Europe

Financials

Anas Abuzaakouk (CEO since Aug 2017, joined 2012) bought 30,000 shares at €149, spending €4.5m. He has a great track record based on his 21 prior purchases. This is his single largest purchase and the highest price he has paid. He last bought in Oct 2025 at €108. Smart Insider has ranked the stock several times based on his prior activity, with the majority of those signals proving to be very timely. They are ranking the stock +1 (highest rating).

Healthcare

Following publication of the company's FY25 annual report, Iron Blue increases their CTEC score to 29/60 (newly top decile). They see upside risk to the group’s future D&A expense given FY25 PPE/RoU capex exceeded depreciation by a 10-year high 33% of PBT adj and balance sheet intangible assets under construction (historically mainly software) almost trebled Y/Y. Risks in CTEC’s debtor book may be emerging with year-end debtors overdue by >90 days but not impaired increasing to $31m from $8m despite FY25’s rise in provisioning expense. Inventory impairment provisioning remained compressed and CTEC continued its trend of stripping out restructuring and other costs. FY25’s trade payables spiked higher, bringing risk of mean reversion. They also note that both the CEO and CFO were internal appointments.

Industrials

Report by

Insight Investment Research

Robert Crimes highlights GET as a unique long-duration infrastructure asset with a potential takeout emerging. Eiffage and Mundys will likely soon own ~59.8% of the company, having recently added to their positions. Insight’s buyout scenario IRR is 14.7% (at 25% share price premium of €24/share), +410bps above their deal Ke of 10.6%. While shuttle traffic remains pressured by excess ferry capacity, this has been offset by higher pricing, supporting continued revenue growth. The underlying appeal is the asset’s durable cash generation, with ~€710m recurring FCF (~6.9% yield) and long-term growth driven by pricing, traffic recovery and new high-speed rail routes.

Technology

The group’s year-end update more than confirmed the optimism management showed at the interims. Revenues will be ahead of consensus, with double digit growth and record backlogs. Confidence is also evident in a 21% increase in headcount, albeit with some margin pressure from contractor usage. Consensus revenue forecasts have been upgraded, though EBIT has edged slightly lower. The balance sheet remains a clear strength with £160m of net cash and potential for ~£70m of Y2 FCF. While analysts appear to be recognising the revenue inflection, the implied to Y3 EBITM ratio here is now 40. That is very low for the growth on offer, with Willis Welby arguing the shares could easily rise 50% from current levels.

North America

Identifying stock swaps within your portfolio

Mill Street's Swap Shop report reflects frequent interest from equity portfolio managers in using their MAER model (the Monitor of Analysts’ Earnings Revisions) to identify problematic low-ranked holdings and provide high-ranked substitutes that preserve overall portfolio allocations. The screens take advantage of MAER’s strong intra-sector or intra-industry ranking performance to allow managers to stay not only within a benchmark universe but also identify stocks within specific industries as potential swaps to keep sector / industry weightings consistent. This month they include swap screens for Global Technology / Communication Services stocks and Global Energy / Materials sectors stocks to capture the key topical themes of Tech / AI and commodity prices. Also included are the regular screens for the S&P 500 universe and their European stock universe. Click here to access the report.

Drone related investment ideas

Red Cat (RCAT US) - expected to disappoint on its recent and highly speculative marine drone division; management has credibility issues from previously missing on guidance; and the company has yet to be included in the Department of War’s Drone Dominance Program.

Motorola Solutions (MSI US) - has been a dominant name in critical communications equipment for fire, police and government for decades. The long thesis now is based on the company's “transformational” acquisition of Silvus Technologies, a tactical drone networking business.

Fujikura (5803 JP) - tremendous scaling opportunity for selling co-packaged optical connectors for AI data centres, alongside expanding demand for fibre optics in drones - which is poised to become one of the fastest-growing segments within fibre optics - from military kamikaze and loitering munitions to commercial inspection drones, delivery systems and advanced surveying platforms.

