John describes as one of the most compelling shorts he has seen in many years. The $6bn Canadian specialty apparel retailer is viewed as over-earning after 2 years of exceptional demand, with SSS up 12% and 27% in FY24/FY25, single-digit markdowns, gross margins above 60% and EBITDA margins in the mid-30%s. John believes demand is now slowing sharply as customers push back on aggressive pricing, including AURs up 15% last quarter, setting up higher markdowns and EBITDA margin normalisation 1,500-2,000bps below recent levels, while consensus still models margins rising.

Consumer Discretionary

The Retail Tracker pushes back on the idea that LULU is a “dead brand”, arguing the stock now prices in a permanently impaired business rather than one capable of stabilising. They acknowledge that LULU is no longer as hot as during the post-Covid WFH boom and deservedly de-rated after product and merchandising missteps. However, recent traffic and sell-through suggest the new team’s assortment changes are beginning to work, with pastels, brighter colours and new styles gaining traction, while new product now represents c.30% of the assortment. Accessories weakness was planned, while the "ugly" TJ Maxx-style checkout areas are being phased out. With the shares down 45% YTD and trading below 10x, The Retail Tracker sees scope for a recovery towards $200 if execution improves.

Consumer Staples

Hedgeye has been short ELF for much of the past year, citing an oversaturated beauty market and soft organic core, with units down c.5% after the Aug 25 price increase, but now believes that last month's haircare launch creates a more constructive setup. They see haircare as a natural extension of ELF's dupe model into a fast-growing, high-priced beauty category, with $6-10 products undercutting prestige brands while “skinification” increases multi-SKU routine potential. The 2022 ELF SKIN launch, now the #11 mass skincare brand, provides a template, while the March haircare test sold out in 48 hours with 65% new-to-brand buyers. As the top line improves due to hair care launch, continued growth in Rhode/Skincare and international whitespace (legacy peers 70% Intl. vs ELF 20%) Hedgeye sees the stock revisiting $100 by year-end and more than doubling over a TAIL duration.

Materials

The market is fundamentally mispricing tier-1 lithium producers by anchoring valuations to depressed spot prices. OMNISIGHT’s latest Master Dossier on ALB exposes a massive structural gap between Chinese spot indexes and actual realised contract pricing. While consensus models assume an $8/kg plateau, ALB’s opaque index-lagged contracts and price floors generated significant FCF, allowing the company to pay down $1.3bn in corporate debt in a single quarter. Furthermore, ALB is demonstrating aggressive capital discipline by intentionally idling capacity, such as the Kemerton Train 1 facility in Australia. This deliberate restriction of Western conversion supply engineers artificial scarcity, ensuring margin protection that algorithmic trading models are currently failing to discount.

Technology

The new market narrative is focused on Arm’s AGI CPU strategy, under which the company targets $15bn of additional FY31 revenue, but AlphaValue sees major execution, customer and market risks. FY26 revenue grew from $4bn to $4.9bn but was heavily supported by related-party licensing and services revenue from a SoftBank affiliate, while external licensing revenue declined. Margins also remain far from the FY31 model: non-GAAP operating margin has stayed in the low-to-mid 40% range, while GAAP margins are significantly lower once share-based compensation is included. AlphaValue also questions whether selling server CPUs risks competing with Arm’s own licensees and undermining its neutral IP model. Even assuming management’s FY31 targets, the shares trade around 40x highly optimistic 5-year-forward EPS vs. 230x current P/E. The stock is disconnected from fundamentals. TP $97.8 (70% downside).

Borrowed Growth: The accounting & financing behind Broadcom's results

Technology

As the capital expenditures required to fund AI compute infrastructure scale to unprecedented heights, a critical transition is occurring. AVGO's operating profile is no longer determined solely by end-market demand for its custom chips. Instead, its financial performance has become intrinsically linked to how that demand is structurally financed, contractually recognised and ultimately converted into cash. In this report, Veritas separates organic, customer-funded consumption from growth that may be pulled forward or amplified by supplier financing structures, revenue recognition policies, or balance-sheet optimisation techniques. For instance, Receivables and contract assets reached ~$16.1bn in 2025, up ~82% against ~24% revenue growth, pushing adjusted DSO from 62 days to 92 days, while factoring masks how far the cycle has actually stretched beyond that.

