Europe

Shorts continue to deliver strong alpha

Vision initiated 5 new shorts and closed 9 in Q1. Regarding the closed shorts, alpha ranged from 46% on the high end with AAK, to 6% on the low end for Assa Abloy. Other closed shorts included Fluidra, KION Group, Dorman Products, Planet Fitness, Pop Mart, Smoore International and Techtronic Industries. Consistent with Vision’s pursuit of liquid and non-consensus ideas, the 5 new shorts in Q1 had median average daily $ volume of >$150m and median short interest % of free float of 2.5%. Their new shorts include European luxury, European telco, European cap good, US restaurant and US healthcare.

Consumer Discretionary

The shares have been volatile over the past few years from plunging on UK RevPAR softness, before rallying on trading beats, only to fall again following the UK Budget and more recently amid geopolitical tensions in the Middle East. The result is that it is remarkably cheap and structurally well-positioned to benefit from an inevitable normalisation in travel demand and easing macro restrictions. Ongoing estate optimisation and conversion-led expansion underpin growth towards ~98K UK rooms by FY30. While near-term margins face pressure from business rates and inflation, cost mitigation and efficiency initiatives support ~22% medium-term margins. Germany is approaching profitability and represents a key growth driver. Despite elevated capex, the balance sheet remains solid and shareholder returns intact. WTB offers compelling upside potential based on fundamental valuation metrics, supported by a favourable ESG profile. TP £31.79 (35% upside).

Consumer Staples

Rocky Road Rebate Accounting - MICC’s first post-demerger annual report flagged multiple red flags, with Forensic Alpha’s primary concern centred on working capital and off-balance sheet exposure. In FY25, incomplete disclosure - particularly around rebates processed via Unilever under an agency model - leaves investors unable to determine the total rebate accrual. However, balance sheet movements are consistent with a potential reduction, which could inflate revenue. This sits uneasily with management’s emphasis on “volume-led” growth, where discounting would typically remain elevated. While no misstatement is identified, limited disclosure in such a high-risk area warrants close monitoring and a fuller explanation from management. Forensic Alpha increases MICC's Risk Score to 8/10.

Financials

The market is missing a key earnings driver as ~20% of AUM is currently fee-free but will convert to fee-paying over the next 6 years. This creates a LDD CAGR on the top line without requiring market growth. With a largely fixed cost base, STJ can deliver ~10 points of margin expansion through 2030. Additional bull points flagged include STJ’s success in capturing the next generation of wealth (one third of clients are under the age of 40); while AI-driven efficiencies could unlock ~30% productivity gains and further consolidation within the advisor ranks. The stock trades on ~15x depressed earnings but ~5x 2030 earnings, with ~70% of cash returned via dividends and buybacks. TP £22.00 (80% upside).

Technology

The group's competitive moat is anchored by three mutually reinforcing advantages: 1) a proprietary, cloud‑native payments infrastructure with direct integrations into 50+ national payment systems across the world, creating a durable cost leadership position that compounds with scale; 2) a Mission Zero pricing philosophy, that continuously reinvests operational efficiencies and scale benefits into lower prices, driving organic volume growth and deepening customer stickiness; and 3) a growing platform business, which is transforming potential competitors into distribution partners, expanding the company's netting pool and lowering unit costs across the entire network. 2Xideas forecasts 14.7% revenue CAGR and 15.9% underlying income CAGR to FY32E. Assuming a conservative 20x exit NTM P/E, this supports ~17.5% annualised TSR.

While revisions have deteriorated again for Willis Welby’s Media coverage, the median implied to Y3 EBITM ratio of 40 is very low. They continue to highlight Benefit Systems, which has good financial productivity and a clear growth story in Eastern Europe and Turkey. Although some investors may not like the geographical exposure, this looks like a business that should compound well for shareholders. The share price has fallen back in recent market turmoil and the implied to Y3 EBITM ratio is 70 which still leaves a lot of potential. They also flag Vivendi, where the SOTP story looks to be way above the current share price. It still looks like a very cheap call on Universal Music in particular, given the expectations ratio here is now just 50.

North America

Minimising losses, maximising gains: Second buy signal activated

ViewRight's Defender Program has activated its second tactical buy signal following the S&P 500’s close below 6,375, bringing deployed exposure to 25% of its predefined allocation (out of a 40% maximum). The framework continues to operate within a healthy bull market regime, with no evidence of deterioration in market breadth or participation preceding the recent pullback. Historical analysis provides important context at this stage. Since 1988, drawdowns reaching this level have typically followed one of two paths: stabilising and recovering near current levels, or progressing into deeper and more prolonged declines. Notably, 91% of such episodes resolved before requiring further deployment. Defender’s rules-based approach is designed to systematically add exposure into periods of weakness within healthy bull markets, removing discretion and maintaining discipline across a range of outcomes.