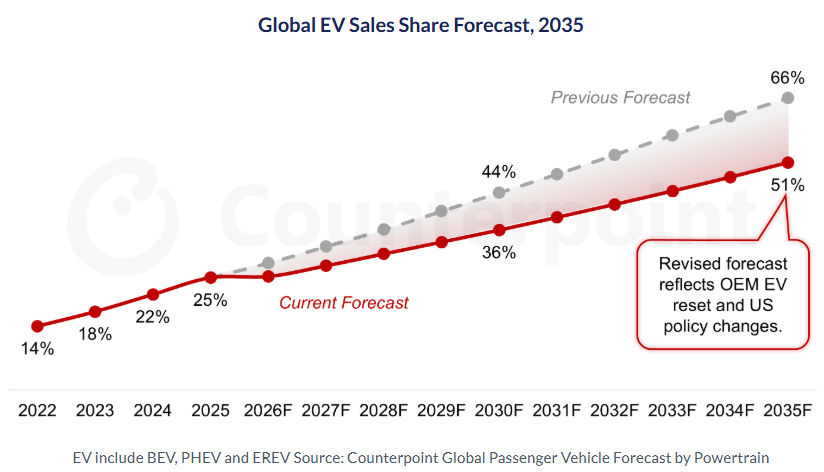

EV adoption slows, but long-term fundamentals remain strong

Consumer Discretionary

Counterpoint cuts their long-term EV adoption forecast, now expecting EVs to reach 51% of global vehicle sales by 2035 (vs. 66% previously), reflecting OEM pullbacks after >$70bn of losses and a slower-than-expected ramp. Despite this, the long-term outlook is strengthening. Falling battery costs (sub-$70/kWh by 2030 and reach $55/kWh by 2035) and energy market disruption following the Iran war are improving the relative economics of electrification. EV share is expected to reach ~36% by 2030 (~10% CAGR), with BEVs leading and hybrids (PHEVs/EREVs) emerging as critical bridge vehicle types globally. The industry is shifting from aggressive targets to a more measured rollout, while adapting to evolving regulatory policies, but structural drivers remain firmly intact.

Consumer Discretionary

Paragon’s executive diligence memo was originally published when Heidi O’Neill was being discussed as a potential CEO successor at Nike and they viewed her as a poor fit for that role. At LULU, she is somewhat better matched to the brief, but their core reservations remain. She has tended to look stronger as an operator and internal brand steward than as a true strategic architect. That matters at LULU, where the challenge requires a sharper product vision, stronger innovation instincts and a willingness to make harder calls on strategy and talent. So, while the fit is better than it would have been at NKE, Paragon still views her as more of a stabiliser than an obvious answer to LULU’s deeper issues.

Consumer Staples

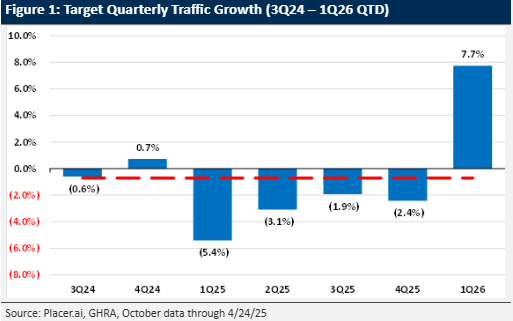

GHRA’s Proprietary Quarterly Store Manager Survey reinforces improving operational momentum, aligning with their traffic data and field checks that point to tangible progress in restoring merchandising authority through a refreshed assortment. This supports GHRA's optimistic outlook for TGT first outlined in their Jan 26 upgrade. Survey results show a notable sequential improvement: 29% of managers report sales tracking above plan (vs. 11% in 4Q25), while 31% cite stronger traffic (vs. 9%). Seasonal performance was particularly robust, with 46% indicating better-than-expected trends (vs. 9%), alongside a meaningful pickup in discretionary demand, suggesting recent brand partnerships are resonating. However, promotional intensity has increased, with 60% flagging higher markdown activity. While inflation concerns among customers edged up, sentiment appears to be stabilising.

Financials

MRX is a beneficiary of geopolitical instability, particularly in commodity markets, where it is a leading player. The shares have pulled back from recent highs but are only ~12% above the 2025 peak, despite 1Q26 profits likely to rise c.50% Y/Y - implying meaningful multiple compression. Fighting Financials sees scope for this to reverse as volatility persists. Consensus Q1 PBT forecasts sit c.13-14% below management’s end of March guidance, while FY26 consensus implies flat Y/Y performance for the remaining quarters, which is clearly inconsistent with the current earnings trajectory. With the potential to return >60% of its m/cap via dividends and buybacks over the next 5 years, MRX stands out as one of the cheapest, high-quality financials in their investment universe and is one of the few compelling long ideas in a market, where opportunities are largely on the short side.

Canadian Lifecos: Private credit risk under scrutiny

Financials

Roshan Paunikar’s analysis highlights rising scrutiny around private credit exposure within Canadian lifecos, with risks centred on below-investment-grade assets, valuation opacity and broader fixed-income sensitivity. While portfolios remain skewed towards higher-quality credit, companies are not insulated from a weaker environment, with potential impacts including higher credit losses, fair value marks and pressure on regulatory capital. Manulife Financial appears most exposed driven by a higher proportion of below-investment-grade private credit and a relatively riskier fixed-income portfolio, while Sun Life Financial appears most negatively exposed to wider credit spreads. Great-West Lifeco appears to have the most conservative investment portfolio among peers.