Technology

BTN remains sceptical of IPGP’s apparent earnings resilience, arguing recent “beats” have been flattered by unusually wide guidance ranges and accounting tailwinds. The company missed 1Q26 consensus EPS by 2c, but prior quarters looked stronger because management guided to very broad EPS ranges, including 5-35c in both 3Q25 and 4Q25, despite EPS already running around 30-35c in the preceding three quarters. BTN also questions valuation: at c.72x forward adjusted EPS, trailing four-quarter adjusted EPS of $1.40 includes 53c of interest income; excluding this, the multiple rises to c.135x. Earnings quality concerns include several quarters of declining charges against gross profit; prior warranty-accrual reductions that may now reverse as warranty expense rises; extended machinery useful lives; fully depreciated assets supporting margins; and reduced bad-debt reserves despite 74% non-US sales.

Technology

Trivariate models MU’s earnings across thousands of simulated scenarios varying the size and duration of the current memory cycle, concluding that peak earnings are most likely between mid-2028 and late-2029. Their base case assumes that c.75% of the current earnings improvement is structural rather than purely cyclical, driven by AI-related memory demand extending the cycle beyond historical norms. Under this scenario, the company’s peak EPS could approach $190-$200, materially above current Wall Street expectations, while normalised earnings power is estimated at $82-$86 per share after adjusting for cyclicality. The current share price implies only c.5-6x projected peak EPS; if investors ultimately value peak earnings closer to 8x, the stock could be worth $1,500-$1,600/share. Even using normalised earnings the stock appears reasonably valued trading on 11-12x EPS.

Enterprise IT Channel Checks: AI demand meets pricing pressure

Technology

Channel conversations highlighted accelerating AI adoption, tightening cybersecurity spending priorities and growing pricing pressure across the infrastructure market. Partners pointed to rising enterprise demand for AI governance, next-generation SIEM platforms and sovereign cloud solutions, while networking, memory and security vendors continue to push through additional price increases. Sales Pulse also shares fresh partner commentary on key names including HPE, Zoom, RingCentral, Palo Alto, F5 and Nice, along with several emerging trends shaping the enterprise technology landscape heading into quarter-end.

Asia

Asian insider sentiment turns bullish

Smart Insider’s June Asian insider-trading review shows a sharp improvement in sentiment across Asia ex-Japan/Taiwan, with 1,354 insider purchases from 969 companies totalling US$1.3bn, up 70% vs. May, almost double June 2025, and the most buys in a single month since 2020. Selling remained relatively light, leaving the sell/buy ratio at a bullish 0.64. The strongest buying signals were in South Korea, Hong Kong and China. Smart Insider upgraded 30 stocks, the first month with 30+ upgrades, led by tech hardware, chemicals, industrial transport and pharma/biotech. June additions ranked +1 (highest rating) include Bangkok Expressway & Metro, MINISO, Kingsoft, CStone Pharmaceuticals, Hyundai Rotem, Dongwoon Anatech, MLS, Anhui Jinhe Industrial and Yantai Jereh Oilfield Services.

Aequitas reviews two upcoming Asian lock-up expiries with very different risk profiles. For Bharat Coking Coal, the 6 month lock-up on the balance of Coal India’s promoter stake expires on 14th July, releasing c.US$1.3bn of BCCL shares, equivalent to c.70% of the company and 87 days of ADV. However, despite the stock trading c.65% above its IPO price, Aequitas thinks a near-term placement is less likely given Coal India is Government controlled, although medium-term dilution remains possible to lift free float and meet minimum public shareholding rules. GigaDevice looks more exposed to near-term selling: cornerstone investors owning c.2% of the company, worth c.US$1.4bn and eight days of ADV, are released on 12th July and are sitting on huge gains. Aequitas thinks they may look to book profits after the stock’s strong run.