Communications

While the market treats APP as an AI play, Andrew Freedman sees it is an infrastructure monopoly story. APP’s true moat is MAX, its mediation platform controlling >60% of mobile gaming impressions and supplying the auction data that powers AXON - without it, AXON’s performance is materially weaker. Andrew’s analysis includes how the company's 2025 game divestiture created a structural data deficit; why the identity graph is more fragile than the market appreciates; how E-Commerce scaling faces a bifurcated reality; why the mediation monopoly is under attack and the spread is unsustainable; and, how the regulatory cascade creates asymmetric downside.

Discounters dominate top retail long ideas for Q2

Consumer Discretionary

John Zolidis continues to favour discount retailers for Q2, as persistent inflation from tariffs and high gas prices is expected to outweigh any stimulus tailwinds. Within the space, he highlights Five Below as the best unit growth story in retail, while Dollar Tree offers upside from a successful multi-price transition. Dollar General is improving execution, recovering margin and driving traffic with a lot of room to go relative to previous results. Savers Value Village stands out as a mispriced growth story at <7x EBITDA. Beyond discount, Sprouts Farmers Market should see comps recover on affordability, while National Vision remains an early-stage transformation story. Rounding out the basket are Boot Barn, supported by favourable Western wear trends, and Academy Sports, a cheap, heavily shorted name with comps turning positive.

Healthcare

Aaron Fletcher’s short thesis on IBRX centres on a disconnect between hype and fundamentals. The company remains a single-product story with a limited bladder cancer indication. Despite a +280% YTD stock surge and a stretched ~73x P/S multiple, revenues are modest (~$113m) and Anktiva sales growth is already slowing, while the business continues to burn ~$350m annually. The rally has been driven by CEO-led hype, culminating in an FDA warning letter. Aaron also highlights increasing competition and near-term catalysts. He pitched IBRX at our latest Best Equity Short Ideas Conference - click here to listen.

Healthcare

The best-kept secret in healthcare - MDLN is described as a category killer with best-in-class distribution assets delivering HSD-to-LDD% EBITDA growth, a long runway and wide moat. Its model creates a powerful flywheel, using distribution as a loss leader to lock customers into higher-margin private-label contracts. There is a “coiled spring” in earnings from FY27-30 as customers migrate, driving significant margin expansion. The company is also an AI beneficiary via its partnership with Swisslog, supporting further efficiency gains. As a newly public name, MDLN remains underfollowed, with valuation better framed against MRO distributors, elite big-box retailers or growth MedTech. There is scope for a 35-40x multiple, implying ~$70/share (~60% upside).

Industrials

Eric Fernandez expects AAON to miss estimates over the coming quarters, driven by backlog deferrals and margin pressure. He argues consensus is over-extrapolating recent growth, while the company’s exposure to data centre cooling is less attractive than perceived, as the market shifts towards immersion/direct-to-chip cooling. Backlog quality is also a concern (AAON included a new risk factor for the first time this quarter), with hyperscaler customers able to defer orders and already benefiting from looser payment terms. Cash flow is weak and working capital is building, with receivables slowing from ~50 to ~90 days over the past 2 years. Finally, a change in revenue recognition is pulling sales forward, at least partly driving recent positive surprises.

Industrials

Stands to benefit from ongoing supply chain disruption, with Hamed Khorsand highlighting HWKN’s domestically sourced inventory and production capabilities as a key advantage. The Iran conflict has tightened global supply, allowing HWKN to capture higher pricing and margins in its industrial segment, which is more exposed to spot pricing. The company has historically benefited in such environments and the disruption is expected to support both fiscal Q4 (end Mar) and Q1 (end Jun) performance. Additional upside may come from liquid phosphate sales, as shortages of dry phosphates push farmers towards alternatives. While water treatment remains more contract-driven, seasonal demand and recent acquisitions should support steady growth, with near-term earnings likely to surprise on the upside. TP $200 (30% upside).

Technology

The semiconductor distribution channel is posting ~40% Q/Q revenue growth in 1Q26, but the composition tells a more nuanced story than the headline suggests. JNK's supply chain checks show 800G optical module demand at a 2-year high, with all global Tier 1 makers pulling orders and Broadcom Tomahawk 6 extending the cycle into 2H26; simultaneously, the ASIC-to-GPU semi revenue mix is shifting from 80/20 towards 60-70/30-40, positioning MRVL as the most direct beneficiary. On the consumer side, Apple/iOS is outperforming seasonal patterns (+10% Q/Q vs. flat expected in Q4), though component buyers stocking ahead of tariff increases are raising H2 inventory correction flags. The divergence between data centre acceleration and consumer pull-in risk shapes the setup for H2.