Industrials

Investors should own the stock ahead of what Craig Huber believes will be a robust US residential market recovery leading to an estimated 25% pick-up in mortgage inquires in 2027 and a further 20% jump in 2028. He also continues to argue that investor AI fears related to EFX and the information services stocks, in general, that he covers are completely irrational. With ~90% of revenue derived from proprietary data and significant regulatory barriers, AI is a net positive. Craig’s new 2026/27 adjusted EPS estimates are a Street-high of $8.79/$11.35 vs. consensus of $8.59/$10.28, with a 12-month TP of $224 (30% upside).

Materials

GMR cuts FCX to Sell following further production downgrades at Grasberg, with the ongoing impact of the 2025 “Mud Rush” now expected to persist through 2027. They estimate cumulative production losses of 952kt of copper, 1.5Moz of gold and 6.6Moz silver over 2025-2029, equating to $19.2bn of lost revenue at spot prices (or $15.4bn on GMR’s base case price forecasts). GMR has cut 2026/27 EBITDA forecasts by 15-21% and reduced its valuation by 27%, arguing the recent share price reaction underestimates the severity and duration of the impact. With risks of further downgrades and rising capex, downside remains.

Technology

JNK’s analysis suggests LSCC is tracking ahead of guidance, with Q1 supported by strong bookings extending into 1H27 and a book-to-bill above 1.2. However, this strength is partly driven by Greater China customers pulling forward demand ahead of a ~15% price increase implemented in March 2026, with regional shipments running ~25% above Q4 levels. Lead times remain elevated at over 26 weeks, constrained by substrate and packaging rather than wafer capacity. With servers accounting for ~60% of revenue and exposure to Intel and AMD platforms, the company also benefits indirectly from AI-related demand. JNK's analysis suggests pricing can support growth even if volumes soften.

Technology

QCOM’s guidance came in weak, but visibility into the end of the handset correction is improving, with orders expected to normalise from Q4. More importantly, confirmation of a hyperscaler data centre win provides tangible evidence that diversification is gaining traction, alongside strong automotive momentum. If the market is finally prepared to look beyond Apple-related risk, then the shares have a lot further to go. QCOM remains one of the few semiconductor names with credible AI exposure that has yet to see a meaningful re-rating, while consensus expectations - currently implying no EPS growth in 2027 - is clearly too low.

Technology

The market is misdiagnosing structural share loss as a temporary slowdown. OWS’s industry checks suggest enterprise weakness is driven by competition from Microsoft Teams and Zoom, while a lack of innovation is reflected in Gartner’s Magic Quadrant rankings. Management’s expectations for high growth from AI and RingCX products appear optimistic, with feedback indicating these offerings are largely undifferentiated. At the same time, aggressive cost cuts in R&D and sales are cited as contributing to customer dissatisfaction and weaker retention. With RPOs (backlog) flat for nearly two years and FCF overstated (adjusting for buybacks reduces 2025 FCF to $196m from $530m and the FCF yield was 5.6% rather than the 15% bulls use to argue that RNG is a cheap stock), OWS sees continued pressure on growth and valuation.

Asia

Industrials

Hamed Khorsand highlights Azul as a post-restructuring opportunity following its emergence from Chapter 11 bankruptcy, which materially reset its capital structure and reduced net leverage to ~2.3x EBITDA. The company eliminated ~$2.5bn of debt and lease obligations, cut interest costs by >50% and is now positioned to generate sustainable FCF. Despite this, the stock trades at ~3.9x 2026 EV/EBITDA, a significant discount to regional peers. The key catalyst is a planned NYSE listing, which should broaden investor awareness and drive a rerating. With a differentiated domestic network and improving profitability, Hamed sees ~70% upside to his (12-month) TP of R$50.

Materials

The closure of the Strait of Hormuz is driving dislocation in ammonia and sulphur markets. AECI is well positioned, sourcing ~85% of ammonia from Sasol’s Secunda plant and avoiding import exposure, while ~50% of global sulphur trade typically transits the Strait. Resulting shortages have triggered sharp price spikes, with AECI monetising existing inventory. Its sulphuric acid business (~R600m revenue, HSD margins) should see a near-term earnings boost (for approx. a quarter based on current conditions). Operations have also improved following stabilisation at Modderfontein. With peer Omnia sourcing ~50% of its ammonia requirements from imports, AECI is better positioned. Chronux expects EBITDA to reach ~R4.5bn by FY27 and increases their HEPS by 10.7% (FY26) and 3.8% (FY27). TP increased to R132 (from R125).

