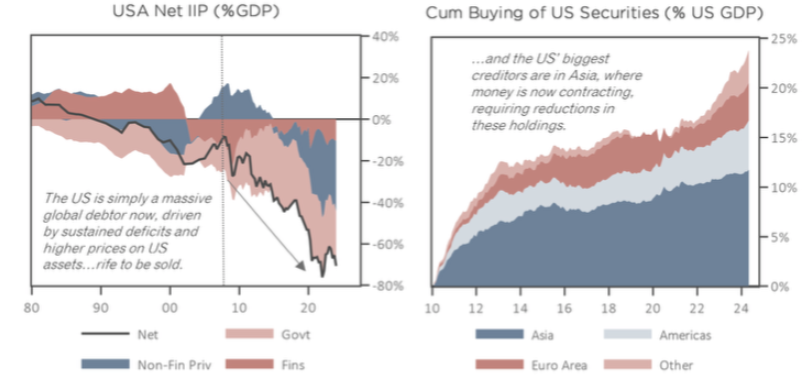

Asian Financial Crises v.2.0

Whitney Baker believes North Asian financials will buckle under the one-sided mismatches they’ve built up in US assets, with losses buried under the veneer of tech-geared equity gains. Liabilities are being contracted by policymakers’ own misguided attempts to defend currencies. Shrinking monetary bases force bond sales, crowding out stocks. Asian sales of US bonds add duration back to the US, aligning with a shallow American recession. Despite ongoing investment in infrastructure, the Fed will overreact with rapid rate cuts, causing a rotation out of US stocks into bonds. As Asians repatriate funds, the dollar weakens, triggering asset declines. Eventually, renewed Fed printing sets the stage for a stagflationary recession. Bottom line: in AFC v.2.0, the Asians are the creditors with too many foreign assets, while the US is the EM with too many foreign liabilities.

Argentina: Should we worry about the Treasury’s short-term debt?

The stock of zero-coupon ARS-denominated LECAPs soared in recent weeks, with the total outstanding value reaching ARS17.8trn. On top of this, the government is in conversation with banks to transform ARS13.3trn of reverse repos into a new note. Marcos Buscaglia examines the evolution of short-term ARS Treasury debt in the next 12 months. In the base case scenario, the evolution of short-term debt does not balloon. Even if the BCRA has to sterilise the equivalent of $300m per month, the debt is still not unstable. For instability to occur there needs to be either a new issuance in high quantities, a much higher increase in real interest rates, or a cessation of the upcoming devaluation.

China’s wargames in the Indo-Pacific

Although the US and China seek to rekindle ties, Indo-Pacific security is a major flashpoint. China’s Digital Silk Road (DSR) is a multi-tiered mega-infrastructure project aimed at expanding Beijing’s influence and technological foothold in the Indo-Pacific. The DSR is representative of China’s hybrid warfare, fusing both traditional combat with covert intelligence operations. The emergence of new, pro-China leaders in the region delineates a shift in regional politics and a renewed trust in Beijing. China’s enormous investment in the Indo-Pacific states is shrouded in uncertainty and challenges the interests and sovereignty of regional nations. As the US and the greater Western order attempt to challenge China’s growing sense of hegemony, Beijing’s wargames continue to intensify in the region.

Kenya: Protests run out of steam

Anti-government protests planned in several urban centres, including Nairobi, failed to materialise on July 4th. This comes after protests calling for President William Ruto to resign took place in multiple areas. Those protests followed mass demonstrations in June to denounce the Finance Bill 2024, which Ruto has since withdrawn. Several reasons account for failed demonstrations, including concessions put forward by Ruto, the lack of a coordinating body, apathy among activists and lack of public support. These factors and additional concessions by Ruto suggest that further major protests are unlikely in the immediate term.

Korea: Adding to the long

The Kospi 200 weekly close above 385 is viewed as a breakout from a 14-week consolidation, targeting 410 (chart 1). Last week’s strong showing has taken RSI up to 69, just below overbought 70. Chris Roberts is now 100% long from 325.60 and is moving the stop on this position to a daily close below 344. He adds another 10% at market and 10% at 388.50, with the stop loss at a daily close below 355. Chris Roberts’ longer-term target stays at 500+, with the index remaining in a secular uptrend.