Quantum utility likely to arrive before 2030

Technology

Rosenblatt analysts believe commercial quantum utility will arrive before the end of the decade, will be significantly disruptive and that investors should care. Their 30-page report helps investors get smarter on quantum as we move towards an integrated AI-quantum world. If there is one key takeaway, it is that quantum computers will likely bring tectonic shifts to the economy by enabling room-temperature superconducting, customised pharmaceuticals and more efficient production of fertiliser - markets where better solutions could have an economic impact of ~$10trn. They see opportunities to benefit from this shift in buy-rated IonQ, D-Wave, Quantum Computing and Rigetti.

Emerging Markets

India: Channel checks indicate strong execution divergence across sectors

Ola Electric raises the sharpest concern, with 10+ store closures in Gujarat. This raises a fundamental question: is the company recalibrating its EV ambitions, or quietly scaling down retail presence? The situation draws uncomfortable parallels with governance concerns seen in other high-profile cases where investor messaging lagged underlying reality. Elsewhere, Lenskart continues to scale effectively, with strong tier 3/4 traction and lean store models. Campus remains stable but with limited operating leverage. Bluestone carries high vendor-funded inventory. In financials, Affordable Housing Finance faces structural constraints while Personal Loans exhibit rising borrower leverage, highlighting emerging risks beneath stable demand trends.

Petrobras: +72% outperformance in just 11 weeks

Energy

Looking at the 50 biggest stocks in the Emerging Markets universe, Crystal Shore currently ranks only 6 in their 1st (Top) Quintile. One of these 6 is Petrobras. They upgraded the stock to their Top Quintile on Jan 19th of this year. Over the ensuing 11 weeks, the stock has delivered a +64% return (USD). MSCI World (USD) was down -8% over the same time period. The 5 other Top Quintile stocks today are China Construction Bank, Bank of China, BYD, Fubon Financial and FirstRand. Crystal Shore ranks 1231 stocks every week in their GTL and GTM datasets.

Financials

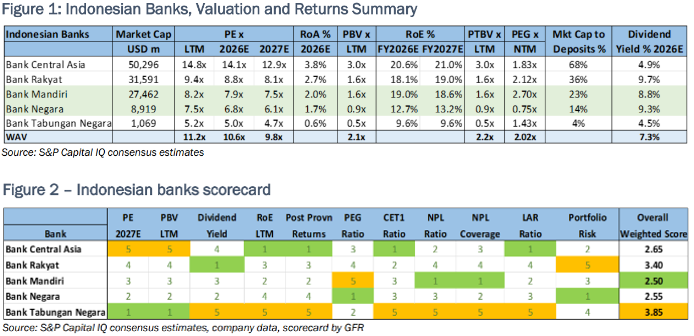

Victor Galliano upgrades Bank Mandiri and Bank Negara to Buy on better-than-expected credit quality, attractive valuations and signs the government is reining in market-unfriendly policies. Both banks screen well on fundamentals (fig 1) and in his proprietary scorecard (fig 2). Mandiri is his top pick, driven by strong credit quality and solid returns, supported by mid-ranking valuations. Low NPLs underpin a declining cost of risk and improving post-provision returns, while returns relative to valuation are very attractive. With PBV near a three-year low and bond yields elevated, he sees scope for a valuation uplift if yields ease. Negara’s valuations are close to deep value and, although return trends remain uninspiring, it has the lowest MSME exposure of the peer group and second best NPL coverage.

China Industrials: Two high-conviction ideas with global demand drivers

Industrials

Ninebot (689009 CH) - Revenue +50% in 2025, electric two-wheeler profit +62%. The lawnmower robot business grew +124% and is structurally positioned to benefit from EU policy-driven industry consolidation. Dual-brand strategy (Ninebot + Segway) targeting 20% market share. This is a Chinese industrial with genuine European distribution infrastructure - a rare combination given current geopolitical sensitivities around China supply chains.

Oriental Cable (603606 CH) - RMB 19.3bn order book, 60% in high-value submarine and high-voltage cable. Delivered UK Inchcape project ahead of schedule. China offshore wind accelerating to 12GW+ in 2026, European energy independence driving parallel demand and high-margin export cable mix rising. The 15th Five-Year Plan implies installed capacity doubling vs. the 14th. Order visibility is as clean as it gets in Chinese industrials.