Innolight: AI optics leader targets H-Share listing

Technology

Aequitas offers an early look at Innolight as it aims to raise ~$5bn in an H-share listing (up from ~$3bn in late 2025), potentially making it one of Hong Kong’s largest deals this year. The company is the global leader in optical transceivers and is benefiting from strong demand driven by AI-related data centre capex. Growth has been exceptional, with revenue up 122% in 2024, 61% in 2025 and a further 192% YoY in 1Q26, alongside margin expansion. With revenue heavily concentrated among hyperscalers and shares already trading at elevated multiples (~37x FY26 P/E), the key question for investors is how much of this growth is already priced in.

Developed Markets

Stagflation not spikeflation

Andrew Hunt points out how the 2026 oil shock is now analogous in duration and (almost) severity to the shock in 1973. This is the third or fourth global price shock in six years - people are learning and inflation expectations are no longer anchored. Weak government credibility and a loss of faith in central banks will play a big part. The fact the US and (to a degree) Chinese central banks are accommodating the oil shock via money creation will further encourage inflation expectations. Elsewhere, other central banks appear to be prevaricating over reactions. The clamour for fiscal measures to help people afford oil they may not physically be able to buy will feed inflation, just as it did during the pandemic when aggregate demand was supported even when supply was compromised. We are on course for a second surge in inflation, and Andrew also expects a global recession – or at least near recession – from the middle of this year.

Climate risk is still not priced into markets

David Owen & Marchel Alexandrovich point out that climate risk has not gone away and has yet to be priced into markets. The scientific evidence continues to build; as do emissions in the upper atmosphere. Moreover 2026 will likely bring the return of an El Niño with its associated risks of more extreme climate related events. Recently the ECB examined the effect of extreme high and low temperatures, and high and low precipitation on GDP and inflation, whilst the BIS focused on the challenges faced by Africa. The current energy price shock is a reminder of just how dependent Europe is on imported fossil fuels. Meanwhile the US administration is all in on fossil fuels, and lower GHG emissions are simply not on the agenda. Until the US changes direction, politically, global net zero is out of reach. In the meantime, economies remain exposed to further energy shocks, increased inflation volatility, and damage from physical climate change.

A trade idea in UK rates

The booby prize for worst performance by a DM bank is the UK, claims Brian McCarthy, with the institution allowing a 107-basis point shift in market expectations for year-end rates from a more than 50-basis point cut flipped to a more than 50-basis point hike. Brian finds this incomprehensible. With any luck they will be bailed out by a reversal of the supply shock before they can follow through on a policy error of such magnitude, otherwise the UK economy will be pancaked and driven into an unnecessary recession. Brian likes buying Sept or Dec SONIA futures on a retracement in UK rate expectations upon resolution in Iran. For those who don’t share his confidence that there’s going to be a resolution, he likes selling 9550 puts on September SONIA. Take in 13 and a half bips, so you're earning about half a rate hike. Your strike is 75 basis points away from the current rate. So you're covered for three and a half hikes.

Europe: Uncontrollable hiccups

Niall Ferguson expects euro area headline inflation, measured by the harmonised index of consumer prices, to peak near 3.5% in late 2026 or early 2027 and to return to 2% in 2H2027. This is a higher peak than consensus and a longer return to target than in the European Central Bank’s adverse scenario. The return to 2% inflation was never sustainable. Imported disinflation from Chinese manufactured goods had been masking broad but shallow inflation in domestic services, and the current shock now arrives with no disinflationary buffer. Accordingly, Niall expects the ECB to hike rates by 50 bps by year-end. His views on US and EU rates and inflation translate to a minimally stronger euro than the market is pricing; Niall sees the EURUSD spot price at 1.178 and the one-year forward at 1.193. Europe’s second inflation shock in four years will prove less acute than the first but harder to shake.

US: Going overweight on tech

The Vermilion team remain bullish on the S&P 500 (SPX), Nasdaq 100 (QQQ), and Russell 2000 (IWM). Market dynamics continue to improve ever since the major bullish false breakdowns at 6480-6520 on the SPX, 24,000 on Nasdaq futures (NQ), and $245 on the IWM, with all of them now breaking out to all-time highs and holding above bullish gaps from April 17. Everything that the team sees suggests bulls remain firmly in control, so the team want to be buying any pullbacks for the foreseeable future to the 20-day MA or 21-day EMA. The team discussed adding exposure to growth, and primarily technology, as growth has taken over as leadership relative to value. RS on the cap-weighted XLK is now breaking above its 2025 highs and they are upgrading Technology to overweight. The team have remained overweight semiconductors (SMH, NVIDIA Corp, Taiwan Semiconductor Manufacturing Co Ltd, Ciena Corp, etc.) and memory (SanDisk Corp, Western Digital Corp, Seagate Technology Holdings PLC, Micron Technology Inc) ever since last June, and these remain their favourite areas within Tech.