Korean Banks: Woori is the top pick, Hana retained on buy list

Financials

Victor Galliano reviews 6 South Korean banks using profitability and credit-quality screens, together with his proprietary weighted scorecard, to identify attractive value and sustainable-return potential. Woori Financial is the deep-value top pick, supported by a very attractive PEG ratio and high dividend yield; strong credit quality credentials, as well as strong capital adequacy ratio. Its PBV discount to KB Financial has widened to more than 35%, greater than one standard deviation from the 3 year mean and a level rarely sustained for long. Hana remains attractive on valuations vs. returns, with appealing equity risk premia and dividend yield. Importantly, pre- and post-provision returns have been on a steady upward trend over the last 5 quarters, helped by interest margin resilience in a dovish interest rate environment.

Developed Markets

Underweight stocks & bonds, overweight private credit & commodities

Craig Ferguson points out that the 40 yr long disinflationary bond bubble ended at March 2020 cycle lows. A new inflationary decade of high macro data volatility, policymaker activism & mistakes, demographic decay, deglobalisation and geopolitical tension is underway. Decade long bubbles in bonds, stocks, property & corporate bonds that are leveraged to & dependent on yields & excess liquidity should unwind. This unwind started in 2021 with rising government bond yields. To date this has not yet punctured bull markets in stocks and corporate bonds. The normal template is high cash rates produce recession & growth assets correct to “cheap” levels. After the first inflation rate hike cycle 2020-2023 and the second disinflation rate cut cycle 2023-2025, the third inflation rate hike cycle is underway. How far inflation spikes will dictate whether this is a short sharp 1995 hike cycle, a moderate rate hike cycle or a hard 2022 cycle. The harder the worse for recession odds and stock markets...

Global liquidity levels off as policies diverge

Global liquidity levels off as base peaks Global liquidity levels are levelling off at US$194.1tr, as the shadow monetary base has likely peaked. Michael Howell observes that near-term momentum is driven by base effects, low volatility, and renewed US Federal Reserve injections of 3.3% on a three-month annualised basis, which reversed mid-June tightening. However, Michael notes that the shadow monetary base has stalled at US$110.3tr due to weakening People's Bank of China liquidity, ongoing Bank of Japan and European Central Bank quantitative tightening, and US dollar strength. Meanwhile, the MOVE index remains low at 65, suggesting a deliberate US Treasury policy to lower volatility. In response to this liquidity cycle phase shift, allocation data show that investors remain broadly risk-on but are gradually trimming exposure to emerging markets across Latin America and Asia, while rotating modestly within developed markets by remaining very risk-on in Japan and maintaining a broadly neutral exposure to the US and UK.

The inevitable correction

While many people continue to shake their heads in wonderment at the way that markets shrug off fundamental macroeconomic issues, John Llewellyn provides a sobering emotional counterweight by recalling Minsky’s generic 6 stages of speculation and crisis. Events start with a “displacement”: some exogenous shock outside the macroeconomic system. Expansion of bank credit enlarges the total money supply and feeds the boom. Demand pressure and prices increase, giving rise to new profit opportunities. Positive feedback develops. “Euphoria” sets in. Bubbles or manias develop. The number of firms and households engaging in these practices grows large. ‘Overtrading’ spreads from one country to another, through arbitrage for internationally traded commodities and assets, capital flows, foreign exchange, or psychological transmission effects. Importantly, John says the correction that so many economists expect will not necessarily lead to a major crisis as in 2008. However, a correction seems virtually inevitable.

UK: Westminster is on the ropes, risk assets aren’t

Report by

BCA Research

BC

According to Ayaan Sohhel and Jeremie Peloso the UK economy is becoming increasingly fragile, but the investment outlook is improving. They say slower growth and a more dovish BoE will support gilts, while UK equities will likely benefit from a favourable sector mix and a weaker pound. Ayaan and Jeremie note that the UK entered the Iran-related energy shock with recessionary signals already flashing red. The public sector is temporarily cushioning the downturn, but it will not prevent weaker labour demand and slowing real income growth from causing a slowdown. Anchored inflation expectations should allow the BoE to start cutting by early 2027, supporting our overweight position on Gilts. Trade remains one of the few bright spots, as resilient services exports and AI-related exports partially offset domestic weakness. Ayaan and Jeremie favour UK equities over Eurozone peers, prefer healthcare over banks and large caps over small caps, and remain cyclically bearish on sterling.