Developed Markets

The reality behind humanoid robotics

Report by

BCA Research

BC

Humanoid robotics are hitting the news every day, but the BCA team point out that they are not yet an imminent investment theme. The industry remains in a nascent, pre-commercial phase, with only 13,000 units shipped in 2025. Some estimates value the industry as already worth up to $5bn, but often include wheeled social robots and software/services bundles. As it stands, they are not significantly contributing to the manufacturing process. Generative AI’s rapid progress has boosted optimism, but self-driving cars show how easy it is to underestimate the complexity of physical AI. Significant bottlenecks remain, with an 80-90% cost reduction and improved battery life needed. For those looking to invest, several ETFs present possible long-term plays, including BOTZ and ROBO. Given the importance of battery life, the battery tech supply chain is another way for investors to play the automation theme, with options including LIT, BATT and LITM.

Turning cautious ahead of the obvious

Konstantin Fominykh’s tools turned cautious before the markets saw the obvious, having initiated sell signals on the S&P500 and US industrials on Feb 9th (before the 9% and 8% drops), US healthcare since Feb 3rd (7% drop), US tech (11% drop) and Bitcoin (38% drop). The Middle East situation is worsening. Private credit signals a prolonged contraction; default rates appear low on the surface, but adjusted measures suggest significantly higher stress, with effective defaults closer to ~6.4%. Konstantin is selling US financials. He also remarks that the AI/tech trade is not working because everyone already owns a lot of it, and has a fresh sell on AI and Next Gen Software ETF (March 23rd). There is a likely recession ahead catalysed by a reversal in AI capex and the energy supply shock; expect earnings to peak Q1-Q2. Investors were spoiled by the 16-year bull market, so it’s no surprise that people still believe in "strong earnings" and "buy the dip".

UK equity market briefing

As a direct result of higher petrol prices, CPI inflation is likely to increase to around 3.25% in March. Darren Winder explains that this needs to be balanced against the impact of base effects and the reduction in the energy price cap. Overall, his arithmetic shows inflation dipping below 3% in April. If maintained at recent levels, sharply higher wholesale gas prices are likely to result in the energy price cap rising by around 20% over July-September. Without policy interventions (which are likely), this would add ~0.5% to CPI and contribute to higher government debt interest payments. On his current arithmetic, CPI averages around 3.25% in 2026. As energy price pressures subside, CPI will fall towards the 2% target during 2027. This allows policy interest rates to resume a downward path. The jump in market interest rate expectations, to well over 4%, will, in Darren’s view, prove to be relatively short-lived as Bank Rate is maintained at 3.75%.

Equities downgraded to neutral

Sam Burns has downgraded equities to neutral and raised cash in response to a deterioration in his indicators and increased macro risk and may do so further. Since the beginning of March when the US/Israel-led war in the Middle East started, his Equity Risk Model has deteriorated further, now below the 50% level and thus no better than neutral. While equity P/E ratios have declined, higher bond yields have largely offset the rise in earnings yields, leaving his Implied Growth Model still at elevated levels. Macro uncertainty has surged (again) and investors are focusing on how long and how bad the supply disruption in the Middle East will be – markets expect just a few months, but that timeline is gradually lengthening as escape routes for Trump are reduced. The positives are that earnings estimates are holding up so far, and short-term oversold conditions are in place.

The US faces sharper inflation from crude than the UK

It is true that the UK is more susceptible than most to energy fluctuations, which is slightly ludicrous given its access to North Sea oil & gas reserves. It is also true that due to duties & taxes British drivers pay roughly 80% more to fill up their cars than their American counterparts. Yet these very taxes shield consumers from crude oil volatility. So far in March, even as oil prices rise over 30% y/y, petrol prices on British forecourts have risen by 9.6% y/y whereas US comparative “gas” inflation at the “pump” is 22% y/y. In other words, twice as bad, despite the US’s much acclaimed self-sufficiency (which is not entirely true). Despite what many believe, the reality is that the US inflationary impulse is greater than the UK’s with respect to petrol.