US: Warsh ready for prime time at the Fed

Based in part on his previous interactions with Kevin Warsh, the prospective next Fed Chairman, John Ryding discusses what he is likely to do when he takes over on 15th May. John says that Kevin understands complex economic arguments but is not wedded to conventional academic wisdom. Kevin hates inflation and firmly believes that it is a monetary phenomenon and that the Fed must take responsibility for it. Although Kevin feared at one point that the Fed might raise its inflation target to 3%, he seemed adamantly opposed to the idea. Kevin brings a great depth of institutional market knowledge to the Fed, which it desperately needs, and is willing to think outside the box. In his prepared statement to the Senate Banking Committee, Kevin made it clear that he believes “monetary policy independence is essential. Monetary policymakers must act in the nation’s interest . . . their decisions the product of analytic rigour, meaningful deliberation, and unclouded decision-making.”

US: Emerging trends

Konstantin Fominykh comments that his rotation into Defensives might look like a late cycle playbook, but it is very possible. He points out that staples sold off as the war in Iran threatened commodities inputs, but they offer earnings stability with improving pricing power as input costs normalise. He’s initiated buys on the likes of AMZN, HD and CVNA. He’s also buying into healthcare (XLV), which is already up +16% since his purchase on Apr 16th, and US healthcare equipment (XHE). He also keeps his buys on real estate and utilities, with the former up +11% and latter up +20%. Lower rates (buy on 10YUS) make these rate-sensitive sectors more attractive. Meanwhile, tech is extended and positioning overcrowded, and risk/reward is deteriorating vs defensives.