UK: Hedge funds are not the only game in town

David Owen examines how the US and UK are financing their large twin deficits, noting a significant compression in UK margins since the GFC. Addressing Gilt market funding, David argues that UK HFs are not the only game in town despite recent Bank of England leverage changes for repos. While the central bank aims to limit the outsized role HFs play in introducing additional significant volatility when they find themselves long and wrong, alternative buyers absorb supply. Net foreign buying amounted to around £160bn since May 2024, supported by substantial cash sitting on the UK household balance sheet. Concurrently, UK banks are acquiring short-dated Gilts as reserves fall. Crucially, as the balance sheet continues to shrink, additional volatility at the short end of the curve will kick in when reserves fall below the so-called PMR. In a world of fewer reserves, additional volatility could become the norm. The BoE will not want HFs adding to it.

Are E(U) ready?

Examining the Ankara summit, Niall Ferguson delineates an alliance defined by greater European self-sufficiency in conventional deterrence and reduced American forces on the Continent. Niall considers Europe's conventional capabilities sufficient to deter Russia, but warns that the rift in the transatlantic alliance leaves vast capability and logistical gaps to fill before Europe becomes conventionally defensible by 2030. He identifies Washington's plans to reduce force commitments as the most consequential development within NATO, creating an operational window that a recovering Russia could exploit to expose the dwindling credibility of Article 5. For Niall, Europe's greatest vulnerability is the US reduction in logistics rather than combat aircraft, as a shortage of air-to-air refuelling and strategic airlift yields a substantially thinner margin of security. While he places low odds on a conventional Russian attack, Niall foresees Moscow continuing hybrid and covert operations below the politically contested Article 5 threshold.