US: Down to bearish

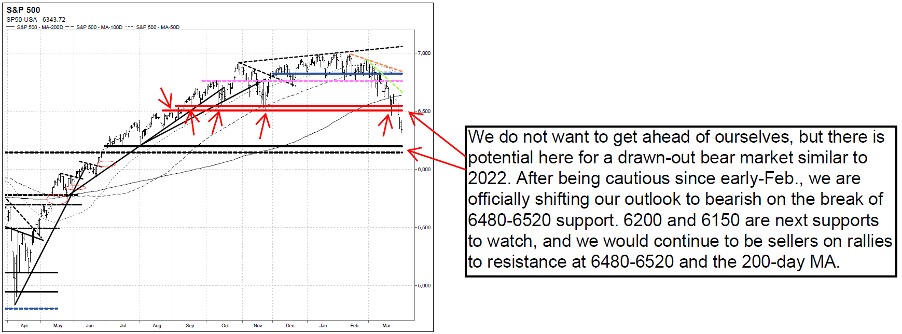

The Vermilion team are officially downgrading their outlook to bearish with the S&P500 (SPX) violating major support at 6480-6520, Nasdaq futures (NQ) violating 24,000 support, and the Russell 2000 (IWM) breaking down below crucial $245 support. This comes the team downgraded their outlook to neutral early in March. Concerns that they discussed since early-February stemmed from deteriorating market dynamics, and ever since then they been concerned about a deeper pullback, likely to 6720-6776, 6690, or 6480-6520 on SPX, while also discussing since mid-March how downside capitulation is likely needed before finding a reliable bottom. With continued deterioration in market dynamics, their report last week discussed how they were closely watching for a breakdown below 6480 and that the SPX likes to test the 200-day MA as resistance (from below) before continuing lower, and this is likely what happened on 3/23/26. 6200 and 6150 are the next supports to watch, and they would continue to be sellers on any rallies to 6480-6520 and 200-day MA resistances.

US: The Private Credit Crunch

US money and credit growth has slowed over recent weeks, and Andrew Hunt believes the Private Credit Crunch may be intensifying. If private finance had indeed become the principal source of external funding over recent years for the now significantly cash flow negative US corporate sector, then the ongoing problems in the private channels will now be causing a binding credit crunch that will likely further suppress economic growth, even before the impact of higher energy prices. This will impact the AI sector. The impact of the Big Bill may offer some near-term support to growth, but Andrew suspects that by Q2 the economy may be soft – a recession may be due to arrive in H2. Investors can expect the FRB to remain active in the debt markets and to press ahead with rate cuts next quarter. If global capital flows continue to stall then the USD will weaken. Under this scenario, UST yields could continue to rise until the FOMC is forced into YCC.

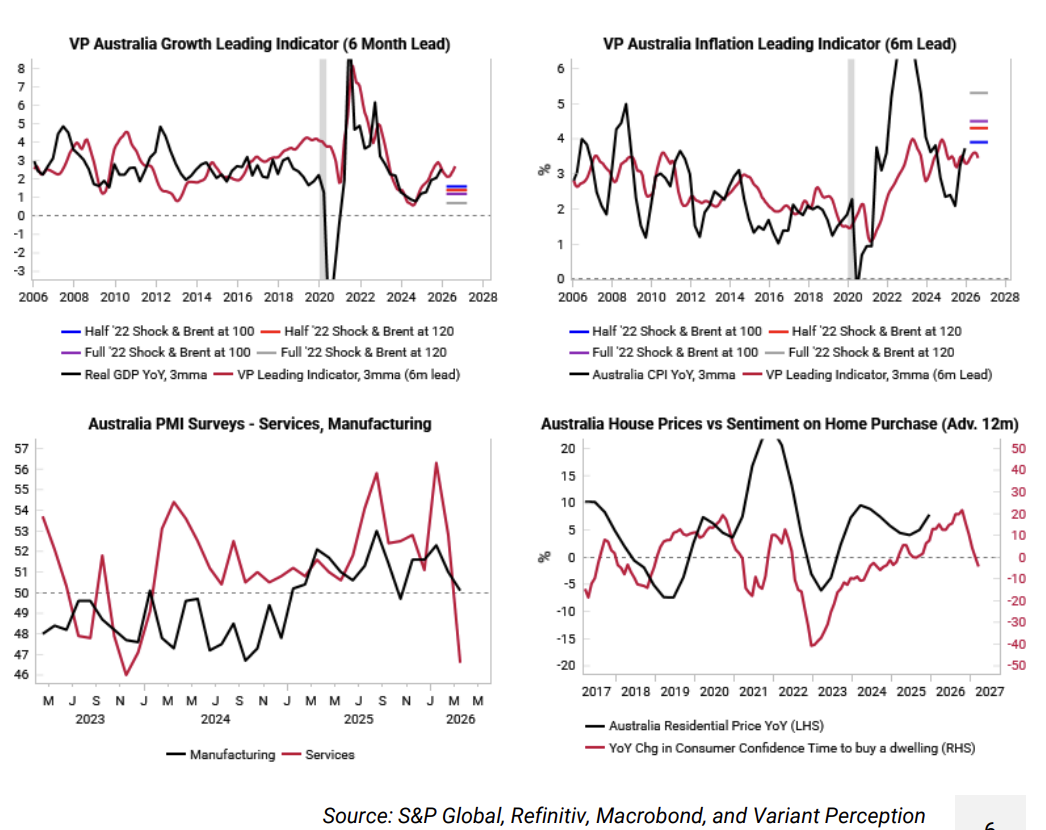

Australia: The lucky country

The Variant Perception stress-tested countries to identify the ones most resilient to energy shocks, with Australia coming out on top thanks to its coal and LNG exports. The team’s range of scenarios show that inflation should remain below the 2022/23 highs. This outlook should reinforce the RBA’s ongoing hawkish stance; at face value, a hawkish RBA and positive terms of trade shift would point to a stronger AUD, but there are signs that a bigger downside growth shock is possible. Both services and manufacturing PMIs were already rolling over before the Iran conflict, which should give the RBA reason for pause, and housing sentiment is weaker today than 3 years ago. Long AUD has been a popular trade that has worked well YTD, but it is going through a correction now given elevated long speculative positioning and a previous LPPL sell signal. The team are waiting for their tactical models to signal a better time to go long the AUD again.