US: The Fed’s struggle for financial mastery

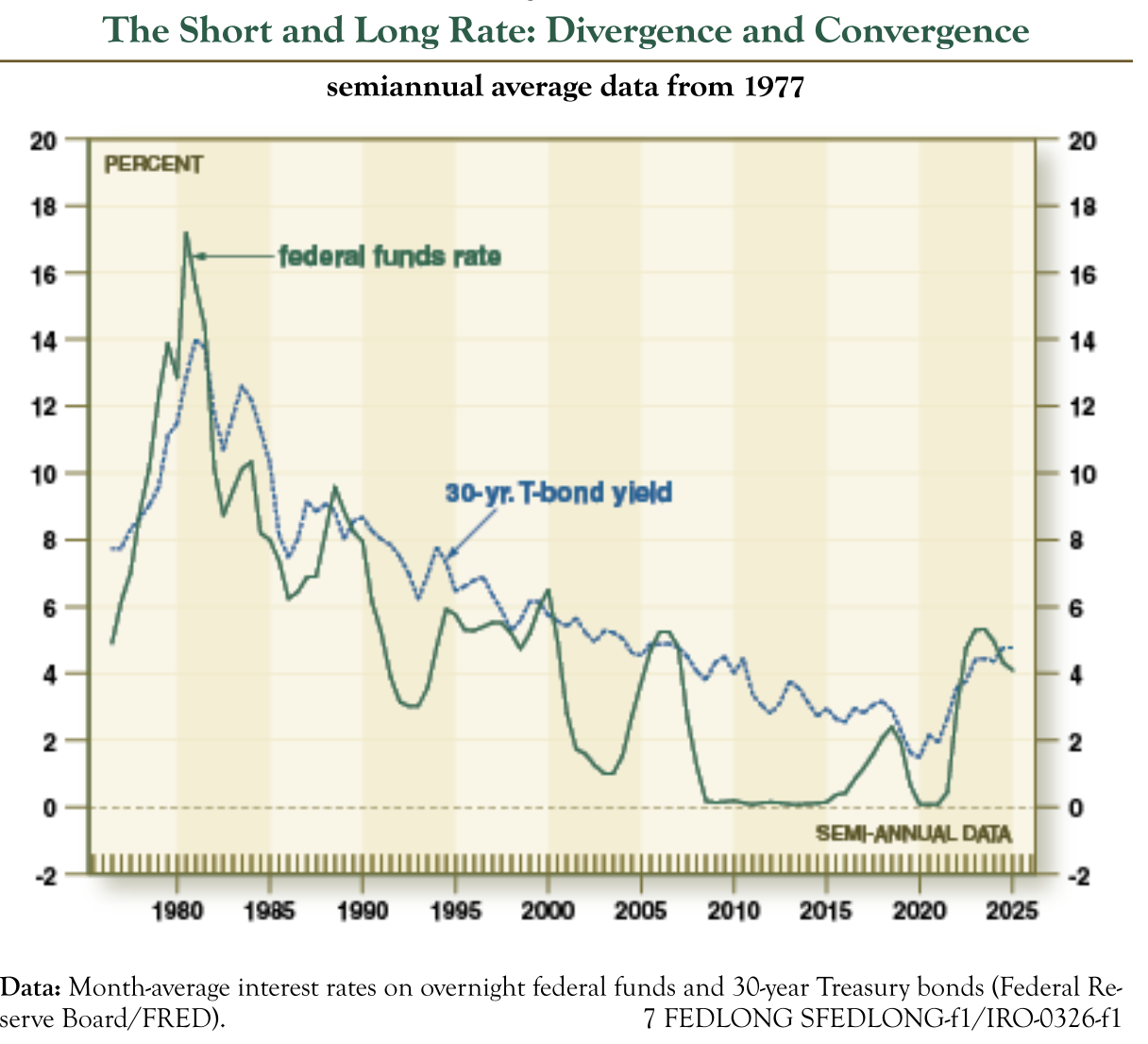

Past research by David Ranson suggests that long rates show very little response to Fed policy. Even after the most vigorous attempts to impose the Fed’s policy rate on the term structure, the short rate tends to converge toward the long end of the curve. This is compatible with evidence that during the past 25 years, the measured influence of changes in the 30-year T-bond yield on real growth and inflation has exceeded that of the Fed’s policy rate (see chart). The chart shows how sudden divergences between the two ends of the yield occur occasionally, in every case crated by a rate cut at the short end. The slope of the yield curve remains steep for a few years until re-convergence begins, which is attributable to a reversal in Fed policy and not a response of the long rate to the Fed’s cutting. On average, complete reversal takes four years. Rates are governed by market forces, not monetary policy.

USD / Singapore Dollar

Chris Roberts examines the Singapore Dollar (SGD), which appreciated against the USD from the end of 2001 until the summer of 2011. The USD fell 35% during that time. Following a modest retracement of losses in 2011-2017, the USD was rangebound for 8.5-years. Towards the end of that period, the USD failed to reach the top of the range and in recent months it has broken down again. The breakdown from the rectangle targets a fall to USD/SGD1.1625. Note that the MACD is below the Zero Line again, reflecting negative USD momentum. Go 200% short at market. The stop is a daily close above USD/SGD1.3228.

Japan: Yen under the cosh

The yen breached Y/$1.60 on Thursday and JGBs are under pressure again after Trump signalled that a prolonged blockade on the Strait of Hormuz may be necessary. Ironically, Graham Turner points out that it may not be the inflation numbers that undo the Japanese bond market: the data had been benign in recent months and the BoJ has time on its side and can wait. The problem is the Japanese Government’s insistence that it can hike defence spending, without compromising on other areas of spending. Markets had been persuaded by the new prime minister’s claim that a "responsible expansionary fiscal policy" could work. Ironically, the trade and manufacturing data in Japan suggests that the Takaichi Government can be more prudent: it can afford to accommodate higher defence spending without resorting to more borrowing. It just chooses not to. The long end of the JGB market will react before too long.

Multi-managers: Key trends in technology, operations, platform growth

A new 20-page AFI research report focuses on multi-managers, the hedge fund sector's key driver of industry growth this decade, and provides unique insights into their operational footprint, tech deployment and future priorities. The report, sponsored by SS&C and based on extensive research and a survey of 100 members of the global hedge fund industry in Q1 2026, shows how AI and talent are defining 2026 themes for the sector. Click here for your free download, which serves as a showcase of the AFI Intelligence product.

Emerging Markets

Argentina: Make hay while the sun shines

Marcos Buscaglia comments on a challenging year of debt services ahead for the government and central bank. Even if debt with the IMF and other multilaterals is rolled over, the debt maturing next year is very high with total hard currency debt services nearing $36bn, of which $18bn pertain to bonded debt. The government already squandered an opportunity to tap markets at the beginning of the year, when the risk appetite for Emerging Markets debt was high. Marcos believes the government is reluctant to issue market debt because of the inevitable rise in interest bills, but he finds that this is both inevitable and not worrisome in the short term. He believes the market is more than willing to take on new Argentine debt, with 10-year rates possibly dropping to low 9s. The government should take advantage.