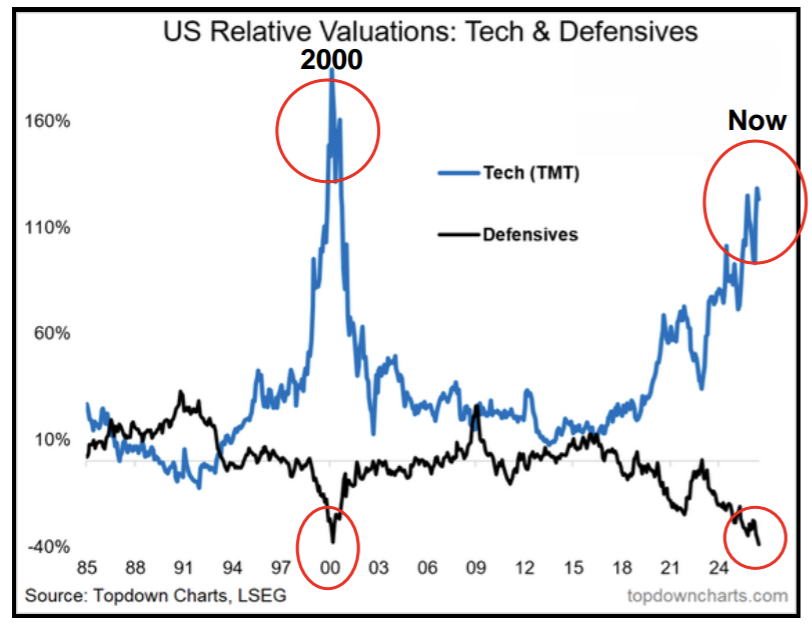

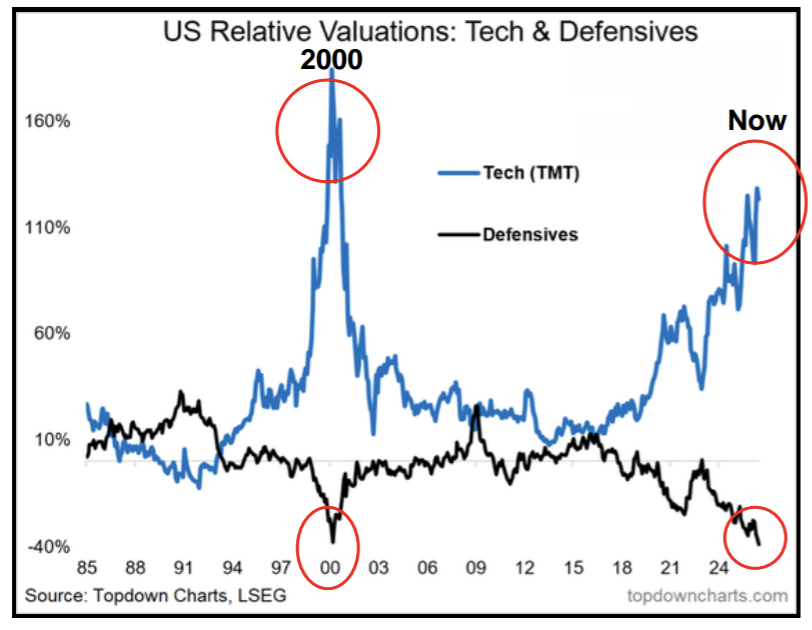

US: AI stocks are horrendously overvalued

At the top of the March 2000 TMT bubble, tech crashed and defensive sectors rallied. Michael Belkin thinks we’re in a similar set-up now. As the AI boom runs out of steam, it is becoming clear that tech stocks are horrendously overvalued, mainly the AI and momentum stocks that are retail investor favourites. With MAG7 stocks down a lot from their peaks, the hyperscalers are under pressure to justify or reduce their excessive datacentre investment plans. Even a slight suggestion of scaling back grandiose AI investment plans would send a shockwave through all the AI infrastructure plays. XLK is down -7% from its June 2nd peak despite the biggest public tech inflows of all time, imagine what will happen when inflows turn into outflows. Michael’s model recommends focusing on healthcare, financials, consumer staples, utilities, REITs and energy. They sound like boring yesteryear fallen stars, but they’ll become attractive as the bloom falls off the AI rose.

US: Slower wages despite lower jobless rate

Graham Turner notes that jobs growth in the US slowed in June to +57k, but the unemployment rate fell to 4.19%. Graham says that it is tempting to put one of these numbers down to statistical noise, but they can both be right and may reflect the new norm. Prior to Covid, Fed research had suggested that the breakeven for non-farm employment growth was slowing to around 60-65k m/m. New research suggests that the breakeven for payrolls has dipped to 10k m/m, implying that the labour market is getting tighter and warrants a Fed hike. But the June payroll report also revealed a decline in the growth rate for average hourly earnings for production and non-supervisory workers. Real average hourly earnings are contracting for all employees. Graham says that disruption to the labour market from technology (AI) suggests that NAIRU has also fallen sharply: the case for a Fed hike is not proven.

Don’t underestimate the peak in AI capex

Gaius King argues that investors are dramatically underestimating the potential implications behind Meta's announcement to sell its excess AI compute. This decision marks a structural change, signalling a realisation that further investment into AI research is probably pointless. Gaius observes that Meta has unilaterally fundamentally changed the parameters of the game, forcing other participants to react as the market's assumption of scarcity comes into question. This shift will weigh heavily on cloud peers like AMZN, ORCL, and MSFT, alongside chip and memory names like NVDA and MU, as demand for their products drops. With mega-cap US hyperscalers projected to spend $755Bn in 2026 capex — representing 100% of operational cash flows — any collective reduction could halve 2027 expenditures. This impending phase shift threatens to trigger daily forced liquidation ratios across record South Korean margin loans and unwind crowded retail positions in US-listed semiconductor ETFs.

Emerging Markets

Argentina steers a delicate monetary FX balance

Marcos Buscaglia notes the Argentine peso weakened 5.2% against the USD in June, the second consecutive month of real-term depreciation as local conditions changed. Farmers' USD sales remain low and oil prices dropped, prompting the central bank to slow down FX purchases to $1418mn. To manage this delicate balance, authorities are increasing supplies of foreign exchange hedging via dollar-linked bonds and rebuilding their position in Rofex. Although a tightening of monetary conditions recently pushed interest rates up, the central bank did not roll over ARS4.5tn in a bi-weekly auction to force immediate declines, as reviving credit remains atop their priority list. Marcos expects the currency to continue weakening in the second half of 2026 alongside a gradual real-term depreciation. Dollar-linked hedged strategies look attractive after carry opportunities reset, offering tactical opportunities to build synthetics by buying the dollar-linked bonds and selling USD in the futures market.