Emerging Markets

Argentina: A once-in-a-generation opportunity

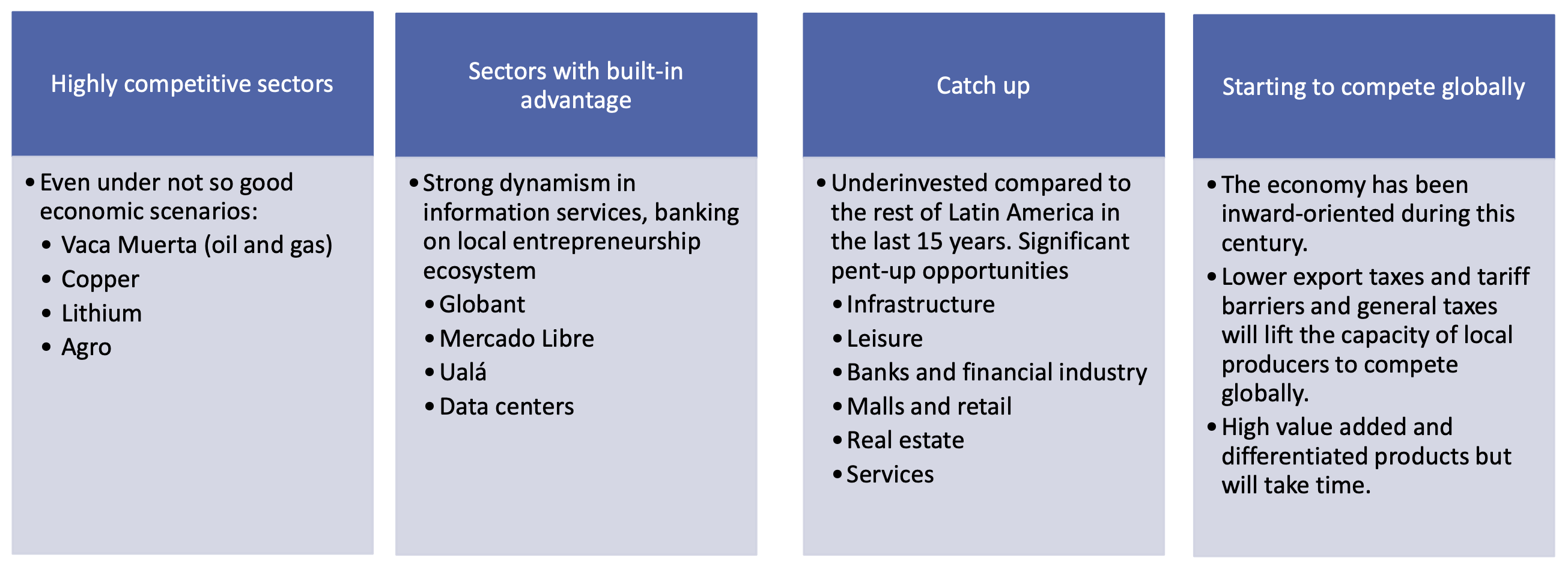

Marcos Buscaglia deep dives into Argentina and points out how the government is implementing two important transitions at once. First, a structural change in growth strategy from a protected economy to an export-oriented one and from regulation to deregulation. Second, the implementation of an inflation stabilisation effort. The last two years have seen an impressive set of reforms, although the labour market has deteriorated, the credit market remains slow and troublesome, and interest rates jumped into high and volatile territory. Marcos sees the economy remonetising with credit penetration rising, allowing the central bank to purchase reserves without a big sterilisation effort. He also sees investment rising, with high capex and soaring exports, particularly in energy, mining and agro. Opportunities lie in several sectors and themes, including copper, lithium, agro and information services (see chart).