Bulgaria: Investor confidence unlikely to be boosted

Bulgarians headed to the polls last week as Progressive Bulgaria won the election, with Rumen Radov. However, Mario Bikarski points out that the absolute majority could help to avoid government instability, but challenges remain for the administration. The biggest one will be getting through a 2026 budget, the issue that collapsed the previous government. Maintaining generous social transfers whilst adhering to EU-mandated low-debt and deficit commitments is a tight balancing act. Progressive Bulgaria has yet to present a credible budget plan to find that balance, Bikarski warns. Fitch nevertheless confirmed its BBB+ rating with a stable outlook. More problematic for investors and credit risk is the persisting political risk and governance deficit. The fight against corruption will be central to any coalition negotiations. Under EU pressure, some judicial reforms are likely to go ahead in 2026. However, progress will be piecemeal and probably insufficient to meaningfully boost investor confidence.

Chinese Gen Z traders

Charles Hess observes that from 2016 to 2022, US adults under age 35 went from being the least likely group to have a brokerage account to the most, according to the Federal Reserve. But young traders were slower to materialize in China – until recently. From September 2024 to January 2025, the number of investors under age 30 in China doubled, accounting for about one-third of the country’s retail investor base of 240 million traders. Investors under 35 are behind more than 45 percent of new trading accounts opened last year, up five percentage points from the previous year. Charles notes that China’s tech-savvy Gen Z traders are a new and large generation that is much different than prior generations who had assiduously put their money in savings accounts to make up for a lack of government safety nets. With the new generations of investors’ help, the benchmark CSI 300 Index rose 18 percent in 2025, the best year since early in the pandemic.

China: Support for economic growth

Recently the State Council issued guidance on “productive services” (shengchanxing fuwu) in the Service Sector. This confirms what William Hess has been saying about official expectations for the composition of growth over time, that policymakers see the largest potential share gains coming from services (tertiary) output, and within that category see greater room for “productive services” expansion over “living services”. The State Council wants to see total service sector output surpass RMB 100 trillion by 2030, up roughly 23% from current levels, which should raise services sector output to close to 65% of GDP. Meanwhile William continues to expect Vice Premier He Lifeng to deliver some form of growth support and/or easing measures for financial conditions by mid-May. On activity, China has given back most of the Q1 gains observed in March, presumably as a function of Hormuz crisis effects, and so by now the leadership has a clearer picture of what they need to do.

Senegal: Ongoing talks but as yet no IMF programme

Maximilian Hess observes that Senegal is in the throes of a financial crisis caused by the revelations of large amounts of ‘hidden’ debt contracted by the previous government, that has seen an additional 20-30% of borrowing as a percentage of GDP uncovered. The government has leaned on its monetary union, WAEMU, to meet its debt service with local currency issuance. While the WAEMU market has demonstrated surprising liquidity, Senegalese and regional banks are approaching (or have met) their regulatory limits for state debt. Senegal is negotiating with the IMF for the resumption of a USD 1.8 billion facility suspended in October 2024. The Fund noted strong GDP growth, better-than-expected primary and current account performance, and moderate inflation, in 2025, though it expects Senegal’s fiscal and macroeconomic picture to materially deteriorate in 2026. The IMF said that ongoing talks are “complementary to a programme” but are primarily on structural reforms and capacity development.

Thailand gets even weirder

Stagnant, stagnant, stagnant. Thailand remains completely depressed at home, with no sign of buoyancy in any of the domestic indicators that Jonathan Anderson covers. Trade is exploding ... but it's all "throughput". By contrast, the Thai trade numbers are shooting up dramatically - but just as Jonathan has highlighted for the rest of East Asia, this is (i) all concentrated in IT/electronics goods headed for developed AI investment, and (ii) it's also all "round-tripping", with an explosion of imports from China matched by an explosion of exports to the US and to a lesser extent Europe. As a result, there's surprisingly little impact on the local economy. In the meantime, he doesn’t see much to do in Thai assets. There's not a lot of earnings growth in the equity market, and local yield and carry are extremely low. Basically, Jonathan is waiting for the country to start spending again.