Bolivia’s baby steps helped by export prices

Jonathan Anderson points out that high export prices have given Bolivia much-needed breathing room in transitioning from its failed peg, with narrower black market FX spreads and falling inflation. The first adjustment steps are underway, with a new exchange rate regime (at least on paper) and ongoing initial IMF discussions. There’s still a good way to go. In particular, Bolivia needs to address its massive budget deficits and move to a truly market-led interest rate environment. The risk along the way is devaluation followed by a repeg, continued FX controls, little fiscal adjustment and renewed high inflation pressures; just as happened in Turkey, Egypt and Nigeria. It is difficult to call the market. Sovereign dollar debt has rallied dramatically after the elections, and could improve further in the best-case scenario given Bolivia's small market exposures, but could also retrench on policy delays and disappointments.

Brazil: Will the blue wave crash?

Niall Ferguson expects current President Luis Inácio Lula da Silva to be re-elected in the upcoming Brazilian presidential election. While a blue wave sweeps Latin America, its largest economy is poised to remain red as the electorate grows increasingly exhausted by the dichotomy between Petismo and Bolsonarismo. Lula’s populist strategy, including a popular income-tax exemption and a 40-hour workweek proposal, has sweetened the middle-class case but ensured long-term yields remain above 14%, limiting the room for cuts at the central bank. Consequently, Niall expects a run-off against a right-wing candidate as the base case. Flávio Bolsonaro trails his father's historical polling following a banking scandal, while outsider Renan Santos leverages a radical security programme. Niall predicts Donald Trump will impose 25% tariffs on Brazil on July 15, a move set to strengthen the incumbent while hindering the right-wing opposition.

China: June PMI suggests a return of deflationary pressures

Dinny McMahon points out that China’s purchasing managers indices for June indicate stable manufacturing conditions, but factory gate deflation has unexpectedly returned. The NBS manufacturing PMI came in at 50.6, broadly in line with May’s 50.5 reading. The production subindex ticked up to 51.4, while new orders came in at 51.2 – reversing May’s contraction. The NBS producer price subindex fell into contractionary territory at 48.2, reversing five consecutive months of expansion, despite the raw material purchasing price index remaining expansionary at 54.2 – meaning manufacturers are still paying more for inputs but cutting the price of finished goods. Dinny says that the divergence between rising input costs and falling output prices is the most significant signal in this month’s data. Manufacturers appear to be absorbing higher input costs while cutting factory gate prices – a dynamic that will compress margins further and is consistent with the ongoing profit squeeze in downstream industries.