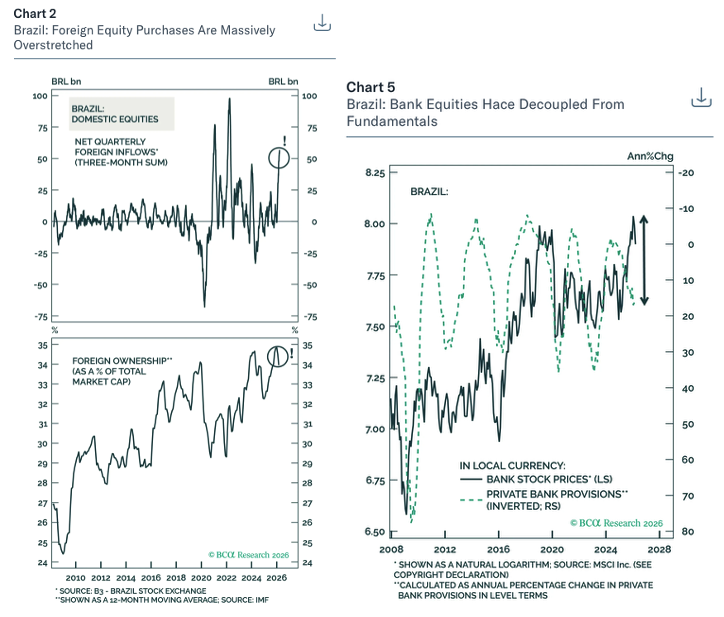

Brazil: Overhyped

Report by

BCA Research

BC

Should investors buy the dip? The BCA team think not. The recent bull market has been fuelled by unsustainable foreign inflows and is massively overstretched (see left chart). The divergence between rising stock prices and worsening macro fundamentals has become untenable (right chart) – investors are too sanguine. Domestic demand will worsen, with odds of a recession rising for the next 6-12 months. The only factor that can prevent such a drastic economic slowdown is major fiscal easing, yet this would cause markets to sell off. Some investors argue that high commodity prices will bail out Brazil, which is theoretically correct, yet in the past this has brought down equities due to the global growth recession it causes. Commodities also matter far less to Brazil’s stock market today. Stay underweight Brazil in equity and fixed-income portfolios. The team also recommend a new short-term trade (three-month horizon): Pay 10-year Brazilian swap rates.

China: Tapping SOE profits

Dinny McMahon notes that in a recent explainer, the finance ministry (MoF) revealed that last year it hiked up SOE profit remittance ratios, as he anticipated. In China wholly owned SOEs are obliged to remit a portion of their profits to the government. Most non-financial, centrally-owned SOEs are classified into one of five categories depending on their business line, subjecting them to profit remittance rates ranging from 0%-25%. In 2025, MoF merged Tier-1 and 2 SOEs into one group and raised their remittance ratio to 35%. This covers China Tobacco, the three major telecommunication and petroleum firms, and electricity utilities and grid firms. MoF also raised the profit remittance ratio for what had previously been Tier-3 firms – which cover SOEs operating in competitive sectors like mining, transportation, and trade – from 15% to 30%. It raised the ratio for Tier-4 firms from 10% to 20%. Dinny wonders if local governments will follow suit and ramp up profit remittance ratios for locally-owned SOEs?

China: Game plan

Niall Ferguson’s takeaway from China’s response to the Third Gulf War and from the design of its new Five-Year Plan is that Beijing is focused on further supply-chain diversification and greater self-sufficiency. We remain sceptical that China can deliver the household consumption revival it seeks. What is clear, however, is that the leadership sees technological innovation as the only way out of China’s socio-economic challenges. The longer the Middle Eastern conflict goes on, the more likely it is to accelerate CNY-denominated trade. When the dust finally settles over Iran, the regional balance may well shift modestly toward China and its currency, at the expense of the United States and the dollar. Niall also believes that an escalation in the Middle East will fuel inflationary pressures, causing the PBoC to wait until 2Q/2026 to start cutting rates via both the reserve requirement ratio (RRR) and the loan prime rate (LPR).

India: Monitoring for a potential short

The iShares MSCI India ETF (INDA US, USD45.82) has broken below the Mar 2025 low of USD47.60 trading down to USD45.71 last week. Last week’s decline completed an 18-month Descending Triangle, targeting a fall to USD38.00. RSI is at an Oversold 27 after peaking around/below High Neutral 60 for 15 months. If a weak rebound rally occurs, Chris Roberts will consider a short, but his base view is that the current global decline is a dislocation, so he would keep risk tight. Chris would only consider buying if one of the USD Indian ETFs formed an acceptable classic chart pattern buy setup.

Iran: What lies ahead

Every time Trump pushes back the deadline for reaching an agreement with Iran, the credibility of his threat wanes and Brunello Rosa sees little reason as to why the Iranians would now feel compelled to give ground. There is a deeper issue: Iran does not trust Trump. The only strategy may be for Iran to impose enough pain by prolonging the conflict until the US and its allies feel the pain, which could send oil prices soaring toward $200/barrel. Brunello explores the scenarios that lie ahead should Washington target Kharg Island. One sees Tehran being toppled, but at an extraordinary cost of hundreds of thousands of troops and trillions of dollars. The second scenario is worse, one that involves a prolonged war of attrition mirroring that of Vietnam. Brunello sees the third possibility of the US achieving its objectives in a matter of months as unrealistic.