Commodities

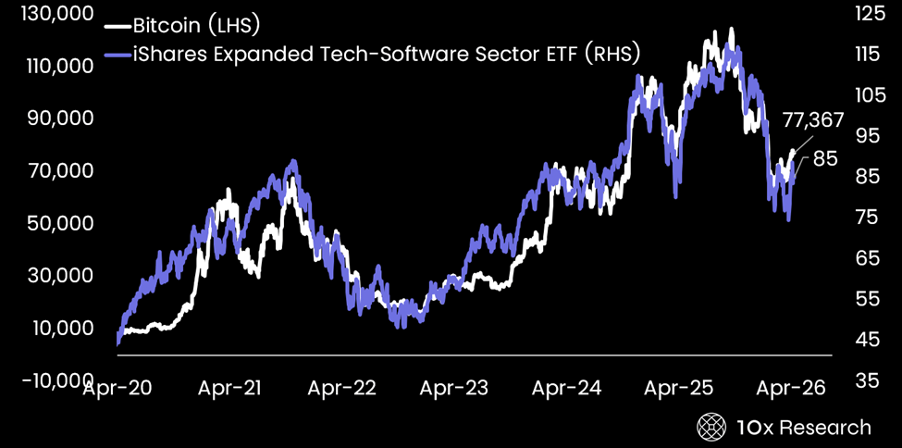

Bitcoin is not a tech stock

Bitcoin has spent the past several years trading in near-perfect lockstep with high-growth software stocks, rising and falling with the Nasdaq as if it were just another tech bet. But Markus Thielen says that reading is wrong, and the mispricing it has created may be one of the most important opportunities in this cycle. The correlation with tech stocks reflects the current composition of Bitcoin's investor base, not Bitcoin's underlying value proposition. Bitcoin's investment case rests on its monetary properties: fixed supply, no counterparty risk, censorship resistance, and its role as a hedge against dollar debasement and sovereign fiscal excess. These characteristics have nothing to do with software earnings, AI adoption curves, or interest rate sensitivity to growth expectations. The more useful framework is to track Bitcoin alongside gold, dollar liquidity, and real interest rates, the variables that govern monetary asset valuations. Bitcoin tends to outperform when real yields fall, when the dollar weakens, and when sovereign debt concerns rise. Those are the signals that matter.

Copper: Lack of supply growth vs rising inventories

David Radclyffe's copper coverage totals ~63% of global mine production. Copper supply continues to wrestle with many legacy headaches from 2025, mixed with the Iran conflict and its implications for diesel and sulphuric acid supply. There is therefore downside supply risk. However, the current oil disruption has implications for global growth and copper demand. Worryingly, David points out that copper inventories are rising rapidly. His coverage universe implies 0.9% annual contraction in refined copper supply in 2026, following a strong 2025. Weak supply growth for 2026, even with moderate demand growth, is at odds with strongly rising terminal market inventories, now at 1,267kt, adding to price risk. Copper is a crowded long trade, with caution warranted. The sector is not particularly cheap at spot 1.6x P/NPV10 and 9x EV/EBITDA. Antofagasta PLC is cut to HOLD. Preferred stocks include Lundin Mining Corp, KGHM Polska Miedz SA, Ivanhoe Mines Ltd, Grupo Mexico SAB de CV, Hudbay Minerals Inc and Teck Resources Ltd.

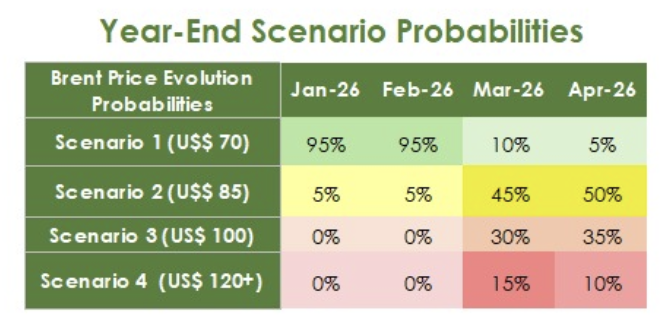

Oil: Predictions for year-end

Brent climbs higher, reflecting the ongoing stalemate between the US and Iran and, above all, the lack of concrete progress in negotiations. The cancellation of the trip of US envoys to Islamabad reinforced the perception that, despite the formal maintenance of the ceasefire, the diplomatic channel remains stalled. At the same time, signs of greater pragmatism from Iran are beginning to emerge, with the possibility of a provisional agreement involving the reopening of the Strait of Hormuz in exchange for partial relief of restrictions imposed on Iranian ports. Even so, US resistance to easing the blockade and regional pressure, especially with the continuation of attacks in Lebanon, keep the geopolitical environment quite fragile. The DayByDay team assign a 50% probability to Brent being priced at $85 by year-end, and 35% that it’ll stay around $100. They see only a 10% chance of prices staying above $120.

Gold and silver entering a new phase

In his latest presentation, Jeffrey Christian of CPM Group discusses the recent movements in gold, silver, platinum, and palladium prices, focusing on the sharp decline in gold and silver and the consolidation pattern developing across precious metals markets. He explains why, despite the recent drop, prices remain within the range that CPM Group has been outlining, and why the current environment continues to point toward a period of sideways, volatile trading rather than a sustained breakout. Jeff discusses how seasonal trends, macroeconomic conditions, and investment demand are interacting to shape price behaviour over the coming months. He discusses the growing likelihood of a consolidation phase through the summer, while noting how economic and political developments could still cause short-term price fluctuations.

Click here to watch.