Indonesia: Record lows but not abandoned

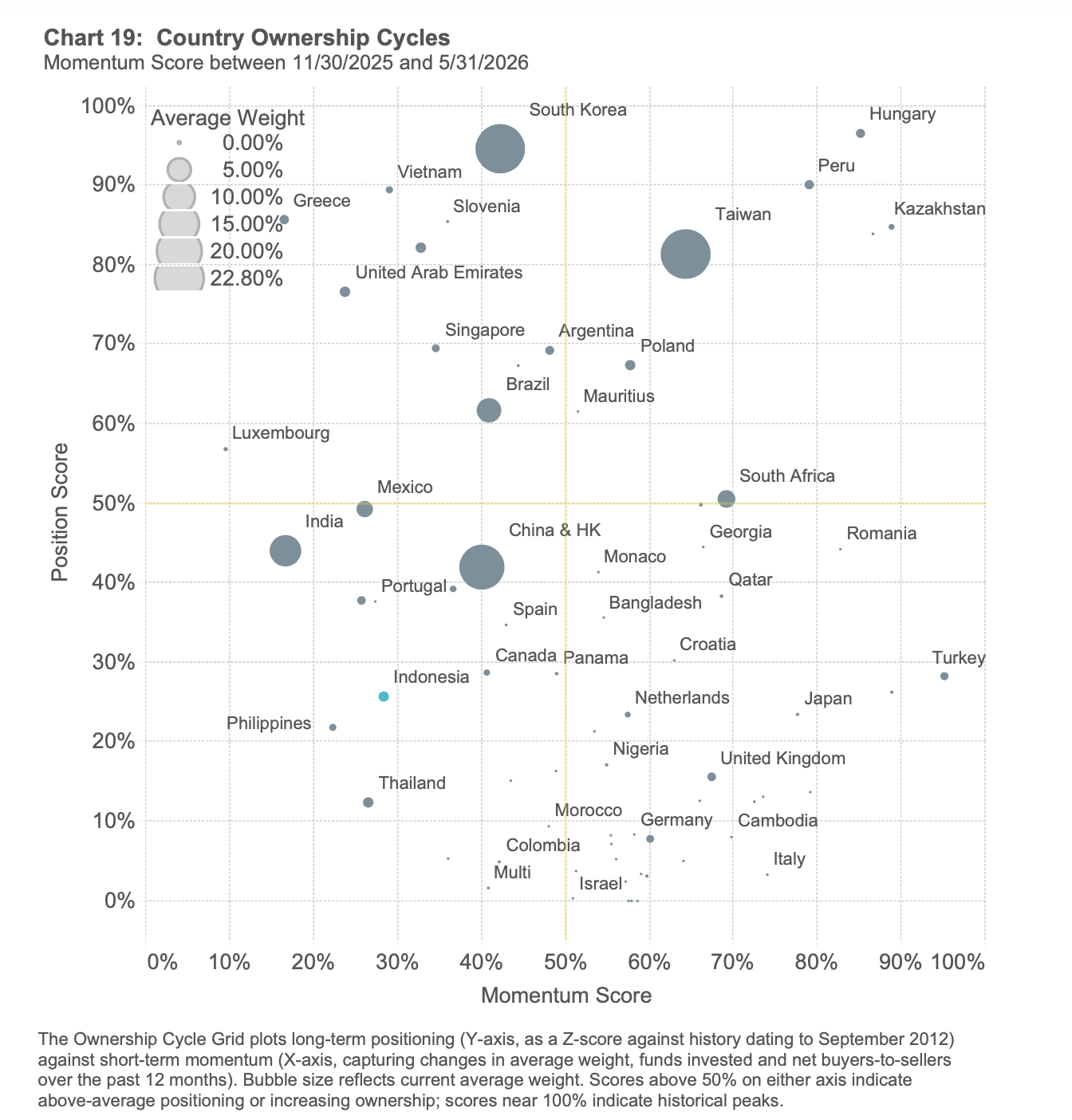

Steven Holden observes that for Indonesia, the direction of travel has been clear for some time, with average weights at all-time lows of 0.93% and participation at a 15-year low of 80.45%. While MSCI's continued review of the country's EM status keeps a structural question mark hanging over the investment case, the structural case for Indonesia has not disappeared. The banking sector remains well-capitalised, and Bank Central Asia continues to command loyalty among managers, held by 42.2% of funds. Sitting in the bottom-left quadrant of the ownership cycle (see chart), the market combines depressed positioning with negative momentum. Yet eighty percent of funds remain invested, and the majority are still overweight relative to the benchmark. Most selling has been a gradual reduction rather than a wholesale exit, meaning the cost of being wrong on a recovery is now arguably greater than the cost of further patience.

Singapore: Is the lion city about to roar?

The iShares MSCI Singapore ETF (EWS US, last USD30.14) has broken out from a 9-month Rectangle targeting an advance to USD32.90. At the same time, the monthly chart shows a possible breakout above an 18-year Ceiling. If a sustained breakout occurs, the target would be USD55.00+. Chris Roberts will open an initial long position and add if a more sustainable advance begins to play out. Go 50% long at market. The initial stop is a daily close below USD27.85.

South Africa: Joburg on the brink

Peter Montalto believes that the Treasury's forthcoming decision on equitable share transfer cutoff to Johannesburg won't create a financial crisis; it will accelerate one already under way. What hangs in the balance is whether Treasury withholds Johannesburg’s July equitable share transfer of just under R3bn under Section 216(2) of the Constitution. Minister Enoch Godongwana's follow-up letter demanded detail on the Eskom and Rand Water debts, but regardless of the tranche decision, the city is in serious trouble. The city is holding about five days of cash against Treasury's 30-day minimum benchmark, facing an unfunded budget gap of about R2.1bn. Before the November election, an Eskom cut-off decision, the Rand Water shutdown, and growing City Power business-rescue talk all land on the same thin liquidity. For banks and creditors exposed to the city or its entities, covenant and facility reviews should assume slower payment.