South Africa: Bozell is in town, now what?

The US Ambassador to South Africa, Leo Brent Bozell III, officially assumed his duties in February. Since then he has tried to strike a balance between creating space for cooperation and negotiation and being firm on President Trump’s misgivings about and demands of SA. Bozell has repeated the US’s ‘five asks’, with B-BBEE revocation or exception for US companies being the top priority. Peter Montalto sees this as a challenging objective to achieve. A forthcoming DTC review offers a key opportunity for constructive engagement, though would not yield results on Trump’s desired timeline; as such, Peter believes the Ambassador should focus on other aspects of the commercial relationship, which is the cornerstone of his efforts to rekindle relations with SA and where progress would be easier. In his latest report, Peter zooms in on the feasibility of the five asks and considers the sanctions risk in case relations are not rekindled.

Vietnam: Off to a strong start

Jonathan Anderson points out that Vietnam is off to a strong start in 2026. Exports and tourism have continued to boom over the past two quarters, with unabated global market share gains. And local spending and credit activity are also on a steady upward trend. As always, Jonathan stays with the underlying growth story. Risks remain if Vietnam gets caught in the middle of a worst-case US-China trade war, but with high external "basic" balance surpluses, ongoing share gains and strong domestic indicators he holds his equity market position as the country continues its path as an Asian tiger.

Commodities

The mispriced escalation risk

Markets have transitioned into a new, high-volatility regime where prolonged conflict is now the base case. The Oil Volatility index (OVC) has surged toward 120, in line with Ron William’s projected target, reflecting crisis-level conditions and implying ~35% monthly price swings (see chart). Ron sees the possibility of prices heading to $200/barrel as markets transition from localised disruption to broader macro dislocation, a possibility that historical precedent presents as highly plausible. This reflects a larger, geopolitically driven cycle instead of a short-term spike, and the dynamic is unfolding within a broader commodity super-cycle framework: gold leads during monetary stress, copper confirms late-cycle growth pressure, and Energy ETF (XLE) is already up +35% YTD in line with Ron’s tactical call. The current environment increasingly resembles a 1970s-style regime of rolling inflation waves, with stagflation risks re-emerging.

Time’s up for just-in-time supply chains

When the US and Israel launched their initial strikes on February 28th, the market priced in a swift resolution. Here at Commodity Intelligence, James Burdass initiated a "30-Day Supply Chain Clock," representing the maximum structural buffer built into the modern, just-in-time global economy. This week, that clock officially struck zero. As the City lawyers are actively witnessing, the logistics have failed, and the contracts are now being torn up. James notes that for the last month, algorithms have traded the rhetoric of peace plans. But peace on paper does not put diesel in an Australian truck, it does not process Chilean copper, and it does not force a supplier to honour a contract when a force majeure has been legally triggered. As the 30-day threshold is crossed, the global market is violently bifurcating between those who own the physical molecules and those who only own the paper promises. Markets also now face the real prospect of accelerating inflation.

Mining equities in turbulent markets

The US-Israeli war with Iran and oil shock has resulted in some of the most volatile markets of recent times. Higher oil prices are clearly inflationary; however, the larger short-term risk for the miners is arguably the supply of liquid fuel.Slowing global growth could erode copper demand; the copper sector P/NPV10 and +1 year P/CF is trading close to previous tough levels with a spot FCF yield of 5.2% being attractive. Gold equities are still attractive with the market imputing lower spot prices today. The shares are cheap on a cash flow basis with a 6.9% spot FCF yield. Gold sector margins are still robust with better balance sheets compared to peers. Copper and gold equities have corrected, and value opportunities have emerged. Preferred coppers are Antofagasta PLC, Lundin Mining Corp and Ivanhoe Mines Ltd, whilst least preferred are First Quantum Minerals Ltd and Southern Copper Corp. Preferred golds are Barrick Gold Corp, Agnico Eagle Mines Ltd and Kinross Gold Corp.

Gold’s next move

In his latest video, Jeffrey Christian of CPM Group reviews the latest developments in gold, silver, platinum, and palladium markets, explaining why prices are rising again and what may come next. He discusses the recent price movements in gold and silver, including the sharp rally earlier in the year, the pullback following Federal Reserve policy signals, and the renewed strength tied to political tensions and broader concerns about global economic stability. Jeff also addresses recent commentary around Russian gold sales, clarifying how the Russian central bank has been managing its reserves since the start of the Ukraine conflict and why recent sales are not unusual in that context. He then turns to the growing interest in hedging, particularly among mining companies, and explains how producers and investors can protect profits while maintaining upside exposure.

Click here to watch.