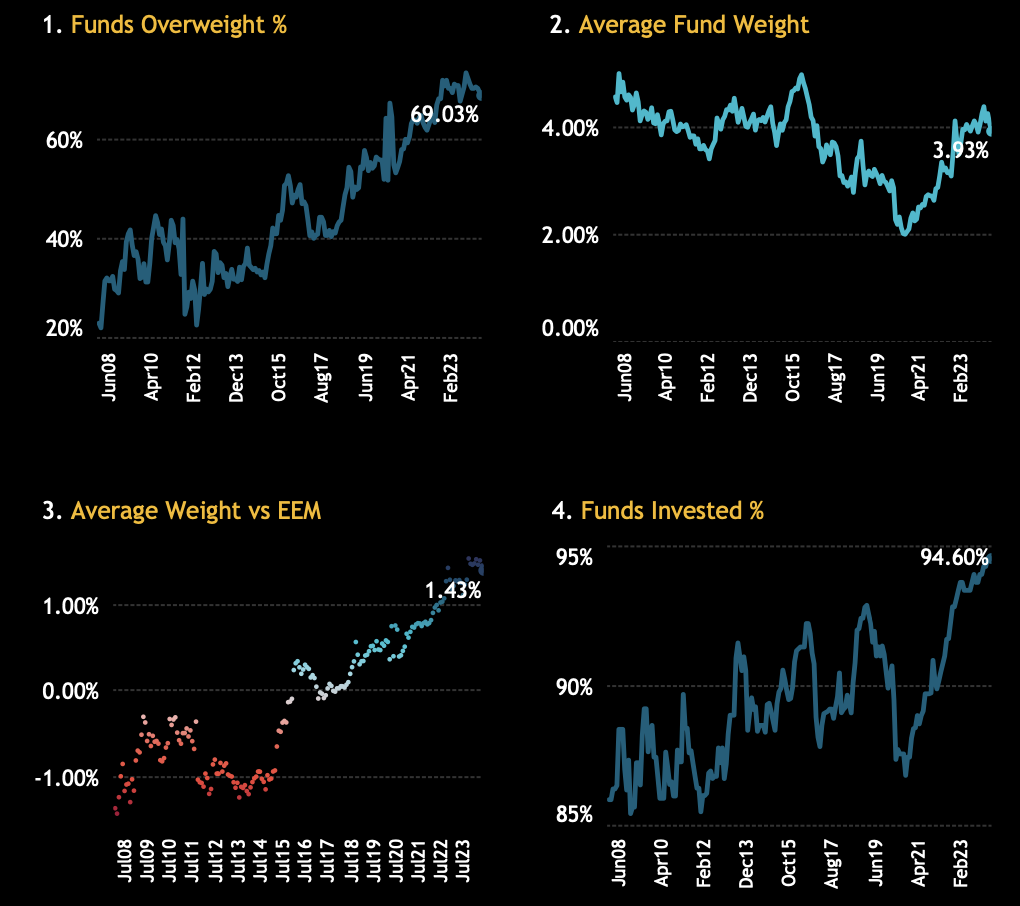

Mexico: GEM funds wrong footed after election results

Active GEM fund managers were caught off guard with their exposure to Mexico heading into the election. The nation had benefited from increased inflows and exposure over the past 3-4 years, with the percentage of funds invested reaching an all-time high of 94.6%. However, the country’s positioning against the benchmark is where it truly stands out, with the percentage of EM funds overweight the benchmark now at 69% compared to just 20% in 2011. This proved costly in the wake of the elections, with crowded stocks like Banorte experiencing big price declines. As it stands in the EM space, Mexico is the largest overweight by average fund weight and the second most common overweight after Indonesia.

Kazakhstan: Next on the list

After Russia, Kazakhstan has the second strongest credit cycle in EM, with a clear surge in local demand and real activity. Just as in Russia, Jonathan Anderson believes the Kazakh economy is hitting peak domestic growth, as external incomes are flat, and the central bank is maintaining high nominal and real rates. In terms of markets, current KZT valuation looks supported by rates, and Jonathan also has no problem with current sovereign dollar yields, but he does have concerns about the recent massive surge in equity prices and multiples.