Commodities

Western subsidy initiatives are overhyped

In their June Macro Digest, OMNISIGHT deconstructs the escalating critical minerals processing race. Market consensus assumes that Western subsidy initiatives, such as the $12 billion US Project Vault, will rapidly neutralise reliance on Asian supply chains. This is a severe miscalculation. While state capital is accumulating unrefined ore, it ignores the physical necessity of finished magnet and alloy production. The fundamental bottleneck is the 5 to 10-year launch cycle for greenfield refining capacities, which current equity pricing falsely assumes will be fully operational by 2027. Furthermore, aggressive state interventions are paradoxically crowding out private capital. The result is an insurmountable time lag that guarantees a structural deficit in processed metals by the end of the decade.

Gold & Silver: Near-term price pullback likely

In this presentation, Jeffrey Christian of CPM Group gives a precious metals update focused on the gold price outlook, silver market slump, investor selling, political risks, platinum and palladium weakness, and the US dollar. He explains why gold continues to test the $4,000 to $4,100 area and why a move toward $3,800 remains possible over the next couple of months. Jeff also discusses silver’s test of the $60 level and why CPM Group would not be surprised to see silver move toward $55-$50 in the short term. He explains why some investors have been selling physical gold, silver coins, ETFs, and other positions, while longer term investors continue to hold precious metals as a hedge against economic, political, and financial risks. The presentation also covers China’s physical gold demand, India’s gold selling, political risks involving Ukraine, Russia, NATO, Israel, Turkey, and broader political instability, all of which remain supportive for gold and silver over time. Click here to watch.

Critical minerals: Don’t just look at the tonnes

James Burdass says that the "China discount" has evolved into something more significant: a geopolitical risk premium. Investors are increasingly differentiating between companies that merely possess mineral resources and those capable of delivering strategic supply. The first differentiator is processing independence: companies capable of separating and processing material outside China are likely to command an increasing premium. The second is commodity mix: projects dominated by abundant light rare earths face fundamentally different economics from those with meaningful exposure to heavy rare earths or defence-critical materials. The third is sovereign alignment: governments across the G7, Australia and Japan are increasingly directing loan guarantees and strategic investment towards projects capable of strengthening domestic supply chains; access to public capital and long-term industrial partnerships is becoming as important as geology itself. Resource investors who continue to value projects primarily on tonnes in the ground risk overlooking where economic value is actually being created.

Data centres: After the gas rush

The Sustainable Market Strategies team highlights how solar, wind, and BESS hybrids already beat gas on cost at 95% reliability, signalling an aggressive shift in data centre power procurement. Natural gas remains the leading power source for US data centres because turbines meet 99.9% uptime requirements and handle rapid AI load swings, but this advantage looks temporary as utility-scale storage costs continue falling. By 2032–2035, emerging long-duration batteries using iron-air and flow systems could close much of this reliability gap. This structural transition exposes a significant market dislocation among overextended turbine manufacturers. While pure-play BESS names have mostly underperformed over the past year, gas turbine makers have sharply outperformed despite losing momentum, creating a distinct short opportunity for companies such as GE Vernova Inc. Conversely, forward-looking investors should enter a position via a market-cap-weighted basket of underperformed BESS providers and secure exposure to high-growth integrators like Clean Max Enviro Energy Solutions Pvt Ltd.

Shifting trade flows destabilise US panel markets

Amid a sluggish US housing market and macroeconomic challenges, demand for structural panels and virtually all solid-wood products is languishing. North American panel producers have carefully managed supply through reduced operating rates, mill curtailments, and delayed capacity expansions to keep markets somewhat tensioned. However, an influx of offshore imports threatens to undermine these efforts and push markets into oversupply. Offshore plywood imports jumped to 177MMsf in May, meaning producers Boise Cascade Co and West Fraser Timber Co Ltd must monitor South American supply closely as weakening domestic demand cannot easily absorb a material increase. Conversely, offshore OSB imports plummeted to less than 1MMsf, keeping the supply balance tensioned for producers such as Louisiana-Pacific Corp, WFG, and Weyerhaeuser Co. Moving into the summer doldrums, investors should maintain caution on all solid-wood leveraged names given an expected seasonal slowdown, keeping in mind that plywood holds more downside risk now.